Understanding Mortgage Loan Services and How They Shape Your Financial Future

Exploring the Different Types of Mortgage Loans Available to Homebuyers

Mortgage loans are essential financial tools that enable individuals and families to purchase homes without needing to pay the full price upfront. These loans come in various forms, each designed to cater to specific financial situations and long-term goals. Fixed-rate mortgages provide stability by maintaining the same interest rate throughout the life of the loan, making budgeting predictable and stress-free. Adjustable-rate mortgages, on the other hand, offer lower initial rates that may change over time based on market conditions, appealing to borrowers who anticipate income growth or short-term ownership. Government-backed loans, such as FHA, VA, and USDA programs, make homeownership more accessible for first-time buyers, veterans, and rural residents by offering lower down payments and more flexible credit requirements.

The Application Process for Mortgage Loans and What Lenders Look For

Securing a mortgage loan involves a detailed application process designed to assess the borrower’s financial stability and repayment ability. Lenders typically review credit scores, employment history, income, existing debts, and overall financial behavior. A higher credit score can often result in lower interest rates and better loan terms, while consistent employment history reassures lenders about the borrower’s financial reliability. The debt-to-income ratio, which compares monthly debt payments to monthly income, plays a crucial role in determining loan eligibility VA loans Greensboro and affordability. Understanding these requirements before applying can help borrowers choose the best loan type, prepare necessary documentation, and increase the likelihood of approval.

Interest Rates and How They Influence the Total Cost of a Mortgage

Interest rates are a critical factor in determining the overall cost of a mortgage loan. Even a small difference in rates can significantly impact monthly payments and the total amount paid over the life of the loan. Fixed-rate loans lock in a consistent rate, shielding borrowers from market fluctuations, whereas adjustable-rate loans can fluctuate based on economic conditions, sometimes resulting in lower initial payments but potential increases over time. Understanding the relationship between interest rates, loan terms, and repayment schedules empowers borrowers to make informed decisions and select the mortgage plan that aligns with their financial goals.

Down Payments and Their Effect on Loan Terms and Monthly Payments

The size of a down payment can influence both loan approval and future financial obligations. Larger down payments generally reduce the loan amount required, potentially securing lower interest rates and decreasing monthly payments. Some lenders offer special programs that allow smaller down payments for first-time buyers or those with limited savings, though these may require additional insurance or fees. Planning a down payment carefully can help manage long-term costs, reduce financial stress, and facilitate smoother mortgage processing.

Additional Costs Associated with Mortgage Loans Beyond Principal and Interest

While monthly principal and interest payments make up the core of a mortgage, borrowers should also account for other expenses that affect affordability. Property taxes, homeowners insurance, private mortgage insurance (PMI), and maintenance costs are common additional financial responsibilities. Budgeting for these expenses ensures that homeowners can manage their mortgage sustainably without unexpected financial strain. Being aware of the full cost structure of a mortgage loan is essential for long-term financial planning and maintaining homeownership stability.

Refinancing Mortgage Loans as a Strategy to Reduce Costs and Improve Financial Flexibility

Refinancing allows homeowners to replace an existing mortgage with a new loan that may have better terms, lower interest rates, or different repayment structures. This strategy can be particularly useful when interest rates drop or when borrowers want to consolidate debts and improve cash flow. However, refinancing also involves fees and closing costs, so evaluating the potential savings against these expenses is critical. Understanding when and how to refinance can help homeowners optimize their mortgage and free up financial resources for other priorities.

Working with Mortgage Brokers Versus Direct Lenders and Choosing the Best Option

Borrowers can choose between working directly with banks and lending institutions or using mortgage brokers to access a wider range of loan options. Direct lenders often offer streamlined processes and specific loan products, while brokers provide expertise in comparing multiple lenders to find the best rates and terms. Selecting the right approach depends on individual preferences, financial complexity, and comfort level with the application process. Evaluating the pros and cons of each path ensures borrowers make an informed choice that meets their needs.

Understanding Mortgage Loan Servicing and Its Role in Homeownership

Mortgage loan servicing refers to the management of the loan after it has been disbursed, including collecting payments, managing escrow accounts, and handling customer service. Servicers ensure that taxes and insurance premiums are paid on time and that any issues with the loan are addressed promptly. Knowing who services your mortgage and the level of support provided can reduce confusion and help homeowners stay on top of their obligations, avoiding late fees or penalties.

Tips for Improving Loan Approval Chances and Securing Favorable Terms

Successful mortgage applications often involve preparation, research, and financial discipline. Key strategies include maintaining a strong credit score, reducing outstanding debt, saving for a larger down payment, and documenting income and employment history clearly. Engaging with financial advisors or mortgage specialists can also help identify suitable loan products and negotiate favorable terms. By taking these steps, borrowers increase their chances of approval and can secure a mortgage that aligns with both short-term needs and long-term financial objectives.

The Future of Mortgage Loans and Emerging Trends in Home Financing

The mortgage industry continues to evolve with technological advancements, shifting economic conditions, and changing borrower expectations. Digital mortgage platforms are streamlining application processes, AI-driven tools provide personalized loan recommendations, and sustainability-focused loans are emerging for energy-efficient homes. Staying informed about these trends allows borrowers to take advantage of innovative products, maximize savings, and make strategic decisions about homeownership in an ever-changing market.

Категории

Больше

A tabless lyra is a powerful choice for aerial artists who want freedom of movement, clean lines, and versatile performance options. Designed without attachment tabs, this apparatus allows performers to rig from any point, making it ideal for dynamic routines, creative transitions, and visually striking acts. If you are looking to buy tabless lyra equipment that balances artistry with...

Train Battery Market Size, Share, and Growth The global Train Battery Market has demonstrated consistent growth over recent years. According to industry estimates, the market is projected to reach approximately USD 769.24 million by 2030, growing at a CAGR of around 5.1% during the forecast period. Another analysis suggests that the market could grow from USD 275...

Python key phrases are special reserved phrases in the Python programming language that carry predefined meanings and play a vital function in defining the shape and logic of a software. They are an crucial a part of Python’s syntax, and programmers cannot use them as variable names, feature names, or identifiers due to the fact Python uses these words to understand how the code should be...

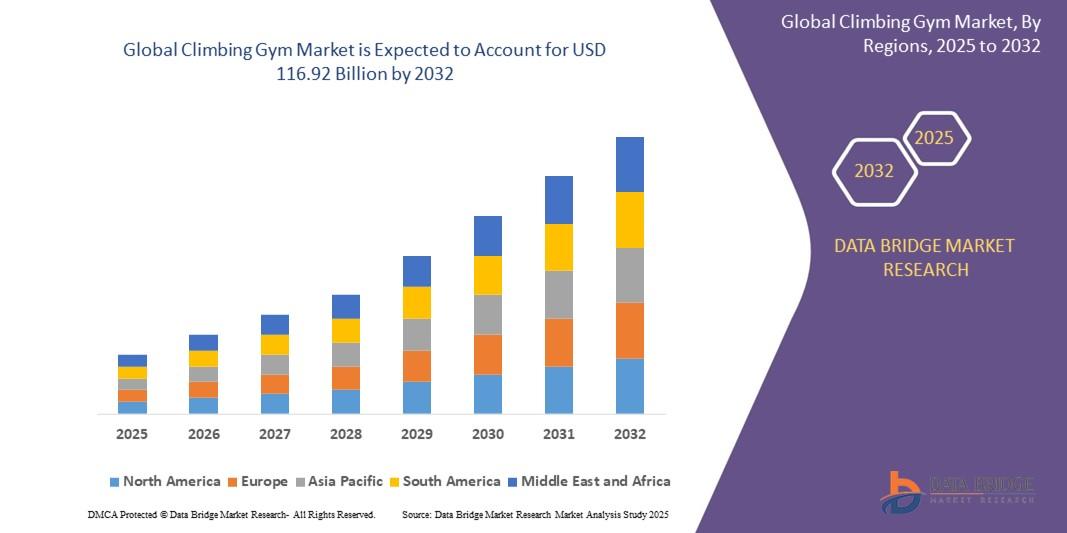

クライミングジム市場の 規模とシェアに影響を与える主な要因 CAGR値 世界のクライミングジム市場は 2024年に711億8000万米ドルと評価され 、 2032年までに1169億2000万米ドル に達すると予想されています。2025年から2032年の予測期間中、市場は主に屋内フィットネス活動の人気の高まりとアドベンチャースポーツへの関心の高まりによって6.40%のCAGR で成長する と予想されます。 この成長は、身体的な健康に関する意識の高まり、都市化、可処分所得の増加、そしてユニークで挑戦的なトレーニング体験への欲求などの要因によって推進されています。...

"Executive Summary Asia-Pacific Golf Apparel, Footwear, and Accessories Market Research: Share and Size Intelligence Data Bridge Market Research analyses that the Asia-Pacific golf apparel, footwear, and accessories market is expected to reach a value of USD 2,825.80 million by 2029, at a CAGR of 3.9% during the forecast period. This Asia-Pacific Golf Apparel, Footwear, and...