Factors That Influence Home Insurance Premiums

Factors That Influence Home Insurance Premiums

Home insurance premiums vary widely depending on several factors that insurance providers use to assess risk. These factors help determine the likelihood of a claim and the potential cost of covering damage or loss. Understanding what influences home insurance premiums can help homeowners make informed choices and potentially reduce their insurance costs.

One of the most significant factors affecting home insurance premiums is the location of the property. Insurers evaluate environmental risks such as exposure to storms, flooding, wildfires, or high crime rates. Homes in areas with a higher risk of natural disasters or frequent claims generally face higher premiums due to the increased likelihood of loss.

The age and condition of the home play a major role in determining insurance costs. Older homes may have outdated electrical wiring, plumbing systems, or roofing materials, which increase the risk of damage or fire. Poor maintenance can also lead to higher premiums. Homes that are well-maintained or recently renovated often qualify for lower insurance costs because they present less risk to insurers.

Construction materials and building design also influence premiums. Homes built with durable, fire-resistant materials are generally less expensive to insure than those constructed with materials that are more vulnerable to damage. Roof type, foundation quality, and overall structural integrity all factor into risk assessments.

Coverage limits and deductibles have a direct impact on premium costs. Higher coverage limits result in higher premiums because the insurer assumes greater financial responsibility. Conversely, choosing a higher deductible can lower premiums, as the homeowner agrees to cover more of the initial costs in the event of a claim. Selecting the right balance between coverage and deductible is essential for cost-effective protection.

Claims history is another important consideration. Homeowners who have filed multiple claims in the past may be viewed as higher risk, leading to increased premiums. Even claims made by previous owners of the property can sometimes affect insurance costs. Maintaining a claims-free history can help keep premiums more affordable over time.

Security and safety features can positively influence home insurance premiums. Homes equipped with smoke detectors, burglar alarms, fire extinguishers, and monitored security systems are often eligible for discounts. These features reduce the likelihood or severity of losses, making the home less risky to insure.

Lifestyle and usage factors also play a role. Homes used as rental properties, vacation homes, or for business purposes may carry higher premiums due to increased exposure to risk. Similarly, the presence of certain features, such as swimming pools or fireplaces, can raise insurance costs because they increase liability or fire risks.

Understanding the factors that influence home insurance premiums allows homeowners to take proactive steps toward managing costs. By maintaining the property, choosing appropriate coverage, and investing in safety features, homeowners can secure reliable protection while keeping insurance expenses under control.

Categories

Read More

The Indian escort KL Service: A Way to De-Stress De-stressing is achieved by hiring an Indian escort KL girl through a local agency in Malaysia. She will provide ultimate pleasure and relaxation for you. Take a break from your worry and enjoy every activity with your Indian escort KL girl in Malaysia, while fully relaxing without remorse for attempting something you cannot do with a normal...

For individuals struggling with excess weight, modern medical treatments offer more options than ever before. Two of the most popular approaches are the Allurion Balloon and weight loss surgery. Both are designed to help people lose weight and improve their overall health, but they differ significantly in terms of procedure, recovery, risks, and results. If you're considering medical...

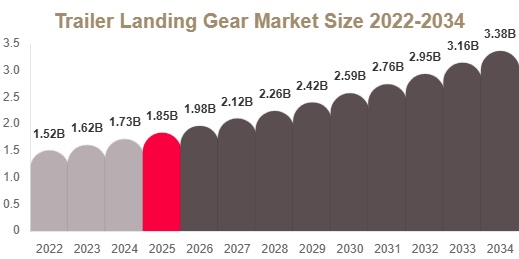

Trailer Landing Gear Market Overview The trailer landing gear market is growing due to rising demand in logistics, freight transport, and commercial trucking operations. These systems provide essential support to semi-trailers during loading and unloading operations. According to Reed Intelligence, the market is driven by global trade expansion, logistics network growth, and increasing demand...

SEBI Registered Investment Advisor Eligibility – A Complete Guide for Aspiring Professionals Have you ever thought about guiding people in managing their money the right way? With more Indians investing in mutual funds, stocks, and retirement plans, the need for trusted financial advisors is growing rapidly. But here’s the catch — in India, you cannot legally offer investment...

You want a partner who turns search visibility into predictable traffic and measurable growth. An SEO agency analyzes your site, targets the right keywords, fixes technical issues, and builds authority so your pages rank higher and attract qualified visitors. Choosing the right agency saves time and budget; this article shows what an agency does, the services to expect, and how to evaluate...