Cheapest Super Visa Insurance for Parents Over 60: 2026 Pricing & Plan Picks

Inviting your parents or grandparents to Canada on a Super Visa is an unforgettable experience — but one requirement you cannot skip is medical insurance that meets Canadian immigration standards. This policy must provide emergency medical coverage, hospitalization, repatriation, and be valid for at least one year. Finding the cheapest Super Visa insurance for parents over 60 can seem challenging, especially since premiums rise significantly with age and health factors, but it’s not impossible with the right approach.

In this comprehensive guide, we explore realistic 2026 pricing data, the best plan picks for older visitors, and practical tips to reduce your insurance costs without sacrificing essential coverage.

Understanding Super Visa Insurance Requirements

Before diving into pricing, it’s crucial to know the requirements set by Immigration, Refugees and Citizenship Canada (IRCC). Your Super Visa insurance must meet the following criteria:

-

Provide a minimum of $100,000 CAD in emergency medical coverage.

-

Be valid for at least one year from the date of entry.

-

Include hospitalization, healthcare, and repatriation.

-

Be paid in full or with documented instalments that cover the entire policy term.

These requirements are strict — IRCC officers may request proof of paid coverage when your parents enter Canada.

Also note that visitor visa insurance Canada policies designed for short-term tourism are not the same as Super Visa plans. While visitor insurance might be cheaper on a per-month basis, it typically doesn’t meet Super Visa criteria for minimum coverage and duration.

Why Super Visa Insurance Costs Rise with Age

Insurance premiums are largely based on risk assessment. Older adults face a higher likelihood of health issues, and insurers price policies accordingly. According to recent pricing data:

-

A person aged 61–64 may pay around $1,168 per year for $100,000 coverage with no pre-existing condition coverage.

-

Premiums can quickly exceed $3,000+ per year for applicants aged 80 and above.

These estimates highlight why searching for the cheapest Super Visa insurance requires careful consideration of different providers and strategies tailored to those over 60.

Current Pricing Trend for Parents Over 60 (2026)

Here’s a realistic snapshot of premiums for older visitors based on recent insurer estimates and industry data:

Typical Annual Premiums for $100,000 Coverage (No Pre-Existing Conditions)

-

60 years: Approx. $1,300–$1,700

-

65 years: Approx. $1,600–$2,000

-

70 years: Approx. 2,200–$2,800

-

75 years: Approx. 2,800–$4,200

Monthly payments are also available through many insurers, making premiums easier to manage, albeit sometimes slightly higher overall due to financing costs.

Top Picks for Cheapest Super Visa Insurance in 2026

Here’s where you can find competitive plans for parents over 60 — balancing lower premiums with required coverage:

1. RIMI (Secure Travel) — Best for Lower Monthly Premiums

RIMI offers some of the lowest priced Super Visa plans for older applicants, especially for people aged 60–75. Their monthly premiums are typically among the most affordable, with optional coverage for stable pre-existing conditions.

Estimated Monthly Rates (with $100k coverage):

Why it’s a top cheap choice:

✔ Lowest base premiums in many age brackets

✔ Flexible deductible and pre-existing condition options

✔ Option to pay monthly instead of upfront

2. 21st Century — Low Base Premiums with Flexible Deductibles

21st Century remains a strong choice when hunting for the cheapest Super Visa insurance that still meets IRCC requirements. It’s particularly worth considering if your parents are in generally good health.

Monthly Sample Rates (approx.):

Advantages:

-

Simple application processes

-

Wide selection of deductibles to reduce premiums

-

Coverage up to two years available in some plans

3. GMS — Affordable If You Want Low Deductibles

For many families, the trade-off isn’t just the Super Visa insurance but also minimal out-of-pocket risk in emergencies. GMS (Group Medical Services) provides plans with low deductible options that stay cost-competitive.

Why GMS is worth considering:

✔ Competitive pricing even with low deductible options

✔ Comprehensive benefits such as prescription drugs and hospital care

✔ Good balance between price and value

This can be particularly appealing for seniors who want to avoid substantial upfront costs in the event of a medical issue.

4. Destination Canada — Value-Driven Coverage

Destination Canada can be a smart pick for seniors who want a mix of affordable pricing and additional perks, such as optional dental benefits. While slightly above the absolute lowest premiums, it still ranks among the most cost-effective broad coverage providers.

Sample Monthly Pricing:

Highlights:

-

Clear pricing tiers by age

-

Deductible options to influence premiums

-

Bilingual customer support

Tips to Reduce Your Insurance Cost Further

Even after comparing providers, there are several strategies you can use to secure the cheapest Super Visa insurance without sacrificing needed protection:

1. Increase Your Deductible

High deductibles typically result in lower premiums. While you’ll pay more out-of-pocket for a claim, the savings on regular premiums can be substantial.

2. Pay Annually if Possible

Some insurers charge a small fee to spread payments monthly. Paying annually can sometimes be cheaper overall if you have the cash flow to do so.

3. Review Pre-Existing Condition Rules

If your parent’s medical condition is stable, some insurers will offer coverage without exorbitant premium increases — but always check stability period requirements before buying.

4. Shop Multiple Quotes

Premiums can differ by hundreds of dollars for the same coverage, especially for people over 60. Comparing quotes from several companies ensures you don’t overpay.

5. Ask for Discounts

Some providers offer discounts for couples or additional add-on benefits. It’s worth discussing these with the insurer or broker before you finalize your purchase.

Comparing Super Visa With Visitor Insurance

While searching for the cheapest Super Visa insurance, some families also check visitor visa insurance Canada options. However, that type of insurance is generally meant for short-term stays and does not meet Super Visa requirements, which demand a minimum of one year of emergency coverage.

Visitor visa plans typically cover shorter stays (e.g., less than six months) and may not include features like repatriation or hospitalization at the levels required for Super Visa applications. Always verify the product details to ensure visa compliance.

Final Thoughts

Finding the cheapest Super Visa insurance for parents over 60 in 2026 doesn’t mean you must sacrifice coverage quality. By comparing providers such as RIMI, 21st Century, GMS, and Destination Canada, adjusting deductibles, and understanding pricing trends, you can secure both value and peace of mind.

Remember, premium is just one aspect — the ultimate goal is to ensure your parents are adequately protected throughout their stay in Canada, while also keeping your overall travel costs under control.

Categorii

Citeste mai mult

Trong thời đại công nghệ số phát triển mạnh mẽ, nhu cầu xem bóng đá trực tuyến ngày càng trở nên phổ biến và tiện lợi hơn bao giờ hết. Người hâm mộ không còn bị giới hạn bởi tivi truyền thống mà có thể dễ dàng theo dõi các trận đấu yêu thích mọi lúc, mọi nơi....

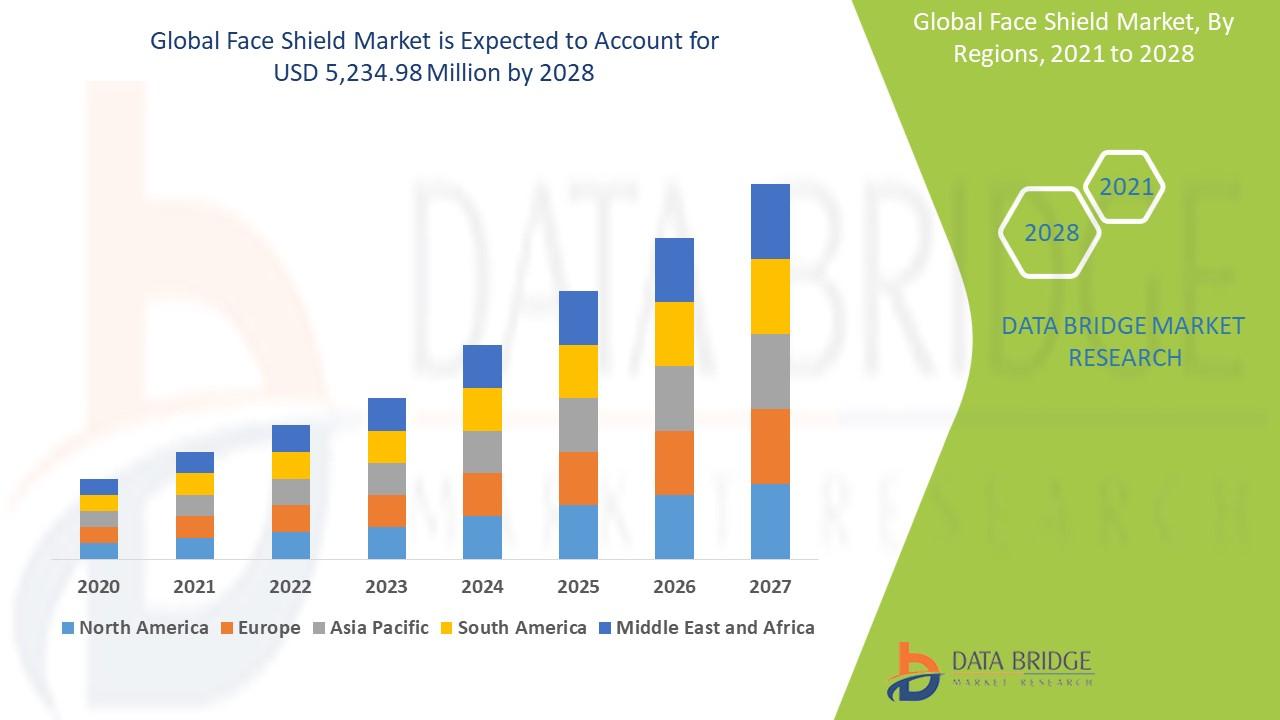

"Executive Summary Face Shield Market Opportunities by Size and Share CAGR Value The face shield market is expected to gain market growth in the forecast period of 2021 to 2028. Data Bridge Market Research analyses that the market is growing with the CAGR of 14.36% in the forecast period of 2021 to 2028 and is expected to reach USD 5,234.98 million by 2028. An international Face...

In Dune: Awakening, the Deep Desert has long served as the primary endgame region, but its constant PvP activity has drawn complaints from players seeking more PvE-focused content. Responding to this feedback, Funcom has updated the public test server (PTS) with an expanded PvE area near the shield wall, covering rows A, B, C, D, and half of E within the Deep Desert. This change effectively...

Learning how to drive has evolved significantly across Australia over the last decade. As automatic vehicles continue dominating Australian roads, more learners are now choosing Automatic Car Driving Classes over traditional manual driving instruction. From busy urban centres to growing suburban communities, automatic driving lessons are becoming the preferred option for students seeking...

According to the latest report published by Data Bridge Market Research, the Asia Pacific Thin-Film Encapsulation Market The Asia Pacific Thin-Film Encapsulation market size was valued at USD 70.56 Million in 2024 and is expected to reach USD 306.44 Million by 2032, at a CAGR of 20.15% during the forecast period In this persuasive Asia Pacific Thin-Film Encapsulation...