Passenger Rail Transport Market Landscape: Competitive Strategies and Infrastructure Investment Priorities (2025–2034)

The passenger rail transport market is moving into a new investment-and-modernization cycle as governments, operators, and travelers rebalance mobility priorities toward capacity, reliability, and lower-emissions transport. Passenger rail includes high-speed rail (HSR), intercity services, regional rail, commuter and suburban networks, and metro/urban rail systems, all built on the economic logic of moving large volumes of people efficiently through constrained corridors. Over 2025–2034, the market outlook is expected to remain structurally positive as cities grow, road congestion and airport capacity limits intensify, and public policy continues to favor rail as a decarbonization lever. At the same time, rail’s competitiveness depends on service frequency, punctuality, and door-to-door convenience—pushing operators to invest in digital operations, rolling stock upgrades, station modernization, and customer experience improvements that make rail more attractive versus cars and short-haul flights.

Market overview and industry structure

The Passenger Rail Transport Market was valued at $260.7 billion in 2025 and is projected to reach $493.4 billion by 2034, growing at a CAGR of 7.4%.

Passenger rail is an ecosystem that combines infrastructure owners and managers (track, power, signaling), train operating companies, rolling stock manufacturers, station operators, ticketing and mobility platforms, and a deep maintenance and lifecycle services layer. The sector’s structure varies by region: some markets operate through national incumbents with vertically integrated infrastructure and operations, while others separate infrastructure management from competitive or franchised operators. Core service categories have distinct economics. High-speed rail competes most directly with air on travel times of roughly two to four hours, requiring premium infrastructure, high utilization, and strong scheduling discipline. Intercity and regional rail emphasize connectivity between city pairs and secondary towns, while commuter rail and metro systems prioritize high-frequency peak capacity and dense urban accessibility. Across all segments, reliability, safety, and network coordination are decisive because rail is a “system business”: punctuality and customer satisfaction depend on the weakest link—signals, power, maintenance, staffing, or station flow.

A defining structural shift is digitalization. Passenger rail is increasingly managed through advanced traffic management systems, modern signaling, predictive maintenance, and real-time passenger information. This is not only about operations; it influences revenue through demand forecasting, yield management in premium intercity services, and better incident response that reduces delay penalties and reputational damage. Another important layer is integration with wider mobility systems. In many cities, passenger rail is being positioned as the backbone of multimodal transport, connected to buses, metro lines, park-and-ride facilities, and micro-mobility—supported by integrated ticketing and journey planning.

Industry size, share, and adoption economics

Passenger rail demand is shaped by corridor density, service quality, and pricing versus alternatives. The “adoption” question is less about whether rail exists and more about whether travelers choose it frequently—depending on frequency, punctuality, comfort, onboard connectivity, and station accessibility. In commuter markets, peak reliability and crowding management drive ridership retention. In intercity markets, time-to-destination and ease of travel (boarding time, city-center stations) determine modal share versus flights and cars. The economics of passenger rail are highly sensitive to utilization. High fixed costs in infrastructure and rolling stock mean that adding passengers at the margin can be profitable when capacity exists, but congestion and underinvestment can quickly degrade service and erode demand. This is why many operators prioritize capacity expansion through timetable optimization, longer trains, platform upgrades, and signaling modernization that increases throughput without fully new track builds.

Market share within the passenger rail ecosystem concentrates among operators and suppliers that can deliver performance and lifecycle cost control. Rolling stock procurement increasingly focuses on energy efficiency, reliability, and maintainability, not just upfront price. Operators also lean into service contracts and availability-based maintenance models that transfer uptime risk to manufacturers or specialized service providers. Where private or competitive operators exist, share is influenced by brand, timetable attractiveness, and customer experience features such as guaranteed seating, digital ticketing simplicity, and consistent onboard standards.

Key growth trends shaping 2025–2034

A first major trend is capacity expansion through modernization rather than purely new builds. Many mature networks are investing in signaling upgrades, digital traffic management, and station throughput improvements to increase trains per hour, reduce delays, and improve resilience. A second trend is electrification and energy optimization. Rail already has strong emissions advantages in many contexts, but operators are pursuing further reductions through regenerative braking, lightweight materials, improved aerodynamics, and energy management systems that optimize acceleration and dwell times. In non-electrified corridors, battery-electric and hydrogen trains are emerging as alternatives to diesel, particularly on regional lines where full electrification is costly.

Third, passenger experience is becoming a competitive battleground. Travelers increasingly expect reliable Wi-Fi, comfortable seating, quieter cabins, clean facilities, and intuitive digital interfaces for ticketing and disruption handling. Operators are redesigning timetables and staffing models to improve punctuality, while also investing in station upgrades—wayfinding, security, accessibility, and retail offerings that make rail travel more seamless. Fourth, rail is becoming more integrated with urban development strategies. Transit-oriented development around stations, park-and-ride expansion, and improved feeder services can unlock demand by expanding the rail catchment area. Fifth, automation and data-driven operations are scaling. Predictive maintenance, condition monitoring, and analytics-based asset management reduce failures and improve fleet availability, while real-time crowding tools and demand forecasting help operators allocate capacity more efficiently.

Core drivers of demand

The strongest driver is urbanization and corridor congestion. As cities and regional mega-corridors grow, roads and airports face physical and environmental limits, increasing the value of rail’s high-capacity footprint. A second driver is decarbonization policy. Rail is frequently prioritized in climate strategies, enabling governments to justify investment through emissions reduction, air quality, and energy security benefits. Third, service reliability improvements can create “virtuous cycle” growth: better punctuality and frequency increases ridership, which supports revenue and reinvestment. Fourth, shifting traveler preferences—especially among younger and urban travelers—favor city-center-to-city-center travel, less friction than airports, and the ability to work or relax onboard.

Economic development and regional connectivity are also important drivers. Rail supports labor mobility and tourism, linking secondary cities to major economic centers. In emerging markets, new metro and commuter rail systems are often built to manage urban growth and improve productivity by reducing travel time. In mature markets, upgrading intercity links can strengthen domestic tourism and reduce dependence on short-haul flights.

Challenges and constraints

Passenger rail faces persistent constraints that shape the pace and quality of growth. The largest challenge is capital intensity and long project cycles. Infrastructure upgrades, station rebuilds, and rolling stock procurement require multi-year planning, complex procurement, and political continuity. Operationally, disruptions are highly visible; delays can cascade across networks, and recovery requires strong incident management and communications. Aging infrastructure is another constraint in many regions, where maintenance backlogs create reliability issues and force speed restrictions that reduce capacity.

Labor and skills availability can also become bottlenecks, particularly for drivers, maintenance technicians, signaling engineers, and digital operations talent. Fare affordability and funding models remain sensitive; many systems rely on public subsidies, and balancing financial sustainability with social accessibility is an ongoing policy challenge. Security and safety expectations are rising as well—both physical security in stations and cybersecurity for connected signaling and operational systems. Finally, passenger rail competes with flexible alternatives like cars and ride-hailing; without reliable frequency and last-mile connectivity, rail’s advantages can be diluted, especially in lower-density regions.

Browse more information

https://www.oganalysis.com/industry-reports/passenger-rail-transport-market

Segmentation outlook

By rail type, urban rail and commuter networks remain the largest demand base in dense metropolitan regions, while intercity rail expands where travel times and frequencies are competitive. High-speed rail grows fastest in corridors with strong city-pair demand and supportive policy frameworks. By propulsion, electrified rail continues to dominate new investment priorities, while alternative propulsion (battery or hydrogen) expands on regional lines where decarbonization is needed without full electrification. By service model, integrated multimodal offerings and mobility-as-a-service platforms gain traction where ticketing, scheduling, and real-time information are unified. By customer segment, daily commuters remain foundational, while leisure and business travelers drive premium value in intercity and high-speed services.

Key Market Players

- Central Japan Railway Company

- SNCF

- Deutsche Bahn

- West Japan Railway Company (JR-West)

- Indian Railways

- East Japan Railway Company

- MTR Corporation Ltd.

- Russian Railways

- Canadian Pacific Railway Ltd.

- Union Pacific Corporation

- China Railways

- KiwiRail Ltd.

- PT Kereta Api Indonesia (Persero)

- Abellio ScotRail

- Arriva Rail London

- Avanti West Coast

- Caledonian Sleeper

- Chiltern Railways

- CrossCountry

- East Midlands Railway

- Eurostar

- Govia Thameslink Railway

- Greater Anglia

- Great Western Railway

- Hull Trains

- Grand Central

- Merseyrail

- Virgin Trains

- ScotRail

- London Overground

- Heathrow Connect

- CD Cargo

- Ceské dráhy

- Die Länderbahn

- GW Train Regio

- Emperor Franz Joseph Railway

- Caile Ferate Române

- CFR Marfa

- Regiojet

- Leo Express

- The National Railroad Passenger Corporation (Amtrak)

- Kansas City Southern

- Hudson Bay Railway Co.

- Quebec North Shore and Labrador Railway

- Norfolk Southern Railway

- BNSF Railway

- Companhia do Metropolitano de São Paulo

- Perurail

- Belmond Andean Explorer

- Ferrovías Central Andina

- Nuevos Ferrocarriles Argentinos

- Trenes Metropolitanos

- Brazil Great Southern Railway

- Ferrocarril Transandino

- Saudi Railway Company

- Israel Railways Ltd.

- Iraq Republic Railways Co.

- Middle East Rail

- Turkish State Railways (TCDD)

- Arabian Railway Company

- Egyptian National Railways (ENR)

- Passenger Rail Agency of South Africa (PRASA)

- Transnet SOC Ltd

- Union of African Railways

- Botswana Railways

- Zambia Railways

- National Railways of Zimbabwe

- Nigerian Railway Corporation

Competitive landscape and strategy themes

Competition in passenger rail is shaped less by price wars and more by performance, reliability, and customer trust. Operators differentiate through punctuality, frequency, onboard quality, and disruption handling. Suppliers differentiate through lifecycle cost, availability guarantees, digital diagnostics, and fleet standardization that reduces maintenance complexity. Winning strategies through 2034 are likely to include: modernizing signaling and traffic management to unlock capacity; investing in rolling stock with high reliability and lower energy use; building strong maintenance ecosystems with predictive analytics; expanding integrated ticketing and multimodal partnerships; and improving station experience and accessibility to widen the addressable ridership base.

Regional dynamics (2025–2034)

Asia-Pacific is expected to remain a high-growth engine as rapid urbanization, continued metro expansion, and strong investment in intercity and high-speed corridors increase passenger rail capacity and ridership, supported by large-scale infrastructure programs and rising middle-class travel. North America is likely to see steady growth driven by commuter and regional rail upgrades in major metros, renewed investment in key intercity corridors, and modernization of rolling stock and stations, with progress shaped by funding cycles and project timelines. Europe is expected to maintain robust momentum supported by dense cross-border networks, strong policy backing for rail modal shift, and continued modernization of signaling and interoperability, alongside premium growth in high-speed and night train services in competitive corridors. Latin America offers meaningful upside as metro and commuter rail projects expand to address congestion and improve urban productivity, though funding stability and operational capability will influence outcomes. Middle East & Africa growth is expected to be selective but accelerating, led by new metro systems, intercity rail corridors tied to economic diversification, and major city development programs; successful scaling will depend on long-term operations readiness, talent development, and reliable maintenance ecosystems.

Forecast perspective (2025–2034)

From 2025 to 2034, passenger rail transport is positioned for steady expansion as mobility systems prioritize capacity, resilience, and decarbonization. The market’s center of gravity shifts toward modernization-led performance: increasing throughput on existing networks, improving punctuality, and delivering passenger experiences that reduce friction and strengthen loyalty. Growth will be strongest where investment aligns with operational excellence—modern signaling, well-maintained fleets, integrated ticketing, and stations designed for smooth flow and accessibility. By 2034, passenger rail is likely to be even more digital, more interconnected with broader mobility ecosystems, and more central to national and urban transport strategies—serving as a backbone for efficient, lower-emissions movement of people across the most economically important corridors.

Browse Related Reports

https://www.oganalysis.com/industry-reports/power-train-and-power-train-parts-market

https://www.oganalysis.com/industry-reports/hybrid-train-market

https://www.oganalysis.com/industry-reports/hyperloop-technology-market

https://www.oganalysis.com/industry-reports/hyperloop-train-market

https://www.oganalysis.com/industry-reports/locomotive-maintenance-market

Categorias

Leia mais

The global Fluorspar Market is expected to experience steady growth over the coming decade, supported by rising demand from the chemical, metallurgical, and construction industries. According to recent market insights, the fluorspar market was valued at USD 2.22 billion in 2025 and is projected to reach USD 3.28 billion by 2035, growing at a compound annual growth rate (CAGR) of 3.99%...

A new growth forecast report titled South Korea Ocean Economy Market Size, Share, Trends, Industry Analysis Report By Industry Type (Marine Transport and Shipping, Marine Tourism and Recreation, Fisheries and Aquaculture), – Market Forecast, 2025–2034 introduced by Polaris Market Research represents conclusive data on the overall market. It majorly targets to provide a...

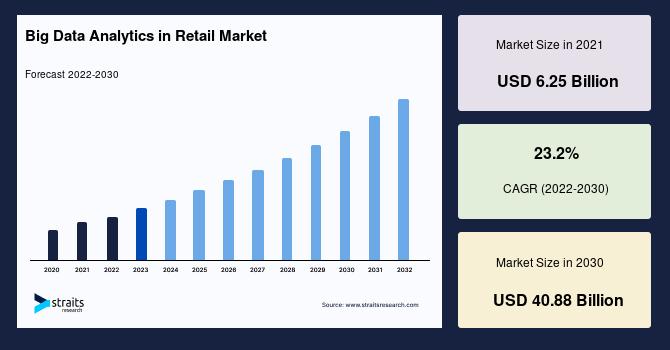

Big Data Analytics in Retail Industry Outlook: Straits Research has introduced a detailed analytical study on the Big Data Analytics in Retail Market, offering insights into market valuation, segmentation framework, and long-term growth trajectory. The publication delivers a structured overview of market drivers, constraints, technological advancements, and strategic developments shaping...

The Science Behind Anti-Aging Skincare Concepts Although BeeTox Wrinkle Face Cream itself is a marketing or product category rather than a scientific term, it is based on well-established cosmetic science principles. Collagen Support in Cosmetics Topical products do not directly replace collagen but may help the skin look firmer by improving hydration and supporting surface elasticity....

Polaris Market Research has published a new report titled Digitally Printed Wallpaper Market Share, Size, Trends, Industry Analysis Report, By Substrate (Nonwoven, Vinyl, Paper, and Others); By Printing Technology; By End-Use Sector; By Region; Segment Forecast, 2023 - 2032 that delivers up-to-date analysis with analyses of the current and future effects of the continuously changing industry...