Do tax accountants help with crypto taxes in Manchester?

The Manchester edge for crypto taxpayers in 2026

Picture this: you’ve spent the last year trading Ethereum on a decentralised exchange, staking in a liquidity pool, and maybe even accepting a bit of Bitcoin as payment for freelance work in Manchester’s tech scene. Come January 2027, HMRC’s new data feeds from UK crypto platforms will land on their desks – and suddenly your Self Assessment looks a lot more exposed. That’s exactly where a local tax accountant steps in, not just to file the return, but to make sure you’re not paying a penny more than you legally owe.

I’ve been advising UK taxpayers and business owners for over 18 years, and the last five have been dominated by crypto queries from clients right here in Greater Manchester. The rules are national, yet the value of a Manchester-based adviser is tangible. Face-to-face meetings in Deansgate or Spinningfields beat endless Zoom calls with London firms. We understand the Northern tech and creative businesses that often mix crypto with property, dividends or side hustles. And crucially, we catch the nuances that generic online calculators miss.

None of us enjoys tax surprises, especially when HMRC’s Cryptoasset Reporting Framework goes live on 1 January 2026. UK exchanges must now collect your National Insurance number, address and transaction history and pass it to HMRC, with the first bulk reports due in May 2027. A good accountant helps you prepare clean records now so that when the nudge letter arrives you can respond confidently rather than panic.

How we turn complex rules into clear action for 2025/26

Let’s be honest – the 2025/26 tax year brings sharper teeth to crypto taxation. Capital Gains Tax (CGT) on disposals sits at 18% for basic-rate taxpayers and 24% for higher- or additional-rate taxpayers after the £3,000 annual exempt amount. That’s a big jump from the old 10%/20% regime that applied before October 2024.

Crypto received as income – staking rewards, mining payouts, airdrops or DeFi lending interest – is taxed at your marginal income-tax rate (20%, 40% or 45%) once it exceeds the £1,000 miscellaneous income allowance. The value at receipt becomes your base cost for future CGT. Get the classification wrong and you could face an enquiry plus penalties.

A Manchester accountant doesn’t just crunch the numbers; we verify your exchange exports against HMRC’s pooling rules. Same-type tokens (all your ETH, for example) sit in a single pool with an average cost. Sell 200 tokens out of 500 and we deduct the proportional cost – not FIFO or LIFO unless the 30-day rule kicks in. I’ve seen clients save thousands simply by applying the correct allowable costs: platform fees, gas, even valuation reports when gifting to family.

We also check interactions with other income. A Manchester freelancer earning £45,000 salary plus £12,000 crypto staking rewards suddenly sits in the higher-rate band. That pushes part of their CGT to 24% instead of 18%. Spotting this early lets us plan spousal transfers or timing of disposals to stay in the basic band where possible.

Real value: verification, correction and peace of mind

Most clients arrive convinced their spreadsheet is fine. Within an hour we usually find three issues: missing pool adjustments, forgotten transaction fees, or gains reported in USD instead of sterling. One client last year overpaid by £4,800 because he treated every swap as a separate disposal without pooling – we corrected it via an amended return and reclaimed the overpayment with interest.

For business owners the stakes are higher. If your crypto activity looks like a trade (frequent, organised, financed by borrowing, aimed at profit), profits are subject to income tax or corporation tax at 19–25% instead of CGT. We review the “badges of trade” against HMRC’s Cryptoassets Manual and help you document investment intent if that’s the reality. Many Manchester Ltd companies now run crypto treasury operations; we advise on extracting profits tax-efficiently and whether Making Tax Digital for Income Tax Self Assessment (phased from 2026) will apply to your crypto side hustle.

Scottish and Welsh clients get an extra layer. Income-tax bands differ north of the border, which can affect which CGT rate slice applies. We run the exact calculation so you don’t inadvertently trigger the 24% rate on a disposal that would have been 18% under English rules.

Be careful here: high-income child benefit charge still applies if adjusted net income exceeds £60,000. Crypto gains and staking income both count. I’ve had clients in Didsbury lose thousands in withdrawn child benefit because they forgot to include a large airdrop.

CGT rates and allowance 2025/26 (England, Wales, NI – other assets including crypto)

|

Taxpayer status |

Rate |

Annual exempt amount |

|

Basic-rate band |

18% |

£3,000 |

|

Higher/additional-rate |

24% |

£3,000 |

(Trustees pay 24%. Carried interest 32%. Residential property higher but crypto is “other” assets.)

Why DIY tools and generic calculators fall short

Online platforms spit out nice PDFs, yet they rarely handle the £1,000 miscellaneous allowance correctly, or spot when staking rewards should be valued at receipt for both income and base cost. They certainly don’t advise on loss harvesting across tax years or offsetting crypto losses against property gains.

A proper accountant builds a permanent tax file: every wallet address, every transaction hash cross-referenced to sterling values on the exact date (using HMRC’s acceptable sources or reputable exchanges). When HMRC asks for evidence under CARF, you hand over a neatly indexed folder instead of scrambling.

I’ve sat with clients who received “nudge” letters in 2025 and thought they were fine because “the exchange sent data”. The exchange data is raw; it doesn’t prove your allowable costs or your non-trading intention. That’s where 18 years of dealing with HMRC compliance teams makes the difference.

Practical checklist every Manchester crypto taxpayer should use before 31 January 2027

-

Download every transaction report in CSV from every platform and wallet for 6 April 2025 – 5 April 2026.

-

Convert all values to sterling on the exact date of each disposal or receipt using reputable sources.

-

Calculate each pool’s average cost before and after every disposal.

-

List all income events (staking, mining, airdrops) and confirm they fall under miscellaneous or trading income.

-

Reconcile total gains against your other income to confirm the correct CGT rate slice.

-

Check for spousal transfers or losses carried forward that can shelter gains.

-

Prepare a covering note explaining any large one-off events (inheritance, employment bonus paid in tokens).

-

File via Self Assessment using the new dedicated cryptoasset pages – don’t bury them in “other gains”.

Run this checklist yourself and you’ll sleep better. Better still, hand it to your accountant and let us stress-test it.

When crypto meets other income streams – the multi-job reality

Many Manchester clients juggle PAYE jobs, property rentals and crypto. Emergency tax codes hit hard when employers pay bonuses in tokens. We’ve corrected dozens of over-withheld PAYE by filing the correct Self Assessment and claiming refunds within the four-year window.

High earners above £100,000 see personal allowance taper – £1 lost for every £2 of adjusted net income. Crypto staking can easily tip you over. One Salford client in 2025 lost £2,500 of allowance because he forgot to include £18,000 of DeFi rewards. We spotted it, amended the return and saved him the tax plus restored his full allowance.

Business structures that actually work in 2026

If your crypto activity is significant, running it through a limited company can cap corporation tax at 19% on profits up to £50,000 (marginal relief to 25%). Dividends then attract the £500 allowance and 8.75%/33.75% rates. We model both personal and corporate scenarios for Manchester clients launching NFT projects or running validator nodes.

VAT is another trap. Most crypto supplies are exempt, but advisory fees or certain exchange services may be standard-rated. We ensure your invoices are correct and reclaim input VAT where possible.

DeFi, staking and the wait for legislative clarity

Current HMRC guidance treats transferring tokens to a DeFi lending protocol as a disposal for CGT, with rewards taxed as miscellaneous income. The 2025 consultation on “no gain, no loss” treatment for certain DeFi arrangements is still under review as of February 2026 – no legislation yet. We advise clients to record the market value at the exact moment of transfer and keep evidence in case rules change retrospectively.

Two real client stories that illustrate the stakes

First, a Manchester software engineer who mined Ethereum in 2024 and treated every block reward as capital. HMRC opened an enquiry in late 2025. We reclassified the mining as miscellaneous income, claimed the £1,000 allowance, carried forward losses correctly and negotiated a penalty reduction from 30% to 10% on the grounds of reasonable care after taking professional advice.

Second, a married couple in Chorlton with £180,000 combined gains in 2025/26. Without planning they faced 24% on most of it. We used spousal transfers, crystallised losses from previous years and timed one disposal into the basic-rate band, saving £9,400. All perfectly legitimate and fully documented.

These aren’t cherry-picked; they’re typical of the cases that cross my desk every week.

Preparing for the CARF data tsunami

From 1 January 2026 every UK-resident user of a crypto service provider must supply accurate name, address, date of birth and tax identification number. Get it wrong and you risk penalties or blocked accounts. We help clients update their profiles now and draft a simple one-page summary they can hand to every platform.

When the 2027 reports hit HMRC, expect more automated enquiries. Having an accountant who already holds your full transaction history means we can respond within days rather than weeks.

Tax-saving opportunities still available in 2026

-

Bed-and-ISA is not possible for crypto, but gifting to a spouse who then uses their own £3,000 allowance is.

-

Crystallise losses before 5 April each year to offset future gains.

-

Consider Enterprise Investment Scheme or Seed EIS if you want to reinvest crypto profits into qualifying UK startups – 30% or 50% income-tax relief plus CGT deferral.

-

For business owners, pension contributions reduce adjusted net income and can restore personal allowance or avoid child-benefit charge.

None of these is aggressive; they are the planning steps I give every paying client.

The First-tier Tribunal perspective – what HMRC really tests

Although few published FTT decisions deal purely with crypto yet, the principles are clear from asset cases. Tribunals examine evidence of trading intention: frequency, organisation, financing, profit motive. They also look at whether you took reasonable care – and professional advice counts heavily when penalties are in play.

I’ve represented clients at compliance meetings where HMRC initially demanded 100% penalties. Once we produced contemporaneous notes showing we advised on pooling and valuation, the penalty dropped to 10% careless. That experience is gold when you face an enquiry.

Your next steps – practical and immediate

-

Gather every 2025/26 transaction file today.

-

Book a no-obligation review with a qualified crypto-savvy accountant in Manchester – ask for their ICAEW or ATT crypto CPD record.

-

Run the eight-point checklist above.

-

If gains exceed £3,000 or income exceeds £1,000 miscellaneous, register for Self Assessment by 5 October 2026 if not already registered.

-

Keep the sterling valuation evidence organised by tax year.

-

Consider quarterly reviews if your activity is frequent.

-

Discuss business incorporation if turnover approaches £50,000 or profits are material.

-

Update every exchange profile with correct UK tax details before 31 December 2026.

-

Ask your accountant to model three scenarios: all personal, spousal split, corporate wrapper.

-

Sleep easy knowing your records will withstand any CARF-driven enquiry.

Summary of Key Insights

-

Manchester accountants deliver the same national expertise with local convenience and faster response times.

-

CGT is 18%/24% after £3,000 allowance; income from staking/mining hits your marginal rate after the £1,000 allowance.

-

Pooling rules and sterling valuation on every event are non-negotiable – DIY tools miss them.

-

CARF data sharing from January 2026 means HMRC will see far more crypto activity; clean records are your best defence.

-

Multi-source income changes your tax band – always model the full picture.

-

DeFi and staking currently trigger disposal plus income events; watch for possible no-gain-no-loss legislation.

-

Trading classification can move you from 24% CGT to 45% income tax – document investment intent carefully.

-

Spousal transfers, loss crystallisation and pension contributions remain powerful, legal shelters.

-

Professional advice demonstrably reduces penalties at Tribunal level.

-

Start your 2025/26 record review now; the 31 January 2027 deadline will arrive faster than Bitcoin hits a new all-time high.

There you have it – practical, up-to-date guidance for the 2025/26 tax year that goes far beyond the basics. If your crypto portfolio is growing or you’ve received any HMRC correspondence, the smartest move is to speak to a qualified local accountant who lives and breathes these rules every day. Your wallet – and your peace of mind – will thank you.

Категории

Больше

Streetwear has become one of the strongest influences in today’s fashion industry, completely transforming how individuals approach personal style and everyday dressing. What originally developed through skateboarding culture, hip-hop communities, and underground urban scenes has now evolved into a worldwide fashion movement embraced across different lifestyles and generations. Modern...

Introduction to ISO Certification in Healthcare ISO certificering zorg (ISO certification in healthcare) refers to implementing internationally recognized standards to improve the quality, safety, and efficiency of healthcare services. Healthcare organizations, including hospitals, clinics, and laboratories, adopt ISO standards to ensure consistent patient care and compliance with...

Thread cutting uses CNC machines and threading inserts to make accurate internal and external threads with correct shape, pitch, smooth finish, and long tool life What Is a Threading Insert? A threading insert is a small cutting tool used to make threads on metal parts during machining. It is fitted into a tool holder and used on lathes or CNC machines to cut internal or external threads with...

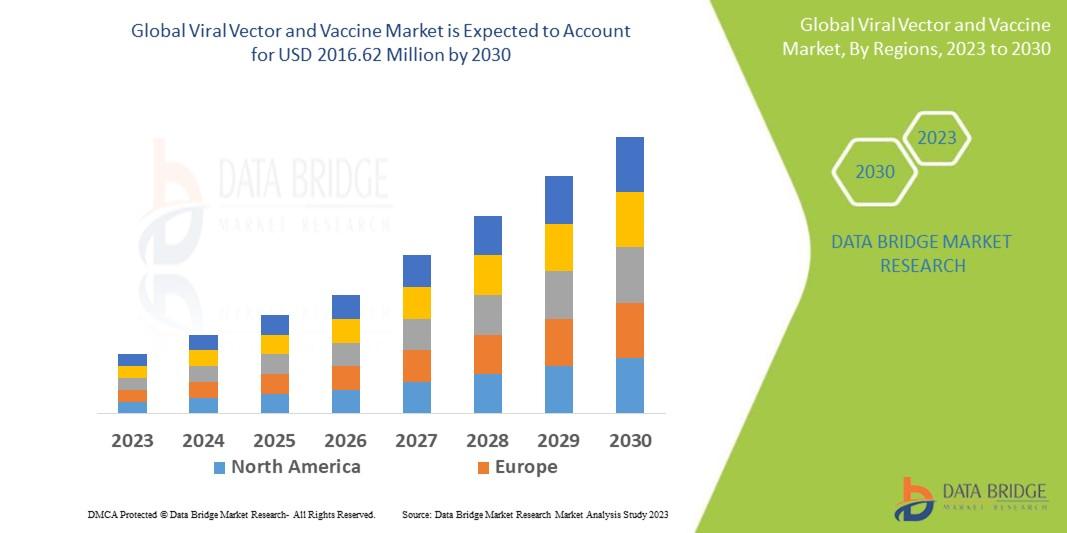

"Executive Summary Viral Vector and Vaccine Market Size and Share Across Top Segments Data Bridge Market Research analyses that the viral vector and vaccine market which is USD 513.43 million in 2022, is expected to reach USD 2016.62 million by 2030, at a CAGR of 18.65% during the forecast period 2023 to 2030.To better structure this Viral Vector and Vaccine report, a nice blend of...

By 2026, capital markets are no longer being reshaped by loud disruption narratives or speculative hype cycles. Instead, a quieter and far more strategic transformation is underway. Institutional investors, sovereign funds, private equity firms, and family offices are reallocating capital toward digital infrastructure that enhances liquidity, transparency, and control. At the center of this...