Liquidity vs Profitability: Striking the Right Balance Using Key Financial Ratios

Two Vital but Competing Priorities

Every business must navigate a fundamental tension between two financial imperatives that, while both essential, frequently pull against each other. Profitability — the generation of surplus revenue over costs — is the ultimate measure of a business's commercial viability and the source of the returns that justify its existence. Liquidity — the availability of sufficient cash and near-cash assets to meet obligations as they fall due — is the operational prerequisite without which a business cannot function, regardless of how profitable it may be on paper.

Strategies that maximise profitability often reduce liquidity: investing cash in productive assets, extending customer credit to drive sales, carrying larger inventory to prevent stockouts. Strategies that protect liquidity often constrain profitability: holding larger cash reserves, shortening receivables cycles, maintaining conservative credit terms. Understanding this tension — and using Financial Ratios to navigate it intelligently — is one of the most practically important analytical skills in financial management.

Why Profitable Companies Still Fail

The counterintuitive reality that profitable companies can and do fail is one of the most important lessons in business finance. A company can report strong net profit margins while simultaneously accumulating overdue payables, drawing down its cash reserves, and approaching a liquidity crisis — because profitability is an accounting measure and liquidity is a cash flow reality, and the two do not always move in tandem.

This divergence is particularly acute in fast-growing businesses. Rapid growth consumes cash — for inventory, for receivables financing, for capital investment — often far faster than the profit generated by that growth can replenish it. The phenomenon of overtrading: growing faster than the business's cash position can support, has destroyed many otherwise sound businesses. Financial Ratios provide the framework for detecting and managing this risk before it becomes a crisis.

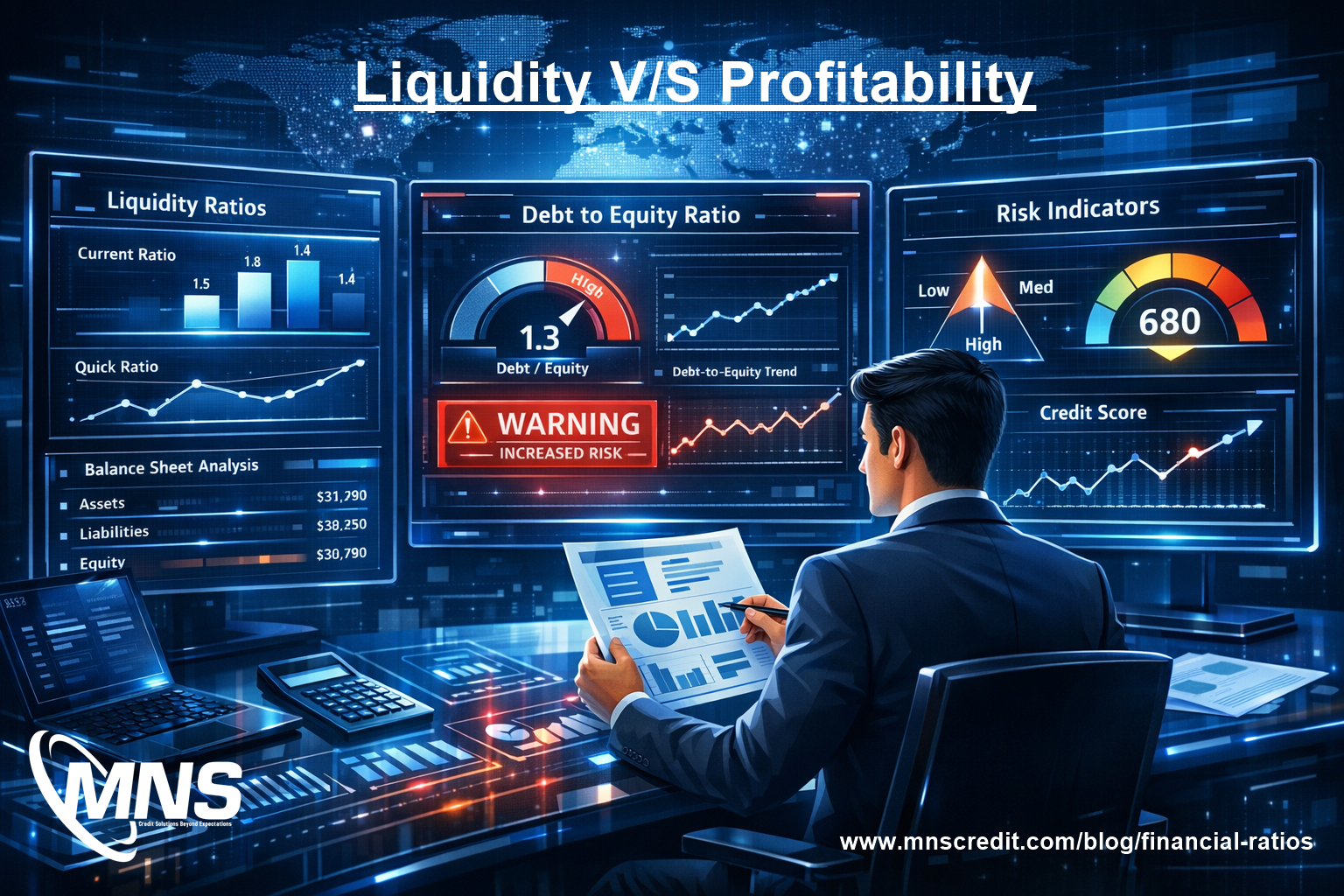

Key Liquidity Ratios and What They Reveal

The Current Ratio, which divides current assets by current liabilities, is the foundational liquidity measure. A ratio above 1.5 is generally considered adequate for most businesses; significantly below 1.0 indicates current liabilities exceed current assets, which is a serious concern. The Quick Ratio refines this by excluding inventory, providing a more conservative view of immediately realisable liquidity.

The Cash Conversion Cycle (CCC) — which combines Days Sales Outstanding, Days Inventory Outstanding, and Days Payable Outstanding — offers a dynamic view of how quickly a business converts its operations into cash. A lengthening CCC indicates that cash is taking longer to cycle through the business, which pressures liquidity even when trading conditions appear healthy. Managing the CCC aggressively is one of the most effective levers for improving liquidity without reducing profitability.

Key Profitability Ratios and Their Relationship to Liquidity

Gross Profit Margin measures the efficiency of core operations — how much revenue remains after direct costs. Net Profit Margin captures the full picture after overhead and financing costs. Return on Equity (ROE) and Return on Assets (ROA) assess how effectively capital is being deployed to generate returns.

These profitability measures have a direct bearing on the liquidity picture, but with a timing lag. Strong profitability that is not converting into cash flow — because of high receivables, slow inventory turnover, or aggressive reinvestment — creates precisely the profitable-but-illiquid condition that poses the greatest hidden risk. Monitoring both sets of Financial Ratios simultaneously, and watching for divergence between them, is the core of balanced financial management.

The Warning Signs of Imbalance

Several ratio patterns signal an imbalance between liquidity and profitability that warrants attention. A rising Net Profit Margin accompanied by a declining Current Ratio suggests that profitability is being generated at the cost of liquidity — perhaps through aggressive credit extension or inventory buildup. A rising Current Ratio accompanied by falling profitability suggests the opposite: excessive caution is protecting liquidity at the expense of commercial performance.

The Receivables Turnover Ratio and Inventory Turnover Ratio are particularly useful for diagnosing the source of liquidity pressure. Slowing receivables turnover — customers taking longer to pay — directly reduces cash availability even when invoiced revenue appears healthy. Slowing inventory turnover ties up cash in stock that is not converting to sales, compressing liquidity without reducing reported profit.

Using a Business Information Report for External Benchmarking

For businesses evaluating their own balance, or assessing the financial health of a counterparty, a Business Information Report that presents key Financial Ratios alongside industry benchmarks provides invaluable context. A Current Ratio of 1.3 may be perfectly adequate in one industry and dangerously low in another; a Net Profit Margin of 5% may be strong for a distribution business and weak for a software company. Without industry context, ratio interpretation is incomplete.

Benchmarking against industry peers reveals whether the liquidity-profitability balance being struck is appropriate for the competitive and operational environment, or whether structural adjustments are needed to bring the business into alignment with sustainable norms for its sector.

Strategies for Achieving the Right Balance

Practical strategies for improving the liquidity-profitability balance include tightening receivables management to shorten the cash conversion cycle, optimising inventory levels through demand forecasting and supplier negotiation, reviewing payment terms to ensure they reflect actual risk rather than sales-driven generosity, and ensuring that profit is being converted into genuine cash flow rather than remaining locked in working capital.

Conclusion

Liquidity and profitability are not competing goals — they are complementary dimensions of financial health that must be actively managed in balance. Financial Ratios provide the precise, comparable, trend-sensitive measures needed to monitor both simultaneously and detect imbalance before it becomes a crisis. Businesses that master this balance — and that regularly review their ratio profiles against historical trends and industry benchmarks — build financial resilience that sustains performance through both growth phases and downturns.

Κατηγορίες

Διαβάζω περισσότερα

Polaris Market Research has introduced the latest market research report titled Medical Tourism Market Share, Size, Trends & Industry Analysis Report By Treatment Type (Cosmetic Treatment, Bariatric Treatment, Dental Treatment, Cardiovascular Treatment); By Service Provider; By Region; Segment Forecast, 2025 - 2034 that highlights the major revenue stream for the forecast period....

The world of cricket betting has rapidly progressed, and T20 Exchange is at the forefront of this revolution. If you like to analyze matches, to predict momentum shifts and trade odds on the fly, it’s as if this platform was built for you. Having been around the cricket betting markets for many years, I can say that T20 Exchange provides a more refined, flexible experience...

India’s textile heritage is a tapestry of artistry, culture, and centuries-old craftsmanship. Among the most celebrated weaves are Banarasi sarees and the lesser-known yet equally exquisite Mashru silk. These fabrics are not just garments—they are expressions of tradition, luxury, and identity. In this blog, we explore the beauty, uniqueness, and appeal of various silk sarees that...

The Internet of Robotics Things Market Forecast to 2031 delivers an in-depth analysis designed for key stakeholders including investors, manufacturers, suppliers, and strategic decision-makers. the study examines current market conditions, emerging technologies, economic factors, and long-term growth opportunities shaping the global Fermented Plant Milk industry. Request a Sample...

Premium facial surgery has become an essential part of modern aesthetic medicine, offering refined solutions for individuals seeking balanced facial harmony and improved self-confidence.Advanced surgical techniques now focus on precision, safety, and natural-looking outcomes that enhance individual features without overcorrection.Patients today prefer procedures that deliver long-lasting...