Vehicle Health Monitoring and Predictive Maintenance: Military Vetronics Market Strategic Insights (2025–2034)

The military vetronics market is entering a reinvention decade as armies modernize armored and tactical vehicle fleets to operate as networked, software-driven combat platforms—while adapting to rapidly evolving threats from drones, precision fires, electronic warfare, and high-tempo multi-domain operations. Vetronics (vehicle electronics) covers the integrated digital backbone inside military vehicles—mission computers, vehicle data buses, power management, communications, navigation, sensors, displays, electronic protection interfaces, turret and fire-control electronics, and health-monitoring systems. As vehicles become increasingly “sensor-and-network centric,” the value equation shifts from simply adding electronics to delivering managed digital performance: secure data sharing, low-latency sensor fusion, resilient connectivity under jamming, cyber-hardened architectures, and upgradeability over long vehicle lifecycles. Between 2025 and 2034, the outlook is expected to remain constructive, supported by large-scale mid-life upgrades, platform recapitalization programs, and the need to integrate counter-UAS and active protection capabilities into vehicle architectures without costly redesign.

Market Overview

The Global Military Vetronics Market was valued at $ 7.01 billion in 2025 and is projected to reach $ 10.73 billion by 2034, growing at a CAGR of 4.85%.

Industry Size and Market Structure

From a market structure perspective, the military vetronics market is a platform-and-mission ecosystem spanning rugged electronics manufacturing, embedded software, system integration, vehicle network architecture, cybersecurity, and lifecycle sustainment. Upstream, value creation begins with suppliers of ruggedized computing modules, processors, displays, vehicle interconnects, wiring harnesses, connectors, sensors, inertial navigation components, antennas, power distribution units, and environmental/EMI shielding solutions designed for shock, vibration, dust, temperature extremes, and electromagnetic stress. Midstream, vehicle OEMs, turret specialists, and defense integrators translate these subsystems into deliverable capabilities—battle management systems, vehicle-to-vehicle and vehicle-to-command connectivity, crew situational awareness suites, driver vision systems, turret and weapon control electronics, electronic countermeasure interfaces, and platform health monitoring. Downstream, the software and sustainment layer becomes a defining differentiator: configuration control, cyber patching, mission system updates, obsolescence management, training and simulation, and readiness services that keep fleets operational over decades. Over the forecast period, value capture is expected to tilt toward providers that combine open, modular vetronics architectures with software-driven integration and sustainment, because customers increasingly buy “assured upgrade pathways and interoperable performance” rather than proprietary one-time electronics installs.

Key Growth Trends Shaping 2025–2034

A defining trend is the acceleration of open architecture vetronics and standardized digital backbones. Armies are moving away from closed, vendor-locked vehicle electronics toward modular computing and network standards that allow new sensors, radios, protection systems, and mission applications to be integrated faster. Common data buses, middleware, and scalable mission computers reduce integration friction, shorten upgrade cycles, and support multi-vendor interoperability across mixed fleets.

Second, sensor fusion and crew-centric situational awareness are becoming the new performance baseline. Vehicles are integrating 360° camera arrays, thermal imaging, laser warning, acoustic shot detection, short-range radar, and external network feeds into a fused operating picture. The key shift is from “more sensors” to actionable decision support—automated cueing, target handoff to weapon stations, and intuitive human-machine interfaces that reduce crew workload in complex environments.

Third, counter-UAS and active protection integration is reshaping vetronics requirements. As loitering munitions and small drones proliferate, vehicles must integrate detection sensors, electronic countermeasures, and hard-kill/soft-kill effectors into the vehicle’s power and data architecture. This increases demand for deterministic, low-latency data exchange, robust safety interlocks, and reliable integration between sensors and effectors—often under severe electromagnetic conditions.

Fourth, resilient communications and contested PNT are becoming core design constraints. Vehicle mission systems increasingly depend on real-time data exchange with dismounted troops, other vehicles, UAVs, and command networks. In jamming-heavy environments, integrated radio suites, smart antenna configurations, network management software, and alternative navigation/timing approaches become essential. This drives growth in integrated communications architectures and vehicle network orchestration that can maintain service continuity and prioritize mission-critical traffic.

Fifth, power and thermal management is moving from an engineering detail to a strategic differentiator. New electronics loads—high-performance processors, sensors, radios, and protection systems—stress vehicle power budgets and heat dissipation limits. Intelligent power distribution, load prioritization, battery management, and advanced thermal solutions support “silent watch,” improve reliability, and enable future upgrades without major redesign.

Finally, health monitoring and predictive maintenance is expanding as readiness becomes a priority. Embedded diagnostics, condition-based monitoring, and fleet analytics help reduce downtime and improve availability by identifying failures early and optimizing spares and maintenance schedules. Over time, this trend strengthens the role of software platforms, data pipelines, and sustainment partners as part of the vetronics value chain.

Core Drivers of Demand

The strongest driver is the need for survivability and faster decision cycles on the modern battlefield. Vetronics enables earlier threat detection, faster engagement decisions, improved coordination with external assets, and tighter integration of protective measures—directly enhancing survivability against drones, precision fires, and ambush threats.

A second driver is the shift to networked ground combat. Armies increasingly require vehicles to operate as connected nodes that share position, sensor tracks, and targeting data with other platforms and command elements. This supports demand for battle management integration, secure communications, interoperable networks, and software-defined upgradeability.

A third driver is the economics of fleet upgrades versus full platform replacement. Many militaries are extending the life of existing armored vehicles through mid-life modernization programs. Vetronics upgrades provide high capability return per dollar, transforming legacy platforms’ effectiveness without needing full chassis replacement.

Finally, cyber resilience and sovereignty priorities encourage investment in secure, trusted architectures—driving demand for hardened computing, secure boot and encryption, and long-term sustainment frameworks.

Browse more information:

https://www.oganalysis.com/industry-reports/military-vetronics-market

Challenges and Constraints

Despite strong fundamentals, the military vetronics market faces constraints that shape execution. The first is integration complexity across legacy fleets. Vehicle platforms often have limited space, weight, and power margin, plus diverse legacy subsystems and wiring. Adding new electronics without causing electromagnetic interference, reliability issues, or maintainability burdens requires disciplined engineering and extensive qualification testing.

Second, cybersecurity is a rising operational risk. As vehicles become software-defined and connected, they also become potential cyber targets. Secure software supply chains, identity and access control, encryption, and continuous patching are increasingly mandatory, expanding program scope and sustainment cost.

Third, obsolescence management is persistent because electronics refresh cycles are far shorter than vehicle service lives. Program success depends on modular designs, stable interfaces, and planned refresh strategies that avoid costly redesigns. Fourth, power and thermal constraints can limit capability insertion pace unless architectures are designed for growth from the start.

Segmentation Outlook

By subsystem category, growth increasingly favors mission computing and open architecture backbones, sensor and situational awareness suites, integrated communications, vehicle power management, and digital interfaces for protection systems and weapon stations. Classic point upgrades—standalone displays or isolated electronics—remain relevant, but momentum shifts toward integrated, software-upgradable architectures.

By application, major demand pools include armored vehicle modernization, tactical vehicle digitization, turret/fire-control electronics integration, counter-UAS and APS integration, and fleet health monitoring and readiness systems. By customer type, long-term value increasingly concentrates in defense forces pursuing multi-year modernization programs and sustainment frameworks that keep mixed fleets interoperable.

By platform approach, the market is expected to see continued demand for comprehensive upgrades of heavy tracked vehicles and IFVs, alongside a growing role for scalable vetronics kits for lighter tactical vehicles and multi-mission platforms where rapid deployment and modularity matter.

Key Market Players

General Dynamics, BAE Systems, Rheinmetall AG, Leonardo, Thales Group, Lockheed Martin, Elbit Systems, Curtiss-Wright, Oshkosh Defense, SAIC, Kongsberg Gruppen, Northrop Grumman, Ultra Electronics, Moog Inc., L3Harris Technologies

Regional Dynamics

North America remains a major vetronics demand center due to large fleet modernization programs, high emphasis on networked operations, and continuous integration of new mission systems. Europe sustains demand through armored fleet recapitalization, interoperability priorities, and heightened focus on contested electromagnetic environments. Asia-Pacific is expected to be a key growth engine through 2034 as regional security drivers accelerate modernization of armored and tactical fleets and expand investment in digitally enabled ground forces. The Middle East & Africa and Latin America offer selective opportunities tied to fleet upgrades, border security, counter-insurgency requirements, and readiness improvements—often favoring modular upgrade packages and sustainment-led models.

Competitive Landscape and Forecast Perspective (2025–2034)

Competition spans vehicle OEMs, defense electronics primes, rugged computing specialists, communications and sensor providers, turret and fire-control suppliers, and systems integrators. Differentiation is increasingly shaped by open architecture compliance, integration speed, cyber resilience, power-aware design, and lifecycle sustainment rather than component performance alone. Winning strategies through 2034 are expected to include: (1) deploying modular, open digital backbones that enable plug-and-play upgrades, (2) strengthening sensor fusion and crew-centric HMI for faster decisions, (3) integrating counter-UAS and active protection through scalable vehicle architectures, (4) delivering resilient communications and PNT solutions for contested environments, and (5) optimizing lifecycle cost through obsolescence management and sustainment-driven readiness services.

Looking ahead, the military vetronics market will remain a foundational layer of ground combat modernization, but its success will increasingly depend on how well architectures adapt to rapid threat evolution and long vehicle lifecycles. The decade to 2034 will reward suppliers and integrators that treat vehicles not as static machines, but as software-enabled mission platforms—delivering secure, interoperable, upgradeable electronics that improve survivability, lethality, and readiness across modern theaters of operation.

Browse Related Reports:

https://www.oganalysis.com/industry-reports/submarines-market

https://www.oganalysis.com/industry-reports/surveillance-radar-market

https://www.oganalysis.com/industry-reports/synthetic-aperture-radar-market

https://www.oganalysis.com/industry-reports/tactical-communication-market

https://www.oganalysis.com/industry-reports/submarine-combat-system-market

Categorii

Citeste mai mult

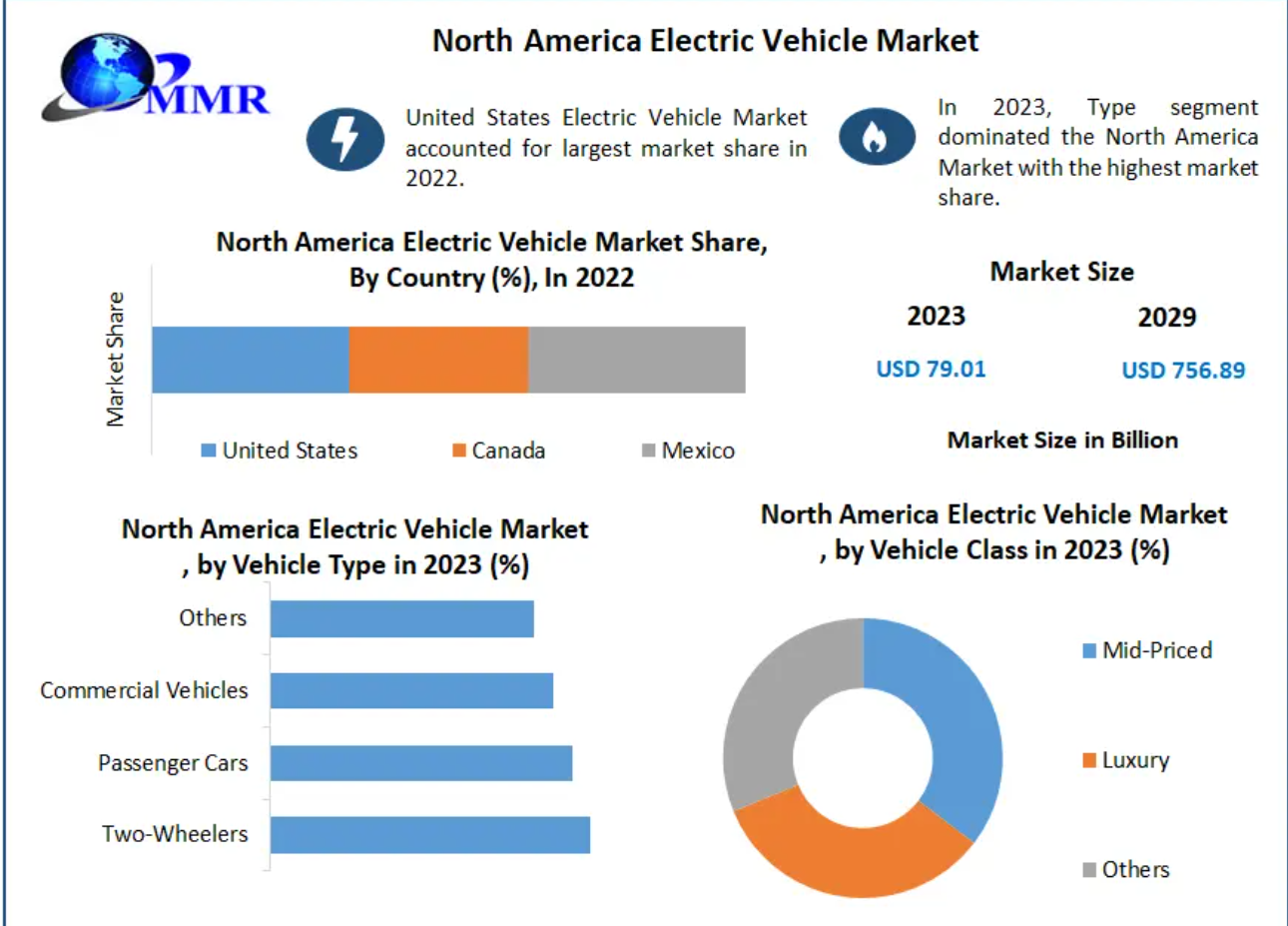

The North America Electric Vehicle Market size was valued at USD 79.01 Billion in 2023 and the total North America Electric Vehicle Market revenue is expected to grow at a CAGR of 38.10 % from 2023 to 2029, reaching nearly USD 756.89 Billion. North America Electric Vehicle Market Overview: Maximize Market Research is a Business Consultancy Firm that has published a detailed...

Advancing Nursing Competencies Through Leadership, Quality Improvement, and Evidence-Based Practice Modern nursing practice demands professionals who are not only skilled in patient care but also capable of applying leadership, quality improvement, and evidence-based practice in clinical settings. Graduate nursing programs emphasize building competencies that allow nurses to make informed...

Nouveau Héros Défensif Un nouveau héros vient d’intégrer la DCE sur FC 26, et cette fois, c’est le défenseur français Dayot Upamecano en version flashback qui fait son apparition. Ce joueur incarne la solidité et la modernité dans la ligne arrière. Doté d’une stature impressionnante, Upamecano est reconnu...

Introduction Dust is present in every home - on floors, furniture, curtains, and even in less visible corners. While often seen as a cleaning concern, it also plays a role in indoor air quality and overall comfort over time. Dust is made up of skin cells, fabric fibers, pollen, soil particles, and fine outdoor pollutants. Because it is lightweight, it can easily become airborne and remain...

Live Chat Skor88 has become an essential feature for users who value instant communication, clarity, and fast responses. In today’s digital environment, people expect immediate answers, whether they are asking about services, features, or technical support. Live chat platforms are no longer optional; they are a necessity. Live Chat Skor88 stands out by offering a smooth and user-friendly...