Psychology Meets Numbers: Fibonacci Methods for Financial Discipline

The Psychology of Spending plays a critical role in financial discipline. Many people struggle with controlling their money not because of income limits but due to behavioral patterns, emotional triggers, and cognitive biases. By combining psychological insights with Fibonacci methods, spending and budgeting can be structured to promote long-term financial stability while aligning with human behavior.

Understanding Behavioral Spending

Spending habits are often shaped by emotional and social influences rather than rational planning. Impulse purchases, peer pressure, and the desire for instant gratification can lead to financial stress. Recognizing these patterns is the first step in gaining control. Fibonacci methods provide a structured framework that allows spending to be divided proportionally, making it easier to manage emotions and maintain financial discipline.

Fibonacci Ratios in Budget Allocation

The Fibonacci sequence—1, 2, 3, 5, 8, 13—represents a natural and visually appealing progression. In budgeting, it can guide the allocation of income to essential expenses, savings, discretionary spending, and debt repayment. Larger proportions can be allocated to necessities, medium amounts to savings or investments, and smaller portions to discretionary spending. This proportional system promotes balanced decision-making and reduces the psychological stress often associated with budgeting.

Controlling Emotional Spending

Emotional spending is one of the main reasons budgets fail. Stress, excitement, and social influence can drive impulsive purchases. Fibonacci budgeting allows discretionary spending to be split into smaller, incremental portions. This method satisfies emotional needs without undermining overall financial goals, aligning spending behavior with both rational planning and emotional satisfaction.

Gradual Habit Formation

Sustainable financial habits develop best through incremental changes rather than drastic measures. Fibonacci methods naturally support this process. By gradually adjusting spending and savings allocations according to the sequence, individuals reinforce positive habits without feeling deprived. Over time, these incremental changes become automatic, leading to lasting financial discipline.

Prioritizing Needs and Wants

Effective budgeting requires prioritization. Using Fibonacci ratios, essential expenses such as rent, utilities, groceries, and debt repayment receive larger allocations, while discretionary spending and luxury items are proportionally smaller. This ensures that critical financial obligations are consistently met while still allowing room for controlled indulgences. The psychological satisfaction of meeting priorities reinforces disciplined spending.

Tracking and Adjusting Spending

Monitoring spending is essential for maintaining control and making informed adjustments. Fibonacci-based allocations create clear benchmarks, making it easier to spot deviations. Minor adjustments can restore balance without disrupting overall financial stability. This structured approach encourages mindfulness and accountability, reinforcing positive spending habits over time.

Counteracting Cognitive Biases

Cognitive biases such as overconfidence, optimism bias, and impulsivity can disrupt financial plans. Fibonacci methods provide a proportional framework that reduces the influence of these biases. Incremental allocations prevent impulsive decisions and promote rational, consistent financial behavior. Integrating behavioral insights with structured planning enhances both discipline and psychological satisfaction.

Everyday Applications

Fibonacci principles can be applied to everyday financial decisions. Groceries, utilities, transportation, and entertainment can all follow proportional allocations based on the sequence. This prevents overspending, improves financial awareness, and aligns daily habits with long-term goals. Structured, incremental spending allows individuals to enjoy their money while maintaining control and discipline.

Motivation Through Incremental Rewards

Maintaining motivation is critical for long-term adherence to a budget. Using Fibonacci-based milestones, small achievements can be rewarded proportionally, reinforcing positive behavior. Successfully managing discretionary spending or achieving incremental savings goals provides psychological satisfaction, strengthening long-term financial discipline and encouraging continued adherence to the system.

Important Information of This Blog

Fibonacci methods combine psychological insights with structured financial planning to foster financial discipline. Understanding behavioral triggers, allocating funds proportionally, and reinforcing habits through incremental rewards allows individuals to achieve sustainable financial control. Mindful tracking, prioritizing essential expenses, and managing discretionary spending support balance and long-term growth. This approach highlights that mastering finances requires both behavioral awareness and numeric planning.

At BusinessInfoPro, we empower entrepreneurs, small businesses, and professionals with actionable insights, strategies, and tools to fuel growth. By simplifying complex ideas in business, marketing, and operations, we help you turn challenges into opportunities and navigate today’s dynamic market with confidence. Your success is our mission because when you grow, we grow.

Kategoriler

Read More

The cleaning services sector is experiencing unprecedented growth globally, as rising awareness of hygiene, urbanization, and industrial expansion fuel demand. Organizations and households are increasingly outsourcing cleaning operations to professional providers to ensure efficiency and compliance with health standards. Residential, commercial, and industrial sectors are all driving growth in...

Introduction Italian furniture is becoming a popular choice for interior design projects across Canada, especially in Mississauga and Toronto, where modern living spaces are constantly evolving. Today, people are not just looking to fill their homes or offices with furniture, but they want to create spaces that feel comfortable, organized and easy to live in every day. Furniture plays an...

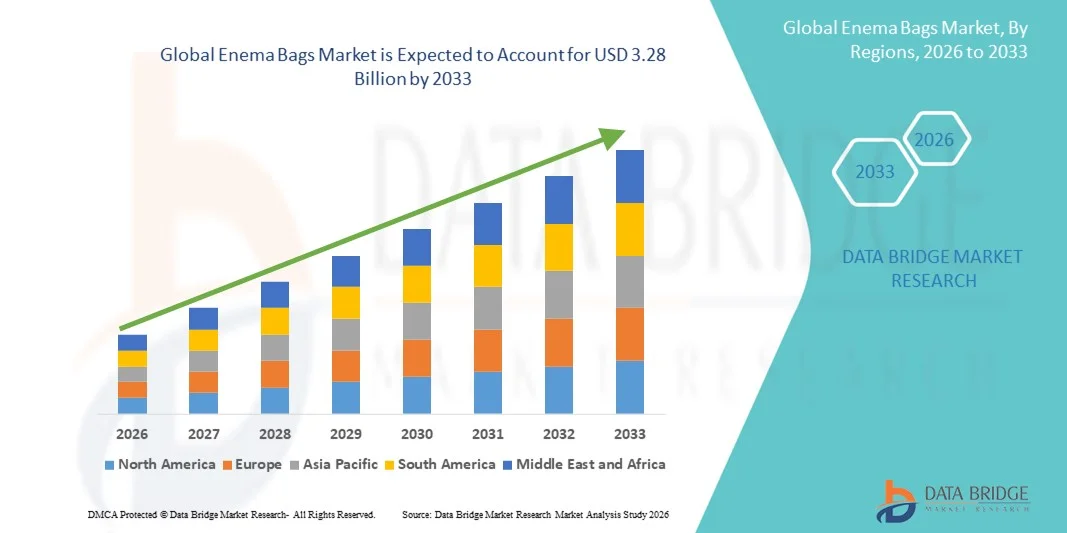

"Enema Bags Market Summary: According to the latest report published by Data Bridge Market Research, the Enema Bags Market The global enema bags market size was valued at USD 1.60 billion in 2025 and is expected to reach USD 3.28 billion by 2033, at a CAGR of 9.42% during the forecast period This Enema Bags Market research report also estimates potential...

Online sports betting has become extremely popular among Indian users who love cricket, football, tennis, and other fantastic games. But with so many platforms available, the biggest question is – how do we choose a safe and trusted betting platform like Reddy Anna? In this detailed guide, we will explain how to identify a secure online betting website and what features make platforms...

Rivelle Tampines is setting a new standard for modern living in Singapore’s vibrant eastern region. Combining elegant design, strategic location, and premium amenities, this development caters to individuals and families seeking comfort, convenience, and style. Prime Location in Tampines One of the most compelling features of Rivelle Tampines is its prime location. Situated in the heart...