What You Must Know to Avoid IRS Penalties

Tax compliance is one of the most important yet frequently misunderstood responsibilities facing small business owners. While most businesses aim to meet their obligations, changing regulations, complex filing requirements, and administrative pressures often create compliance gaps that can lead to penalties, interest, or audits. Understanding how tax compliance works—and how enforcement typically occurs—can help small businesses reduce risk and maintain financial stability.

This guide explains what small business tax compliance involves, the most common mistakes that trigger IRS action, and practical steps businesses can take to avoid penalties while remaining compliant over time.

What Tax Compliance Means for Small Businesses

Small business tax compliance refers to meeting all applicable federal, state, and local tax obligations accurately and on time. These obligations vary depending on business structure, industry, revenue level, and geographic location. Compliance is not limited to filing annual returns; it also includes ongoing reporting, recordkeeping, and payment responsibilities throughout the year.

For federal purposes, compliance generally involves income tax reporting, employment tax filings, estimated tax payments, and information returns. At the state level, additional requirements may include sales and use taxes, employment development contributions, and franchise or gross receipts taxes.

Because tax rules apply differently to sole proprietorships, partnerships, limited liability companies, and corporations, business owners must understand how their entity type affects compliance expectations.

Core Tax Compliance Requirements Every Small Business Must Follow

Income Tax Filing Obligations

All businesses must report income earned during the tax year. How that income is reported depends on the business structure. Sole proprietors report business income on their individual returns, while partnerships and S corporations file informational returns. C corporations file separate corporate income tax returns.

Errors in income reporting—such as omitting revenue, misclassifying income, or failing to report digital payments—are among the most common compliance issues identified by the IRS.

Estimated Tax Payments

Many small businesses are required to make quarterly estimated tax payments. These payments apply when taxes are not fully covered through withholding and the business expects to owe a certain amount at year-end.

Failure to make timely estimated payments often results in underpayment penalties, even when the annual return is filed on time. Understanding how estimated payments work is essential for maintaining consistent compliance.

Payroll and Employment Tax Compliance

Businesses with employees must withhold federal income tax, Social Security, and Medicare taxes, and remit employer contributions. These amounts must be reported accurately and paid on strict schedules.

Payroll tax errors—including late deposits, misclassified workers, or incorrect reporting—can escalate quickly because employment taxes are considered trust fund taxes. The IRS treats these violations seriously and may pursue enforcement actions earlier than with other tax issues.

Sales and Use Tax Responsibilities

Sales tax compliance depends on state law and business activity. Businesses that sell taxable goods or services may be required to collect, report, and remit sales tax. For businesses operating across state lines, compliance becomes more complex due to differing nexus standards.

Sales tax errors often stem from misunderstanding when collection is required or failing to track tax obligations as business operations expand.

Common IRS Penalty Triggers for Small Businesses

Several recurring issues tend to draw IRS attention:

-

Filing returns late or not filing at all

-

Underreporting income or overstating deductions

-

Making late or incomplete payroll tax deposits

-

Failing to respond to IRS notices

-

Poor or missing financial records

Unfiled returns and unresolved balances can compound over time, leading to penalties, interest, and enforcement measures. Businesses facing unresolved tax obligations often encounter issues related to back taxes owed, which can affect credit standing and operational flexibility.

IRS Notices: Why Early Response Matters

IRS notices are often the first indication of a compliance issue. These notices may address discrepancies, missing information, balances due, or proposed adjustments. Ignoring notices can escalate the situation, resulting in liens, levies, or enforced collection.

Businesses that receive audit notices or examination requests should understand the process involved in an IRS audit and gather requested documentation promptly. Early, organized responses can significantly limit exposure and reduce the scope of enforcement.

Recordkeeping as the Foundation of Compliance

Accurate recordkeeping is central to tax compliance. Businesses are expected to maintain documentation supporting income, expenses, payroll, and asset purchases. Common records include bank statements, invoices, receipts, payroll reports, and prior tax filings.

The IRS generally recommends retaining records for at least three years, though longer retention may be required for certain transactions or unresolved issues. Inadequate documentation often leads to disallowed deductions or unfavorable audit outcomes.

Preparing for and Managing Tax Audits

Audits are not always triggered by wrongdoing; many result from automated matching programs or random selection. However, certain factors—such as inconsistent reporting or repeated late filings—can increase audit likelihood.

During an audit, businesses may be asked to substantiate income, expenses, payroll records, or tax positions taken. Businesses involved in complex transactions or restructuring should ensure filings align with applicable business law standards, including those addressed under business law considerations.

Preparation involves maintaining organized records, understanding prior filings, and responding within stated deadlines.

Addressing Tax Debt and Compliance Gaps

When compliance issues result in unpaid balances, addressing them early is critical. Unresolved tax debt can lead to collection actions, including liens and levies. Options for managing tax debt depend on the size of the liability, compliance history, and financial condition of the business.

Businesses navigating unresolved balances may need guidance on managing tax debt and securing relief to stabilize operations and prevent further enforcement.

The Role of Professional Guidance in Compliance

Tax compliance involves ongoing interpretation of regulations, deadlines, and reporting standards. As businesses grow, compliance requirements often become more complex, especially when expanding into new states, hiring employees, or restructuring operations.

Understanding when professional guidance may be appropriate can help prevent inadvertent errors. Businesses seeking broader context on representation and compliance matters may find educational resources available through firms such as The Law Office of Pietro Canestrelli, A.P.C., which focuses on tax and business law issues affecting individuals and organizations.

Long-Term Benefits of Staying Compliant

Consistent tax compliance offers several long-term advantages. Businesses that file accurately and on time typically face fewer audits, reduced penalty exposure, and improved financial predictability. Compliance also supports better cash flow management and facilitates access to financing or business transactions.

Importantly, a strong compliance history allows businesses to respond more effectively when issues do arise, limiting disruption and uncertainty.

Conclusion

Small business tax compliance is not a one-time task but an ongoing process that requires attention, organization, and awareness of evolving obligations. Understanding filing requirements, maintaining proper records, responding promptly to notices, and addressing issues early can significantly reduce the risk of IRS penalties.

By treating compliance as part of overall business risk management, small business owners can protect their operations, maintain stability, and focus on long-term growth.

Κατηγορίες

Διαβάζω περισσότερα

The global healthcare sector is witnessing a significant surge in spinal health awareness, driven by the increasing prevalence of degenerative disc diseases, spinal stenosis, and traumatic spinal injuries. Spinal implants devices used to facilitate fusion, provide structural support, or correct deformities have become essential tools in modern orthopedic and neurosurgery. These...

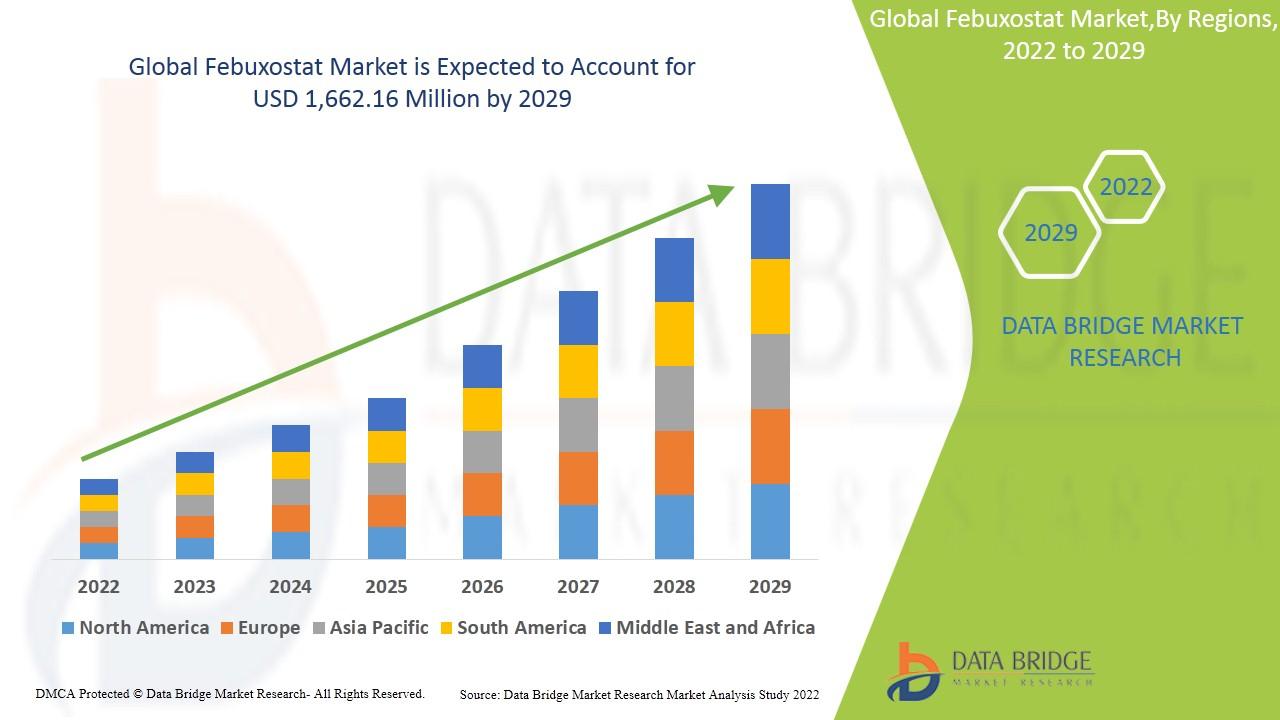

Febuxostat Market: According to the latest report published by Data Bridge Market Research, the Febuxostat Market Febuxostat market is expected to gain market growth in the forecast period of 2022-2029. Data Bridge Market Research analyses the market to account to grow at a CAGR of 7.9% in the above mentioned forecast period and is likely to reach the USD 1,662.16 million by 2029....

Dr. Purodha Prasad emphasizes personalized treatment plans tailored to each patient’s needs. Whether you experience ear pain, muffled hearing, or frequent infections, professional ear cleaning can provide relief. Ear hygiene is essential for overall health and well-being. In Delhi, Dr. Purodha Prasad offers professional ear cleaning services with a focus on safety and...

In today’s fast-paced digital economy, businesses are searching for smarter, faster, and more reliable ways to grow. Data has become the foundation of strategic decision-making, and companies that effectively leverage insights are leading their industries. That’s where Inflectiv comes in. Based in the USA, Inflectiv specializes in turning raw data into actionable strategies that...

ReFirmance is a natural skincare serum designed to support collagen production and improve the appearance of firm, toned skin. It has gained popularity in the USA among individuals looking for a simple yet effective way to address sagging skin, uneven texture, and visible signs of aging without adding complexity to their routine. Commonly applied to the face and neck, it targets areas where...