Aircraft Engine Fuel Systems Market Forecast Amid Aviation Expansion

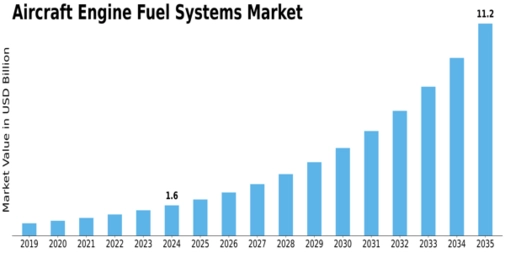

The global forecast for the Aircraft Engine Fuel Systems Market indicates expansion from USD 63.8 billion in 2024 to USS 116.2 billion by 2035 at a CAGR of 5.6%. But beyond the global figure, regional dynamics and growth opportunities warrant closer attention.

Key Regional Markets

- North America and Europe: These mature markets drive demand for retrofits, upgrades and high-end fuel system components. Given established fleets and strict regulatory regimes, OEMs and component suppliers invest heavily in advanced systems here.

- Asia-Pacific: Perhaps the most striking growth opportunity lies in this region. Rapid growth of commercial aviation fleets, increasing military spending and embracing of UAV platforms fuel demand for aircraft engine fuel systems.

- Middle East & Africa, Latin America: These regions represent rising but less-penetrated markets. Growth is driven by infrastructure development, emerging airlines and defence modernisation.

Growth Opportunities

The segmentation data indicates that not only installation of new fuel systems but retro-fitting existing aircraft are major opportunities. In Asia-Pacific and Latin America, newer airlines are buying aircraft with modern fuel systems, while legacy fleets in North America and Europe are being upgraded. Given the overall market trajectory, regional players and global suppliers alike need to tailor regional market strategies—such as local partnerships, supply-chain localisation and after-market services.

Strategic Takeaway

For global players in the aircraft engine fuel systems market, regional growth requires nuanced strategies. In mature regions, differentiation via premium technology and service is essential; in emerging regions, volume growth, cost-effective solutions and localisation matter more. Ultimately, the global number (USS 116.2 billion by 2035) is only meaningful if the regional engines of growth are fully leveraged.

GLOBAL SUPPLY CHAIN & MARKET DISRUPTION ALERT

Escalating geopolitical tensions in the Middle East, particularly around the Strait of Hormuz and the Red Sea, are creating significant disruptions across global energy, chemicals, and logistics markets. Critical shipping corridors are under pressure, with major oil, LNG, petrochemical, and raw material flows at risk, triggering supply chain delays, freight cost surges, insurance withdrawals, and heightened price volatility. These disruptions are increasing operational risks and cost uncertainties for industries dependent on global trade routes and energy-linked feedstocks.

Категории

Больше

The bath and body market continues to expand as consumers prioritize relaxation, wellness, and consistent self-care routines. What was once considered a simple household purchase has evolved into a lifestyle-driven category supported by repeat buyers and strong brand loyalty. For retailers and product developers, this shift presents measurable growth opportunities when supported by smart...

According to the latest report published by Data Bridge Market Research, the Myeloproliferative Disorders Drugs Market The global myeloproliferative disorders drugs market size was valued at USD 9.75 billion in 2025and is expected to reach USD 12.83 billion by 2033, at a CAGR of 3.50% during the forecast period This global Myeloproliferative Disorders Drugs Market report is a...

The e-commerce packaging market has become a vital component of the global online retail ecosystem. As digital commerce continues to expand rapidly, the need for efficient, protective, and sustainable packaging solutions has intensified. Packaging not only ensures product safety during transit but also enhances brand identity and customer experience. This report highlights...

Earning a CompTIA certification like A+, Network+, or Security+ is a big step for any IT career. These exams test real skills and require weeks of focused study. But life does not always follow a study plan. You might have a family emergency, a sudden work crisis, or a technical issue at home. When the exam date arrives and you are not ready or cannot be there, the stress is huge. This is when...

Page one of Google. That's where every website owner wants to be. And honestly, it's not as impossible as it sounds. But it does require understanding what Google actually rewards and then doing that work consistently. There are no shortcuts worth taking. But there is a clear path. And this article walks you through it. What Google Is Actually Looking For Before diving into tactics, it...