Clutch Friction Plate Market 2030: Growth Trends and Analysis

The global automotive industry relies heavily on a complex ecosystem of mechanical components that ensure efficient power transmission, vehicle control, and driving comfort. Among these components, clutch friction plates play a pivotal role in vehicles equipped with manual and semi-automatic transmission systems. Acting as the interface between the engine and the drivetrain, clutch friction plates facilitate smooth gear shifting, torque transfer, and vehicle performance optimization. As global vehicle production continues to evolve, the clutch friction plate market remains a critical subsegment of the automotive components industry.

According to TechSci Research report, “Clutch Friction Plate Market – Global Industry Size, Share, Trends, Competition Forecast & Opportunities, 2030”, the Global Clutch Friction Plate Market was valued at USD 12.40 Billion in 2024 and is projected to reach USD 15.88 Billion by 2030, expanding at a compound annual growth rate (CAGR) of 4.21%. This steady growth reflects sustained demand from both original equipment manufacturers (OEMs) and the aftermarket, supported by expanding vehicle parc, increasing vehicle lifespan, and persistent demand for replacement components.

Despite the gradual shift toward automatic and electric vehicles, clutch friction plates continue to hold relevance, particularly in emerging economies, performance-oriented vehicle segments, and cost-sensitive markets where manual transmissions remain dominant. This article provides a comprehensive and in-depth overview of the global clutch friction plate market, covering market dynamics, segmentation, emerging trends, regional insights, competitive analysis, and future growth prospects.

Industry Key Highlights

-

The global clutch friction plate market is projected to grow steadily through 2030, driven by vehicle parc expansion and aftermarket demand.

-

Aftermarket sales account for a significant share due to regular wear and tear of clutch components.

-

Passenger cars remain the dominant application segment globally.

-

Emerging markets in Asia-Pacific, South America, and the Middle East are key growth engines.

-

Technological advancements in friction materials are enhancing durability and performance.

-

Despite increasing adoption of automatic transmissions, manual vehicles continue to sustain demand.

-

Manufacturers are investing in lightweight, heat-resistant, and long-life friction plate solutions.

-

OEMs focus on performance optimization, while aftermarket players emphasize compatibility and affordability.

Download Free Sample Report: https://www.techsciresearch.com/sample-report.aspx?cid=21445

Understanding Clutch Friction Plates and Their Role in Vehicles

A clutch friction plate is a crucial mechanical component that enables smooth engagement and disengagement of power between the engine and the transmission. Positioned between the flywheel and the pressure plate, it relies on friction material to transmit torque when engaged and disengage power during gear shifts.

The durability and performance of a clutch friction plate directly influence driving comfort, fuel efficiency, and transmission longevity. Over time, friction plates wear out due to repeated engagement cycles, heat exposure, and mechanical stress, making replacement inevitable. This inherent wear-and-tear characteristic underpins the robust demand for clutch friction plates, particularly in the aftermarket.

Market Drivers

1. Expanding Global Vehicle Parc

One of the primary drivers of the clutch friction plate market is the continuous expansion of the global vehicle parc. As more vehicles are added to roads worldwide, especially in emerging economies, the installed base of vehicles requiring maintenance and component replacement increases. Even with slower growth in new vehicle sales in mature markets, the sheer volume of vehicles in operation ensures a consistent demand for replacement clutch components.

2. Strong Aftermarket Demand

The aftermarket segment is a cornerstone of the clutch friction plate market. Clutch friction plates are consumable components that require replacement multiple times over a vehicle’s lifecycle. Rather than replacing vehicles entirely, consumers increasingly prefer maintaining and repairing existing vehicles, particularly during periods of economic uncertainty. This behavioral shift significantly benefits aftermarket suppliers.

For example, manufacturers continue to introduce new aftermarket-compatible clutch friction plates designed to support older vehicle models, enabling cost-effective vehicle ownership and extended vehicle life.

3. Dominance of Manual Transmissions in Emerging Markets

While automatic transmissions are gaining popularity globally, manual transmissions remain prevalent in many regions due to affordability, fuel efficiency, and driving preferences. Countries across Asia-Pacific, Africa, and parts of Latin America still rely heavily on manual vehicles, ensuring sustained demand for clutch friction plates.

4. Growth of Passenger Vehicle Production

Passenger cars represent the largest share of vehicle production worldwide. With millions of passenger cars produced annually, even marginal growth in production volumes translates into substantial demand for clutch friction plates. Additionally, passenger vehicles tend to accumulate higher mileage, further driving replacement demand.

5. Technological Advancements in Friction Materials

Ongoing research and development in friction materials, including organic, ceramic, and composite formulations, is improving clutch friction plate durability, heat resistance, and torque capacity. These advancements support market growth by enhancing product value and extending replacement intervals without eliminating replacement needs altogether.

Market Challenges

Shift Toward Automatic Transmissions

One of the most notable challenges facing the clutch friction plate market is the global shift toward automatic and semi-automatic transmissions. Automatic vehicles eliminate the need for traditional clutch friction plates, reducing long-term demand potential.

Manufacturers must adapt by diversifying into related components, focusing on performance vehicles, or targeting markets where manual transmissions remain dominant.

Increasing Adoption of Electric Vehicles

Electric vehicles (EVs) typically do not require conventional clutch systems, posing a long-term challenge to the market. While EV penetration is currently limited in many regions, accelerating electrification could impact future demand.

Emerging Trends in the Clutch Friction Plate Market

Advanced Friction Materials

Manufacturers are increasingly developing friction plates using advanced composite materials that deliver superior thermal stability, reduced wear, and smoother engagement. These innovations enhance driving comfort while extending component life.

Lightweight Component Design

Automakers and suppliers are prioritizing lightweight components to improve fuel efficiency and vehicle performance. Lightweight clutch friction plates reduce rotational mass, enhancing acceleration and transmission responsiveness.

Performance-Oriented Clutch Systems

High-performance and sports vehicles continue to rely on manual transmissions and performance clutches. This niche segment is driving demand for high-torque, multi-plate clutch systems with superior friction materials.

Digitalization in Manufacturing

The adoption of advanced manufacturing technologies, including precision machining and automated quality control, is improving consistency, reliability, and scalability in clutch friction plate production.

Market Segmentation Analysis

By Type

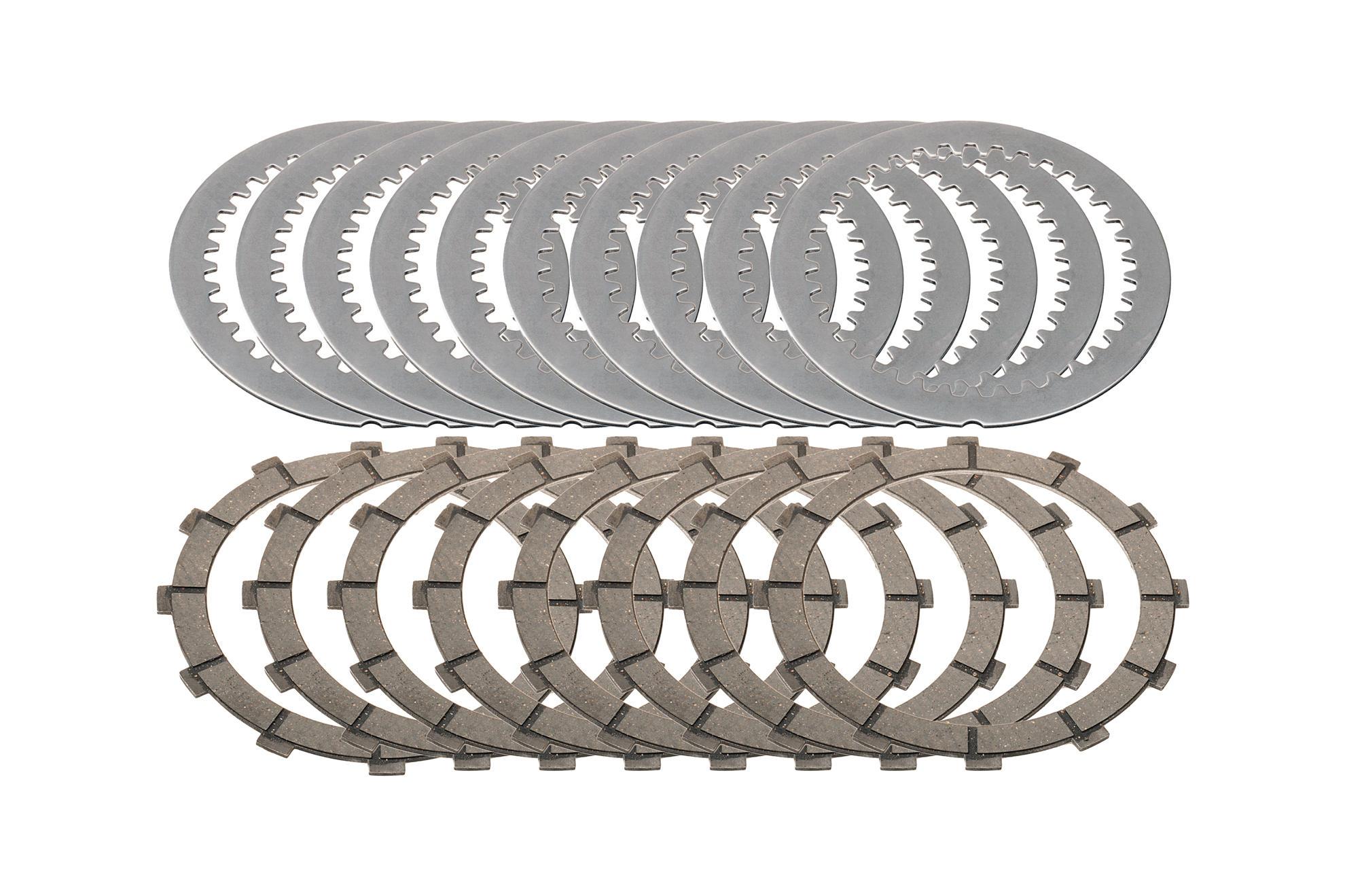

Single Plate Clutch Friction Plates

Single plate clutches are widely used in passenger vehicles due to their simplicity, cost-effectiveness, and reliability. They account for a substantial share of the market, particularly in commuter vehicles.

Multi Plate Clutch Friction Plates

Multi plate clutches offer higher torque capacity and compact design, making them suitable for high-performance vehicles, motorcycles, and commercial applications. Demand for multi plate systems is growing in performance-driven segments.

By Sales Channel

OEM Segment

OEM demand is driven by vehicle manufacturers integrating clutch friction plates during vehicle assembly. OEMs prioritize durability, performance consistency, and compliance with vehicle specifications.

Aftermarket Segment

The aftermarket dominates overall demand due to replacement needs. Independent repair shops, dealerships, and consumers rely on aftermarket clutch friction plates to maintain vehicle performance over time.

By Application

Passenger Cars

Passenger cars constitute the largest application segment due to high production volumes, widespread use of manual transmissions, and extended vehicle ownership periods.

Commercial Vehicles

Commercial vehicles, including trucks and buses, require heavy-duty clutch friction plates capable of handling high torque and frequent load variations. While smaller in volume, this segment commands higher value per unit.

Regional Analysis

Asia-Pacific

Asia-Pacific represents the largest and fastest-growing regional market, driven by high vehicle production, growing middle-class population, and dominance of manual transmissions. Countries such as China, India, and Southeast Asian nations contribute significantly to regional demand.

Europe

Europe is a mature market characterized by technological sophistication and stringent quality standards. While automatic transmissions are common, performance vehicles and aftermarket demand continue to support the clutch friction plate market.

North America

North America shows steady demand, particularly in the aftermarket and performance vehicle segments. Pickup trucks, sports cars, and older vehicle models contribute to replacement demand.

South America

South America offers strong growth potential due to increasing vehicle ownership and extended vehicle lifecycles. Economic considerations encourage repair and maintenance rather than vehicle replacement.

Middle East & Africa

This region is emerging as a growth opportunity, supported by expanding automotive markets, infrastructure development, and rising demand for affordable transportation solutions.

Competitive Analysis

The global clutch friction plate market is moderately consolidated, with a mix of multinational corporations and regional players competing on product quality, pricing, distribution networks, and technological innovation.

Key Competitive Strategies

-

Product portfolio expansion targeting both OEM and aftermarket segments

-

Geographic expansion into high-growth emerging markets

-

Strategic partnerships with vehicle manufacturers and distributors

-

Investment in R&D for advanced friction materials

-

Emphasis on durability and compatibility with older vehicle models

Major Companies Operating in the Market

-

AISIN Corporation

-

BorgWarner Inc.

-

Schaeffler Automotive Aftermarket GmbH & Co. KG

-

Valeo SA

-

ZF Friedrichshafen AG

-

Eaton Corporation plc

-

EXEDY Corporation

-

Mitsubishi Electric Europe B.V.

-

Haldex AB

-

Setco Automotive Limited

These companies compete by leveraging strong brand recognition, extensive distribution networks, and technological expertise.

Future Outlook

The global clutch friction plate market is expected to maintain stable growth through 2030, supported by strong aftermarket demand, expanding vehicle parc, and continued relevance of manual transmissions in emerging markets. While electrification and automatic transmission adoption present long-term challenges, the market is likely to remain resilient due to regional disparities in technology adoption and consumer preferences.

Manufacturers that invest in innovation, diversify product portfolios, and strengthen aftermarket presence will be best positioned to capture future growth opportunities. Strategic expansion into emerging markets and development of high-performance and specialty clutch systems will further enhance competitive positioning.

10 Benefits of the Research Report

-

Provides comprehensive market size and growth forecasts through 2030

-

Offers detailed segmentation by type, sales channel, application, and region

-

Identifies key growth drivers, challenges, and emerging trends

-

Supports strategic planning and investment decision-making

-

Analyzes competitive landscape and company strategies

-

Highlights high-growth regional markets and opportunities

-

Assists OEMs and aftermarket players in product positioning

-

Enables benchmarking against industry leaders

-

Supports market entry and expansion strategies

-

Delivers actionable insights for stakeholders across the value chain

Conclusion

The global clutch friction plate market continues to demonstrate resilience and relevance within the evolving automotive landscape. Driven by aftermarket demand, expanding vehicle ownership, and technological advancements, the market offers steady growth opportunities despite structural shifts toward automation and electrification. With strategic adaptation, innovation, and regional focus, industry participants can sustain growth and capitalize on long-term market potential through 2030 and beyond.

Contact Us-

Mr. Ken Mathews

708 Third Avenue,

Manhattan, NY,

New York – 10017

Tel: +1-646-360-1656

Email: sales@techsciresearch.com

Website: www.techsciresearch.com

Categorie

Leggi tutto

As per Market Research Future, the Ancillary Services Power Industry is playing a pivotal role in maintaining the stability, reliability, and efficiency of modern electricity grids. Ancillary services encompass a range of support functions essential for the smooth operation of power systems, including frequency regulation, voltage control, spinning reserves, and black start services. These...

Executive Summary Europe Colour Cosmetics Market Size and Share Analysis Report The Europe colour cosmetics market size was valued at USD 12.83 billion in 2024 and is expected to reach USD 21.56 billion by 2032, at a CAGR of 6.70% during the forecast period. Europe Colour Cosmetics Market research report acts as a great source of information with...

"Induced Pluripotent Stem Cells (iPSCs) Market Summary: According to the latest report published by Data Bridge Market Research, the Induced Pluripotent Stem Cells (iPSCs) Market The global induced pluripotent stem cells (iPSCs) market size was valued at USD 2.13 billion in 2025 and is expected to reach USD 4.53 billion by 2033, at a CAGR of 9.90% during...

Анализ роли Тан Тан в крио-композициях раскрывает её как архитектора боевого ритма, а не просто источник урона. Её уникальность — в управлении временем. Она не наполняет энергией напрямую, а создаёт «воронки», ускоряющие сам процесс её генерации для ключевых союзников. Это превращает статичную схему боя в динамичный поток, где ультимативные способности активируются с пугающей...

The Cellulose Market research report has been crafted with the most advanced and best tools to collect, record, estimate, and analyze market data. The report also sheds light on the market overview in its entirety touching diverse aspects like product definition, prevailing vendor landscape, and market segmentation. Through the comprehensive and systematic market research study, the report...