Health Insurance in India: Comparing Plans, Premiums, and Coverage in 2025

The health insurance landscape for India is changing quickly. As we move forward into 2025 technological integration, regulatory changes and a post-pandemic emphasis on wellness are changing where Indians go for their cover.

Choosing a health plan is now about much more than just looking for the sum insured, it is about finding a detailed balance of cover, exclusions and premium to cover.

This article highlights the key elements you will want to consider when comparing and choosing the best health insurance for India this year.

Comparing Health Insurance Plan Types

The first step is understanding the types of plans available. Here’s a comparison between the plans:

|

Plan Type |

Who It’s For |

Features |

|

Individual Plans |

Young, single adults looking for affordable coverage. |

Dedicated sum insured for one person. |

|

Family Floater Plans |

Families wanting shared coverage under one plan. |

Single sum insured for all members, advanced restore/recharge features with unlimited restoration, even for unrelated illnesses. |

|

Senior Citizen Plans |

Adults above 60 years. |

Higher premiums cover age-related ailments, reduced waiting periods for pre-existing conditions (as low as 1–2 years); OPD coverage including pharmacy bills. |

|

Top-Up & Super Top-Up Plans |

Individuals with a base/corporate plan seeking extra protection. |

Activate after deductible is crossed; cost-effective way to increase coverage; ideal as an additional safety net. |

Factors Driving Premiums in Health Insurance

The premium is the price of your policy, and it is established by a number of factors. There are a lot of choices and just picking the cheapest one can be a costly error. Here are some of the factors:

Age & Demographics: This remains the primary factor. Premiums increase with age as health risks rise.

Sum Insured: A higher sum insured directly translates to a higher premium. However, the incremental cost for a significantly larger cover is often worthwhile.

Medical History: Insurers now use more sophisticated underwriting processes and your personal, family medical history can have an impact on your premium.

Policy Features: Add-ons like critical illness riders, international coverage, or a lower co-payment clause will increase the premium. Compare what's included in the base plan versus what is an optional extra.

Insurer’s Claim Settlement Ratio (CSR): A higher CSR often correlates with slightly higher premiums, but it’s a price worth paying for reliability.

Coverage in Health Insurance

A complete coverage extends far beyond hospitalization. Here things to look out for:

Pre and Post-Hospitalization: Look for plans which provide at least 60 days of pre-hospitalization and 90 days of post-hospitalization benefits for related expenses, such as diagnostics and medication.

Day-Care Procedures: Check the policy's definition of day-care procedures. It should have a lengthy list of treatments (such as a chemotherapy session or a cataract operation), which are performed without the requirement of a 24-hour hospital stay.

Modern Treatments: Coverage for modern-age treatments, such as robotic surgery, stem cell therapy, and oral chemotherapy, should no longer be considered a luxury but a necessity.

AYUSH Treatment: More policies now offer coverage for treatments provided by AYUSH (Ayurveda, Yoga, Unani, Siddha, and Homeopathy), and it is only getting more popular.

No Claim Bonus (NCB): A no-claim bonus simply means that you haven't made a claim in the previous year. Policies with the best NCB scheme, generally have a maximum limit, will add an incremental value on to your existing sum insured (e.g. each claim-free year adds a value of 50% of your current sum insured), rather than just a discount from your premium.

Conclusion

Finding the appropriate health insurance coverage for India takes a thoughtful comparative review of plans. Don't just blindly compare premiums; examine the coverage carefully, understand the exclusions, and evaluate the reputation of the insurer based on CSR and reviews by policyholders.

There are also specialized products (e.g., Health insurance for NRI) for non-residents getting coverage for their time in India. You can use online aggregators to compare plans side-by-side but always read the final policy wording document before you purchase.

Categorias

Leia Mais

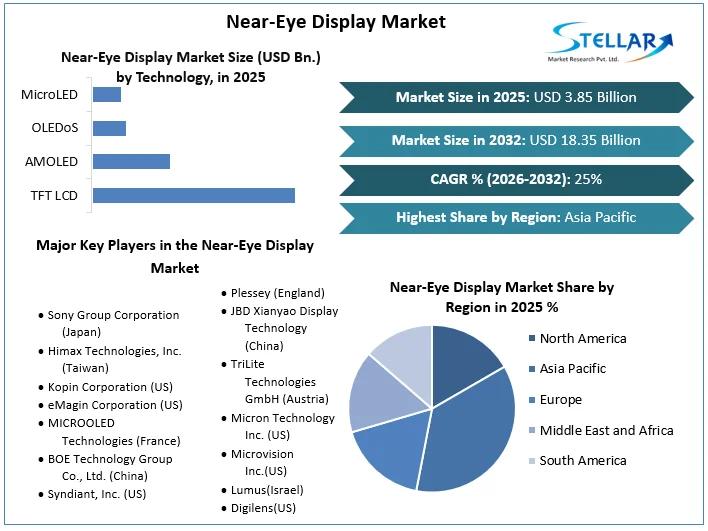

Market Estimation & Definition The global Near-Eye Display Market is witnessing remarkable growth, driven by increasing adoption of immersive technologies across consumer electronics, healthcare, automotive, and defense sectors. According to the latest study by Stellar Market Research, the market was valued at approximately USD 3.85 billion in 2025 and is projected to reach nearly...

The global Software Consulting Market Share is a vast, complex, and highly competitive landscape, with a structure that is best understood as a tiered pyramid. The market is not dominated by a single type of firm; rather, its share is distributed across several distinct categories of players, each with a different business model, target client, and competitive advantage. The top of...

Drew House: The Story Behind Justin Bieber’s Iconic Streetwear Brand In the world of fashion, trends come and go, but authenticity always leaves a mark. Among the countless streetwear labels that have emerged in recent years, one brand has captured the world’s attention not only for its celebrity founder but also for its laid-back, carefree philosophy — Drew House....

A laser cleaner is an advanced surface treatment solution designed to remove rust, paint, oil, oxide layers, and other contaminants from different materials with high precision. It is widely used across industries for restoring metal surfaces, preparing materials for welding, and maintaining equipment efficiency. Unlike traditional cleaning methods, a laser cleaner provides a modern,...

Mango atchar is more than just a condiment; it’s a vibrant reflection of South Africa’s rich culinary heritage. This spicy mango pickle, cherished by households and restaurants alike, adds a burst of flavour to any meal. Whether you’re a food lover seeking the best mango atchar in South Africa or a retailer looking to stock authentic products, understanding this traditional...