United States Atherectomy Devices Market Trends and Forecast, 2025–2033

United States Atherectomy Devices Market Outlook: Minimally Invasive Cardiac Care Driving Steady Expansion

The United States atherectomy devices market is set for robust growth over the next decade, reflecting the country’s rising cardiovascular disease burden and the healthcare system’s strong shift toward minimally invasive interventions. The market is projected to expand from US$ 316.05 million in 2024 to US$ 627.59 million by 2033, registering an impressive compound annual growth rate (CAGR) of 7.92% during 2025–2033.

This expansion is being driven by increasing incidence of peripheral artery disease (PAD) and coronary artery disease, continuous technological advancements in plaque-removal systems, favorable reimbursement policies, and growing physician and patient preference for procedures that reduce hospital stays and recovery time while improving clinical outcomes.

Atherectomy devices have become an integral component of interventional cardiology and vascular surgery in the U.S., particularly for complex, calcified, or long-segment lesions that are difficult to manage using balloon angioplasty or stenting alone.

Download Free Sample Report:https://www.renub.com/request-sample-page.php?gturl=united-states-atherectomy-devices-market-p.php

United States Atherectomy Devices Market Overview

Atherectomy devices are specialized medical tools used to treat atherosclerosis, a condition characterized by plaque buildup within arterial walls that restricts blood flow and increases the risk of heart attack, stroke, and limb ischemia. These devices are designed to remove, shave, grind, or vaporize plaque, restoring vessel patency and improving circulation.

In the United States, atherectomy is widely used in percutaneous coronary interventions (PCI) and peripheral artery interventions (PAI). The technology is often employed alongside angioplasty and stenting to improve procedural success, particularly in patients with heavily calcified or complex lesions.

Several types of atherectomy devices are available, including:

· Directional atherectomy, which selectively cuts plaque from specific arterial areas

· Rotational atherectomy, which uses a high-speed rotating burr to grind calcified plaque

· Orbital atherectomy, which sands plaque using an eccentrically rotating crown

· Laser atherectomy, which vaporizes plaque using high-energy laser pulses

Together, these technologies play a critical role in managing coronary artery disease and peripheral vascular disease, helping reduce symptoms, improve quality of life, and lower the risk of severe cardiovascular events.

Growth Drivers in the United States Atherectomy Devices Market

Rising Incidence of Peripheral Artery Disease and Cardiovascular Disorders

One of the most powerful drivers of the U.S. atherectomy devices market is the growing prevalence of PAD and other cardiovascular diseases. PAD alone affects more than 12 million Americans, with many cases remaining undiagnosed until advanced stages. Aging demographics, obesity, diabetes, smoking, and sedentary lifestyles are accelerating the incidence of vascular disease across the country.

As PAD and coronary artery disease cases rise, the need for advanced plaque-modifying technologies grows in parallel. Atherectomy devices are increasingly favored for their ability to treat complex lesions while avoiding open surgery. Demand is particularly strong for procedures that reduce hospitalization time and enable faster patient recovery, aligning well with modern value-based healthcare models.

Technological Advancements in Atherectomy Devices

Ongoing innovation is transforming atherectomy technology and driving adoption across U.S. hospitals and specialty clinics. Modern devices now offer enhanced plaque-removal efficiency, improved catheter flexibility, real-time imaging integration, and reduced complication rates.

Laser and orbital atherectomy systems, in particular, have gained traction for their precision and safety in treating heavily calcified lesions. Advances in device ergonomics and portability are also expanding usage in outpatient and ambulatory care settings. Strong investment in R&D by leading medical device companies continues to fuel competitive product launches and broaden clinical applications, increasing physician confidence and patient demand.

Expansion of Reimbursement and Insurance Coverage

The U.S. reimbursement environment has become increasingly supportive of atherectomy procedures, especially for PAD and complex coronary interventions. Medicare and private insurers recognize atherectomy as a clinically valuable treatment option, reducing financial barriers for patients and providers alike.

Improved reimbursement has encouraged hospitals and clinics to invest in advanced atherectomy platforms, knowing that procedural costs are more likely to be covered. This has been particularly impactful for elderly patients, who represent a large share of PAD cases and depend heavily on Medicare coverage. Favorable reimbursement trends continue to accelerate adoption and expand patient access to minimally invasive cardiovascular care.

Challenges in the United States Atherectomy Devices Market

High Device and Procedure Costs

Despite strong clinical demand, the high cost of atherectomy devices and procedures remains a significant challenge. Advanced atherectomy systems require substantial capital investment, along with ongoing expenses for disposable components. Even with insurance coverage, patient out-of-pocket costs can be considerable, potentially limiting utilization.

Healthcare providers also face cost-containment pressures, particularly in smaller or resource-limited facilities. Without further reductions in device pricing or continued reimbursement expansion, cost concerns may slow penetration in certain regions despite clear clinical benefits.

Procedural Risks and Shortage of Skilled Professionals

Although atherectomy techniques have advanced, procedures still carry inherent risks such as arterial perforation, distal embolization, restenosis, and vascular injury. Successful outcomes depend heavily on operator expertise, making access to highly trained interventional cardiologists and vascular surgeons essential.

A shortage of experienced specialists—particularly in rural and underserved areas—can limit broader adoption. Training programs require time and investment, and concerns about patient safety may lead some physicians to be cautious with specific atherectomy technologies. Continued innovation to reduce procedural risk, combined with expanded training initiatives, will be critical to overcoming these barriers.

Market Insights by Product Type

Directional Atherectomy Devices Market

Directional atherectomy devices are gaining significant traction in the U.S. due to their ability to selectively remove plaque while preserving healthy vessel tissue. Physicians favor these devices for treating eccentric, calcified, or complex lesions. Integration of real-time imaging and improved catheter designs has enhanced precision and clinical outcomes. Strong reimbursement support and widespread use in PAD treatment make this segment a key growth driver.

Laser Atherectomy Devices Market

Laser atherectomy represents one of the fastest-growing segments, valued for its ability to vaporize plaque with minimal mechanical stress on vessel walls. These devices are particularly effective in treating in-stent restenosis and complex lesions. Advances in laser technology have improved safety and usability, driving adoption in hospitals and ambulatory surgical centers. Continued innovation positions laser atherectomy for expanding market share.

Market Insights by Application

Cardiovascular Atherectomy Devices Market

Cardiovascular applications dominate the U.S. atherectomy market, reflecting the country’s high burden of coronary artery disease. Atherectomy is increasingly used alongside balloon angioplasty and stenting to improve long-term outcomes in high-risk patients. Aging demographics, widespread screening, and strong clinical evidence supporting plaque modification continue to drive growth in this segment.

End-User Analysis

Hospitals

Hospitals account for the majority of atherectomy procedures in the United States. Their advanced infrastructure, access to specialized clinicians, and ability to manage complex cases make them the primary adopters of atherectomy technology. Hospitals often maintain multiple device platforms, allowing physicians to tailor treatment strategies to individual patients. Participation in clinical research and strong reimbursement relationships further reinforce hospital dominance.

State-Level Market Overview

California Atherectomy Devices Market

California is one of the largest state-level markets, supported by its extensive healthcare network, leading research institutions, and high prevalence of cardiovascular disease. The state’s strong medical device ecosystem and high patient awareness drive early adoption of advanced atherectomy technologies.

New York Atherectomy Devices Market

New York’s dense population, sophisticated hospital systems, and high incidence of PAD and diabetes fuel demand for atherectomy procedures. Major hospitals act as referral centers for complex cases, supporting continued adoption and innovation.

New Jersey Atherectomy Devices Market

New Jersey is a steadily growing market, driven by an aging population and rising lifestyle-related cardiovascular conditions. Proximity to major medical hubs and expanding insurance coverage support increasing use of atherectomy devices in hospitals and specialty clinics.

Competitive Landscape and Key Players

The U.S. atherectomy devices market is highly competitive, characterized by continuous innovation and strategic investments. Key players include Boston Scientific Corporation, Abbott Laboratories, Medtronic plc, Cardinal Health, Terumo Corporation, AngioDynamics Inc., and Becton, Dickinson and Company.

These companies compete through technological differentiation, expanded indications, and strong physician training programs to strengthen their market positions.

Final Thoughts

The United States atherectomy devices market is on a strong growth trajectory, supported by rising cardiovascular disease prevalence, rapid technological innovation, and increasing demand for minimally invasive treatment options. While challenges related to cost, procedural risk, and workforce availability remain, ongoing advancements in device design and supportive reimbursement policies continue to expand adoption.

With the market expected to reach US$ 627.59 million by 2033, atherectomy devices will remain a critical component of advanced cardiovascular care in the U.S. For device manufacturers, healthcare providers, and investors, the coming decade offers significant opportunities to improve patient outcomes while participating in one of the most dynamic segments of interventional medicine.

Categories

Read More

The IPL season is full season and the current RCB vs SRH competition is creating sensations among the fans. Both teams have been presenting high intensity cricket with fierce batting, disciplined bowling and random leather twists that define this years tournament. As each of the over has been bringing out new suspense, the match is so far one of the most watched games currently. Since the fans...

Polaris Market Research has announced the latest report, namely EdTech and Smart Classroom Market Share, Size, Trends, Industry Analysis Report, By Hardware (Interactive Projectors, Interactive Displays, Others); By Education System; By Technology (Gamification, Analytics, Enterprise Resource Planning, Security, Advanced Technology); By End-Use (Kindergarten, K-12, Higher Education); By...

An Armature For Power Tools is a core component within electric motors, playing a crucial role in converting electrical energy into mechanical motion. Found in tools such as drills, grinders, and saws, the armature directly influences performance, efficiency, and reliability. Understanding how an Armature For Power Tools functions can help users and manufacturers ensure consistent...

Packaging is a vital part of product presentation in the personal care industry, especially for soaps. Custom die cut soap boxes offer a creative and professional way to package soaps while keeping them safe and visually appealing. These boxes stand out on retail shelves and help brands leave a lasting impression on customers. One of the main advantages of die cut soap boxes is their...

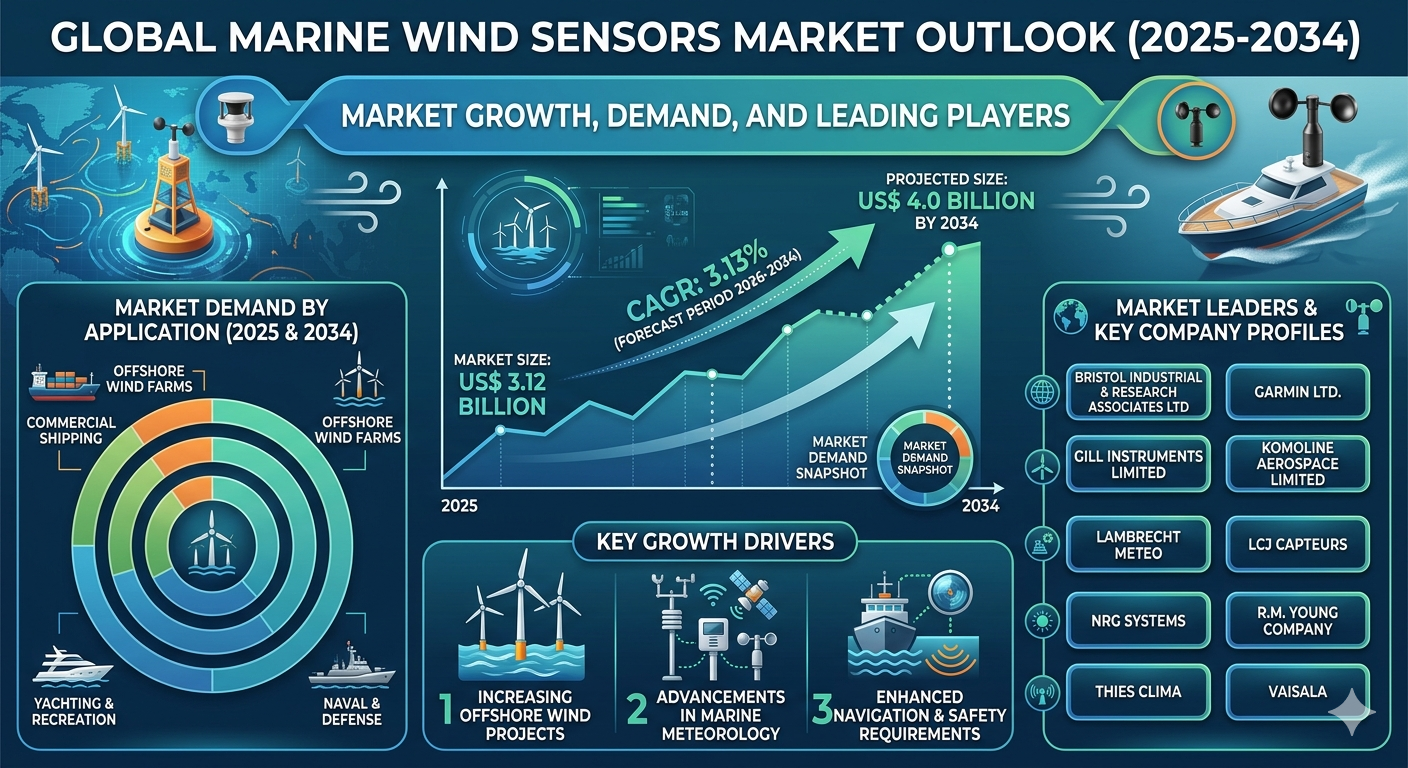

The marine industry is rapidly embracing advanced sensing technologies to improve navigation safety, fuel efficiency, and operational performance. Wind sensing systems have become a critical component across commercial shipping vessels, yachts, naval fleets, and offshore platforms. Increasing maritime activities, rising investments in smart navigation systems, and the expansion of offshore...