Private Money Lenders: A Practical Guide to Fast Real Estate Financing

If a bank won’t lend or you need cash fast, private money lenders can fill the gap by offering loans outside traditional banking rules. You can tap private lenders for quicker approvals and more flexible qualifications, though expect higher rates and stricter terms tied to risk and collateral.

This article will help you understand how private lending works, what to watch for when comparing offers, and practical steps to evaluate credibility and protect your money so you can decide whether private funding fits your situation.

Understanding Private Money Lenders

Private money lenders provide non-bank financing for real estate and short-term needs, emphasizing speed, collateral, and flexible terms. Expect loans based on property value and exit strategy, diverse lender types, and different approval criteria compared with banks.

Definition and How Private Money Lending Works

Private money lending means an individual or private firm lends you funds outside traditional banks, often to buy, renovate, or refinance properties. Lenders focus primarily on the collateral’s current or after-repair value (ARV) and your exit plan — how you’ll repay the loan — rather than detailed income documentation or credit scores.

Typical loan features include shorter terms (often 6–24 months), higher interest rates than conventional mortgages, and larger fees or points at closing. You provide property details, a valuation or appraisal, and an exit strategy such as sale, refinance, or rental cash flow. The lender underwrites quickly, then secures the loan with a deed of trust or mortgage tied to the property.

Types of Private Money Lenders

You’ll encounter several common types:

- Hard money lenders: Professional companies or individuals making asset-based loans for fix-and-flip or bridge financing. They move fast and price loans to reflect higher risk.

- Family and friends: Informal loans with negotiated terms; these can be cheaper but carry relationship risks.

- Private lending groups or funds: Pooled capital from accredited investors or small funds offering standardized processes and defined lending criteria.

- Mortgage brokers and private mortgage companies: They connect you to private sources or originate private loans directly.

Each type differs in speed, documentation, fees, and willingness to finance unique projects. Choose based on your timeline, project risk, and how standardized you want the underwriting process to be.

Private Money Lenders vs Traditional Lenders

Private lenders base decisions on collateral and exit strategy; banks emphasize borrower creditworthiness, income verification, and long-term underwriting standards. You’ll get funds faster from private lenders, often within days to weeks, while bank approvals commonly take weeks to months.

Expect higher interest rates, points, and shorter loan terms from private lenders, but greater flexibility on property condition and borrower credit issues. Banks offer lower rates and longer amortizations but require stricter documentation, lower loan-to-value (LTV) ratios, and more regulatory compliance. Match your choice to your need for speed, tolerance for cost, and ability to meet strict underwriting requirements.

How to Find and Evaluate Private Money Lenders

You’ll need reliable sources to build a pipeline, clear criteria to vet credibility, careful review of loan terms, and a realistic view of risks versus benefits. Focus on documented experience, transparent costs, and written agreements.

Sourcing Reliable Private Money Lenders

Search multiple channels to avoid single-source dependency. Start with local real estate investor meetups, landlord associations, and real estate agents who regularly close investment deals. Ask attorneys, title companies, and accountants for referrals — they often work with repeat private lenders.

Use online platforms and investor marketplaces, but verify identities and track records before trusting listings. Contact past borrowers for references and ask for deal summaries that show loan sizes, LTVs, and outcomes. Maintain a short list of 3–5 lenders you’ve vetted so you can compare offers quickly.

Criteria for Assessing Lender Credibility

Check licensing and business registration where applicable; some states require consumer lending licenses or business filings. Verify at least three completed loans similar to your project type and size. Ask for references with contactable borrowers and specific questions about timelines and communication.

Review lender policies on due diligence: appraisal requirements, borrower experience thresholds, and default handling. Look for transparency — a credible lender provides clear fee schedules, sample loan documents, and a written timeline from application to funding. Red flags include evasive answers, pressure to sign immediately, or unverifiable references.

Loan Terms and Conditions

Compare these core elements: interest rate, origination fees, points, loan-to-value (LTV), amortization or interest-only structure, and prepayment penalties. Note whether interest accrues monthly or daily and how late payments are charged. Confirm whether the loan is recourse or non-recourse; recourse loans allow the lender to pursue your personal assets.

Require a written term sheet before due diligence. Look for specific covenants, exit strategy expectations (sale, refinance, or refinance timeline), and clear closing cost allocation. Create a simple comparison table for each lender showing rate, fees, LTV, term length, and typical funding turnaround to make an apples-to-apples choice.

Risks and Benefits of Working With Private Money Lenders

Benefits: fast funding, flexible underwriting, and willingness to finance unconventional deals or borrowers with limited bank credit. Private lenders often base decisions on asset value and exit plan, which can speed approvals for fix-and-flip or bridge financing.

Risks: higher interest and fees, shorter loan terms, and stricter default remedies. You may face faster foreclosure timelines and tighter covenants. Mitigate risk by negotiating caps on fees, securing an explicit cure period for defaults, and documenting an exit plan that lenders accept. Keep contingency reserves for cost overruns and vacancy to protect your returns.

Категории

Больше

The kitchen is one of the most used areas in any home, making regular cleaning essential for health and safety. From food preparation to daily cooking, keeping your kitchen clean helps prevent germs, pests, and unpleasant odours. These simple kitchen cleaning tips will help you maintain a spotless and hygienic kitchen. 1. Clean as You Cook One of the best habits is to clean while...

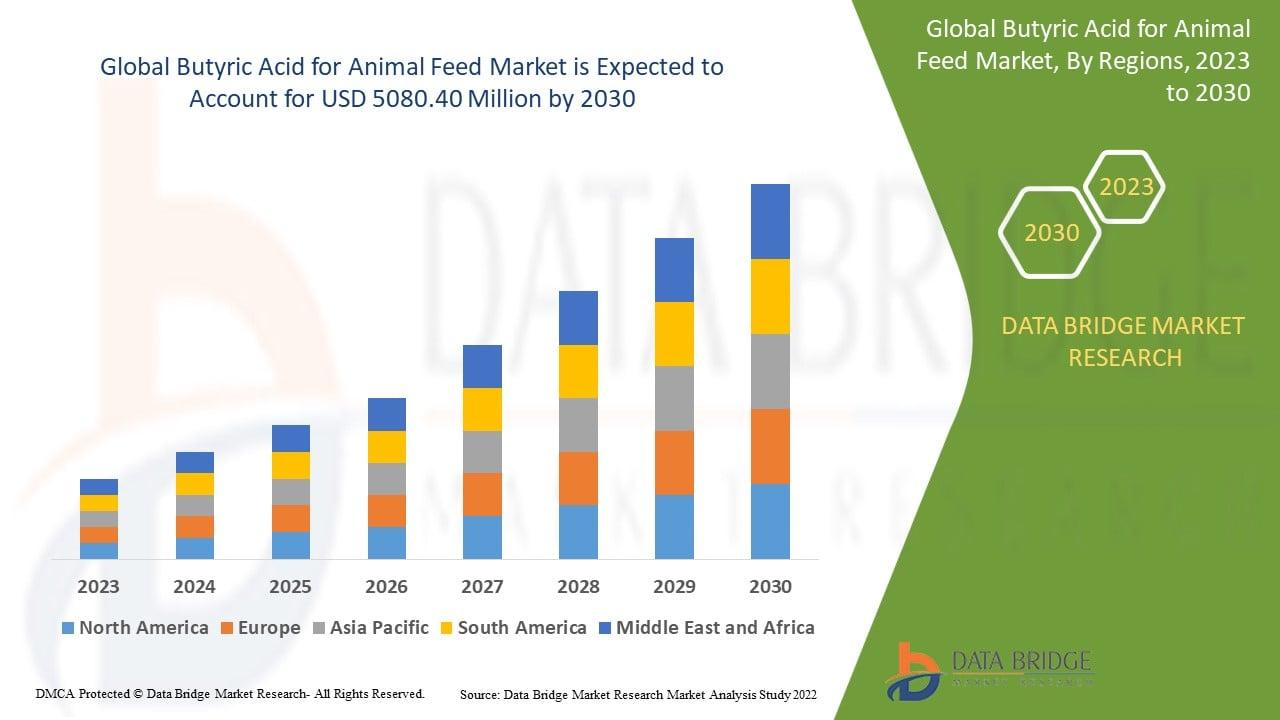

According to the latest report published by Data Bridge Market Research, the Butyric Acid for Animal Feed Market Data Bridge Market Research analyses that the butyric acid for animal feed market was valued at USD 2335.85 million in 2022 and is expected to reach USD 5080.40 million by 2030, registering a CAGR of 10.20% during the forecast period of 2023 to 2030. The Butyric Acid for...

We present a comprehensive, professionally written, and SEO-optimized guide to the Qatar Airways Philadelphia Office, designed to assist travelers seeking accurate, reliable, and efficient airline services in one of the United States’ most historically significant and strategically located cities. Philadelphia serves as an important travel gateway for business, education, and...

In recent years, the global Smart Ticketing Market has undergone a transformative journey, fueled by evolving consumer demands, cutting-edge innovations, and an increasing focus on sustainability. Our comprehensive Smart Ticketing Market Research Report unveils key strategic insights, highlighting growth trends, market dynamics, competitive landscapes, and emerging...

Cricket is not just a sport in India. It is a season, a mood, a daily conversation, and sometimes the main reason people keep checking their phones every few minutes. From IPL nights to World Cup fever, every cricket phase brings its own excitement. That is where Skyexch Plus becomes a useful online space for cricket fans who want quick access, smooth navigation, and a better match-season...