Mortgage Pre-Approvals: Everything You Need to Know

Buying a home is an exhilarating milestone, but one that is preceded by careful planning and sound decision-making. One of the initial and foremost milestones on the journey is getting a mortgage pre-approval. It can give you clarity, confidence, and negotiating power when you make an offer. If you're thinking about diving into the real estate market, this is what you need to know about mortgage pre-approvals.

What is a Mortgage Pre-Approval?

A pre-approval on a mortgage is a promise by your lender that they will lend you money to buy a house based on where you are currently. It's not the same as being approved for a mortgage, but it's a very powerful indicator that you will be approved if something significantly awful doesn't happen to your finances by closing time.

In doing so, the lender will also verify your income, debt, credit history, and other personal financial information. They'll also give you an interest rate quote (which will usually be valid for a limited time frame), so you'll know approximately how much they can lend to you.

Why a Pre-Approval Matters

Know Your Budget

A pre-approval gives you an accurate range of prices to go out and purchase homes. It makes you stay within homes that you can purchase and avoid the heartache of falling in love with a home that you cannot afford.

Shows Seriousness to Sellers

To sellers on red-hot markets, sellers might appreciate buyers having a pre-approval. It shows you are financially prepared and serious about placing a bid.

Lock in Your Interest Rate

Most but not the most liberal lenders will pre-lock your interest rate 60 to 120 days ahead, which can be a buffer effect in case interest rates go up between the date of the pre-approval and when you close.

Spot Potential Problems Early

If your credit history or debt-to-income ratio needs to be adjusted, the pre-approval process will identify it beforehand so that you can adjust it before you make an offer.

What Lenders Take into Account

In order to determine your qualification and terms of your loan, lenders will consider:

Credit Score – Having a higher score can lead to good interest rates and loan terms.

Income – Steady and confirmed income is preferred by lenders.

Debt-to-Income Ratio – A ratio of debt payments to income. Lower is preferable.

Employment History – Stable employment history, preferably in the same position, is ideal.

Down Payment – The size of your down payment impacts the loan amount and whether you’ll need mortgage insurance.

Documents You’ll Need

When applying for a mortgage pre-approval, be prepared to provide:

Proof of identity (government-issued ID)

Proof of income (pay stubs, T4 slips, tax returns)

Employment verification

Bank statements

Account of existing debts and assets

Having these documents in hand can expedite the process and demonstrate to the lender that you're prepared.

How Long Does a Pre-Approval Last?

Pre-approvals generally last between 60 and 120 days. You can reapply if you can't purchase a house within this time period, but probably will have to resubmit documents and financial information.

Pre-Approval vs. Pre-Qualification

These are usually misleading words, but they are not the same:

Pre-Qualification – Informal estimate based on information you provide, often without verifying documents. It's quick, but less accurate.

Pre-Approval – Professional process by which the lender verifies your information. It is of more significance to lenders while quoting quotes.

Avoidable Mistakes

Job and Income Changes

Job change while in pre-approved status forces the lenders to reverify your application.

Gathering New Debt

New charges on the credit card or new loans increase your debt-to-income level and ruin your approval prospects.

Neglecting Your Credit Score

Keep making payments on time and avoid major credit shifts until the house closes.

Not Shopping Around for Lenders

Every lender will have different rates and terms, so comparing would be a wise decision.

What Occurs Following Pre-Approval

With your pre-approval in hand, you are now ready to go house hunting with a firm budget in tow. When you write an offer on a house, the lender will begin a full mortgage application process, finish underwriting, and a property appraisal.

If your financial terms don't change and the home qualifies with the lender, you'll receive final approval and will be ready to close the deal.

Simple Pre-Approval Tips

Check Your Credit First – Being ahead of your score could give you time to make improvements.

Save for a Higher Down Payment – Putting more money down at closing could reduce your loan amount and monthly payment.

Be Financially Secure – Avoid large purchases, co-signing a loan, or large bank deposits.

Deal with a Mortgage Expert – They can negotiate with the lender and secure favorable terms.

The Bottom Line

Pre-approval is more than just a figure—it's an asset that gives you clarity, confidence, and credibility when buying real estate. It creates realistic expectations, makes your offers stronger, and avoids surprises down the line.

Whether you’re a first-time buyer or an experienced homeowner, taking the time to secure a pre-approval before house hunting can make all the difference in finding your dream home and securing it on the best possible terms.

Categorii

Citeste mai mult

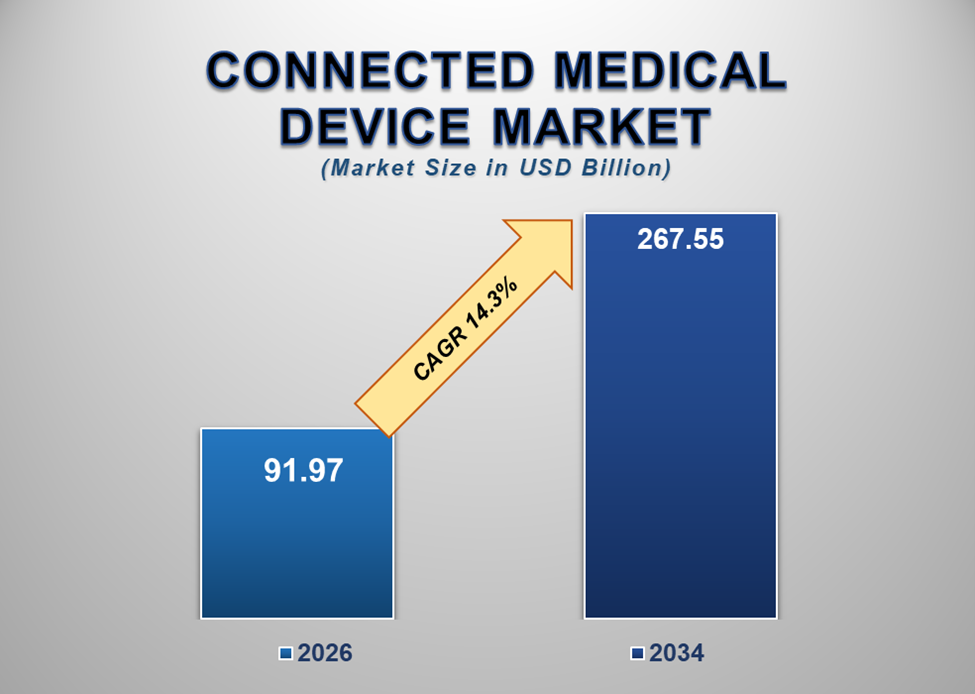

The Connected Medical Device Market Demand is rapidly transforming the global healthcare ecosystem by integrating advanced technologies such as IoT, artificial intelligence (AI), and cloud computing into medical devices. These smart devices enable real-time data collection, remote monitoring, and improved patient outcomes, making healthcare more efficient, personalized, and...

In current years, plug-in automotive gadgets have won popularity as quick and less expensive solutions. One such product is the SynGas OBD Fuel Saver, which claims to decorate fuel economy and optimize engine performance. Its easy set up and ambitious promises have attracted huge attention, but many drivers nonetheless marvel how it honestly works and whether or not it gives you actual...

Hydraulic pumps are vital components in many industrial and mechanical systems, powering machinery efficiently and reliably. Businesses across the manufacturing, construction, and automotive sectors in Singapore rely heavily on hydraulic pumps in Singapore to maintain smooth operations. Choosing the right pump ensures higher performance, reduces maintenance costs, and minimizes operational...

Accessing your account smoothly is one of the most important parts of using any online platform. However, there are times when users may face login issues that interrupt their experience. On Betbhai9, these issues are usually minor and can be resolved quickly with the right understanding. Knowing the common causes and simple fixes helps users regain access without frustration and continue...

Perfect Valentine’s Gift Options Valentine’s Day serves as a heartfelt reminder that the most meaningful expressions of love often come through thoughtful actions and meaningful connections. It’s a special occasion to celebrate the bond you share with someone dear, yet choosing the perfect gift can sometimes be a challenge. While traditional presents are always appreciated,...