5G Chipset Market Size, Industry Growth | 2035

Despite its powerful growth trajectory and immense strategic importance, the 5G Chipset Market Restraints are significant and can create substantial challenges for vendors and the broader ecosystem. The single most significant and persistent restraint is the immense technological complexity and the astronomical cost of research and development (R&D). Designing a state-of-the-art 5G chipset that is competitive at the highest level is one of the most challenging engineering feats in the modern world. It requires deep expertise across a wide range of disciplines, from digital signal processing and RF engineering to computer architecture and low-power design. The cost of designing a single, leading-edge SoC can run into the hundreds of millions of dollars, and the cost of the sophisticated electronic design automation (EDA) software tools required is also immense. This massive and front-loaded R&D investment is a formidable barrier to entry, which is why there are only a handful of companies in the world that can compete at the top tier of the market. This technological complexity and high cost is a major restraint that stifles competition and concentrates market power. The 5G Chipset Market industry is projected to grow to USD 60.0 Billion by 2035, anticipated CAGR of 20.59% during forecast period 2025- 2035.

A second major restraint is the market's profound and unavoidable dependence on a highly concentrated and geopolitically sensitive manufacturing supply chain. While many companies can design a chip, only a very small number of companies in the world—primarily TSMC in Taiwan and Samsung in South Korea—possess the cutting-edge semiconductor fabrication plants (fabs) that can manufacture these advanced 5G chipsets at the most leading-edge process nodes (e.g., 5nm and below). This creates a massive bottleneck and a single point of failure for the entire industry. This manufacturing dependency is a major restraint for several reasons. It gives the foundries immense pricing power. It also makes the entire 5G ecosystem highly vulnerable to any disruption in this concentrated supply chain, whether it's a natural disaster, a factory fire, or, increasingly, a geopolitical event. The strategic importance of Taiwan in the global semiconductor supply chain is a particularly acute point of concern and a major potential restraint on the market's stability.

The third, and increasingly critical, restraint revolves around the complexities of spectrum availability and the slower-than-expected rollout of some of the key features of 5G, particularly in the millimeter wave (mmWave) band. The full promise of 5G's multi-gigabit speeds is heavily dependent on the use of high-frequency mmWave spectrum. However, the rollout of mmWave has been slower and more challenging than initially anticipated. These high-frequency signals have a very short range and are easily blocked by obstacles, which requires the deployment of a very dense network of small cells, a costly and time-consuming process. The availability of licensed mmWave spectrum also varies dramatically from one country to another. This slower and more patchy rollout of the "high-performance" version of 5G is a restraint on the demand for the most advanced and expensive mmWave-capable chipsets. Similarly, the widespread adoption of the other key pillars of 5G, like URLLC and mMTC, is still in its early stages, which can limit the demand for the specialized chipsets designed for these use cases.

Top Trending Reports -

Κατηγορίες

Διαβάζω περισσότερα

Anderson Wins Oscar The Oscar Triumph of Wes Anderson's Henry Sugar Adaptation In a career-defining moment, acclaimed director Wes Anderson has finally claimed his first Academy Award. After eight previous nominations, Anderson's adaptation of "The Wonderful Story of Henry Sugar" secured the Oscar for Best Live Action Short Film at the 96th ceremony. This victory represents just one component...

"Global Executive Summary Asia-Pacific Ophthalmology Market: Size, Share, and Forecast The Asia-Pacific ophthalmology market is expected to reach USD 28.23 billion by 2032 from USD 15.84 billion in 2024, growing at a CAGR of 7.5 % in the forecast period of 2025 to 2032. This Asia-Pacific Ophthalmology Market research report contains specific segments by type and by application. Each type...

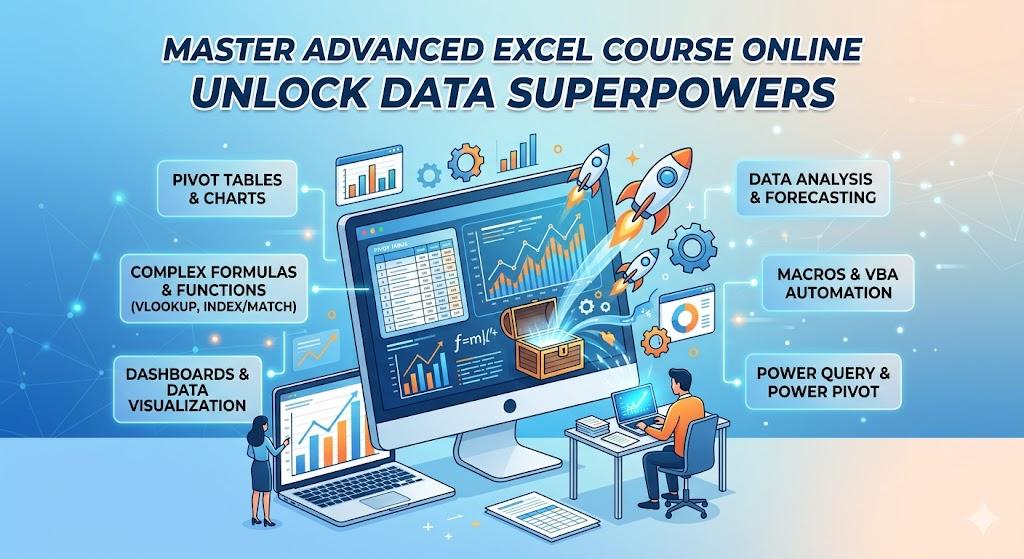

Master Advanced Excel Course Online to automate reports, analyze data, and boost your career. Find expert-led training & Online Certification Courses to get hired faster. Microsoft Excel — The King of the Spreadsheet World In a data driven economy of today, there has not been any competition to Microsoft Excel. Applying to financial modelingAnd inventory trackingFrom sales...

Season 5 of Marvel Rivals has introduced new characters like Gambit and Rogue, marking an exciting development for players. This season's theme revolves around love and relationships, which has resonated well with the gaming community, especially after the fan-favorite pairing of Loki and Mantis was officially recognized within the game. Despite the focus on romantic bonds, fans have quickly...

The Academy is a specialized facility that becomes accessible once your town center reaches level 9. It serves as a hub for technological advancement, allowing you to explore various upgrade paths to enhance your city’s capabilities. Within the Academy, research options are categorized into three main areas: Growth, Economy, and Battle. Each category offers unique benefits tailored to...