Global Waste Management Market to Reach USD 2.8 Trillion by 2036

The global waste management market is entering a transformative decade, evolving from traditional disposal systems into integrated, technology-driven resource recovery platforms. According to the latest analysis by Future Market Insights, the market—valued at USD 1.5 trillion in 2025—is projected to grow to USD 1.6 trillion in 2026 and USD 2.8 trillion by 2036, expanding at a steady CAGR of 5.4%.

This USD 1.3 trillion absolute dollar opportunity signals a structural shift rather than incremental growth, as governments, municipalities, and corporations accelerate investments in sustainability infrastructure and circular economy models.

Market Momentum Driven by Urbanization and Regulatory Pressure

Rapid urbanization and population growth continue to intensify global waste volumes, placing pressure on municipalities to modernize infrastructure. At the same time, increasingly stringent environmental regulations are forcing a transition away from landfill dependency toward recycling and resource recovery.

Key growth drivers include:

-

Urban expansion increasing municipal solid waste generation

-

Circular economy regulations promoting recycling and reuse mandates

-

Digital technologies enabling route optimization and cost efficiency

-

Extended Producer Responsibility (EPR) policies reshaping waste accountability

-

Infrastructure investments in waste-to-energy and advanced processing facilities

Executives are increasingly recognizing waste management not as a cost center, but as a strategic value chain opportunity tied to sustainability and resource optimization.

Emerging Trends Redefining Industry Economics

The industry is undergoing rapid transformation, fueled by technology adoption and evolving business models. Automated systems and data-driven operations are significantly improving efficiency while enhancing profitability.

Notable trends shaping the market include:

-

Smart waste collection systems leveraging IoT and real-time tracking

-

Automated sorting technologies improving recycling yield and economics

-

Shift toward resource recovery over traditional disposal models

-

Integration of renewable energy generation through waste-to-energy plants

-

Private sector participation in municipal waste contracts

These advancements are enabling companies to scale operations while maintaining cost discipline—critical in a price-sensitive, regulation-heavy market.

Regional Insights: Asia-Pacific Emerges as Growth Engine

While mature markets in North America and Europe continue to lead in regulatory sophistication and technological adoption, Asia-Pacific is emerging as the fastest-growing region, driven by infrastructure expansion and rising waste volumes.

-

United States (6.2% CAGR) leads with strong regulatory frameworks and organics recycling initiatives

-

Germany (5.8% CAGR) benefits from advanced circular economy policies

-

Japan (5.5% CAGR) accelerates through automated recycling technologies

-

China (5.1% CAGR) drives large-scale waste-to-energy investments

-

India (4.8% CAGR) sees growth through urbanization and public-private partnerships

Asia-Pacific’s cost-efficient infrastructure development and government-backed initiatives position it as a global hub for waste management expansion.

Competitive Landscape: Scale, Integration, and Compliance Define Leaders

The market remains moderately consolidated, with leading players leveraging integrated service models and operational scale to secure long-term municipal contracts.

Key companies operating in the market include:

Waste Management Inc., Republic Services Inc., Veolia Environment S.A., SUEZ Environment, Clean Harbors Inc., Stericycle Inc., Covanta Holding Corporation, China Everbright International, Remondis SE & Co. KG, Biffa Group

Strategic developments highlight increasing consolidation and capability expansion:

-

Veolia’s acquisition of Clean Earth strengthens its hazardous waste portfolio

-

Biffa’s recycling partnerships enhance plastic circularity infrastructure

-

Cross-border collaborations accelerate environmental service innovation

Companies with end-to-end capabilities across collection, processing, and recycling are gaining a competitive edge, particularly in securing high-value municipal contracts.

Analyst Perspective: Technology as a Competitive Advantage

According to FMI analysts, the next phase of industry evolution will be defined by how effectively companies integrate technology into their operational frameworks.

Digitalization is no longer optional—it is becoming a core differentiator. Automated sorting, AI-driven logistics, and real-time monitoring systems are directly impacting cost structures and service quality.

Additionally, regulatory frameworks are shifting industry focus toward resource recovery and sustainability compliance, reducing reliance on landfill-based models and unlocking new revenue streams.

Future Outlook: From Waste Disposal to Resource Intelligence

Looking ahead, the waste management industry is poised to become a critical pillar of the global sustainability economy. As circular economy principles gain traction, companies that align operations with environmental goals will capture disproportionate value.

Key opportunities include:

-

Expansion of recycling and material recovery infrastructure

-

Growth in waste-to-energy solutions

-

Increasing demand for integrated service platforms

-

Adoption of data-driven waste management ecosystems

For investors and decision-makers, the sector offers a compelling mix of stable cash flows, regulatory tailwinds, and long-term growth visibility - https://www.futuremarketinsights.com/reports/waste-management-market

الأقسام

إقرأ المزيد

In the ever-expanding world of online gaming and betting platforms, Koitoto has started to gain attention among users looking for diverse entertainment options. As digital platforms continue to evolve, services like Koitoto are positioning themselves as accessible hubs for gaming enthusiasts who want convenience, variety, and engaging experiences in one place. What is Koitoto? Koitoto is...

In a world where people move constantly between screens, streets, and reading materials, Lens Vision Optical as become an important idea for modern eye care, and Lens Vision Optical solutions are now expected to deliver both clarity and comfort in one balanced experience. As daily routines become more visually demanding, users need products that support sharp vision, reduce strain, and...

"Europe Contrast Injector Market Summary: According to the latest report published by Data Bridge Market Research, the Europe Contrast Injector Market The Europe contrast injector market size was valued at USD 397.42 million in 2025 and is expected to reach USD 582.71 million by 2033, at a CAGR of 4.90% during the forecast period. Global market research...

The global food market is witnessing a strong shift toward healthier and natural ingredients, and seed-based products are gaining remarkable popularity. Consumers today are more aware of nutrition, leading to an increased demand for seeds that offer both taste and health benefits. From traditional cuisines to modern recipes, seeds are widely used for their versatility. They are rich in...

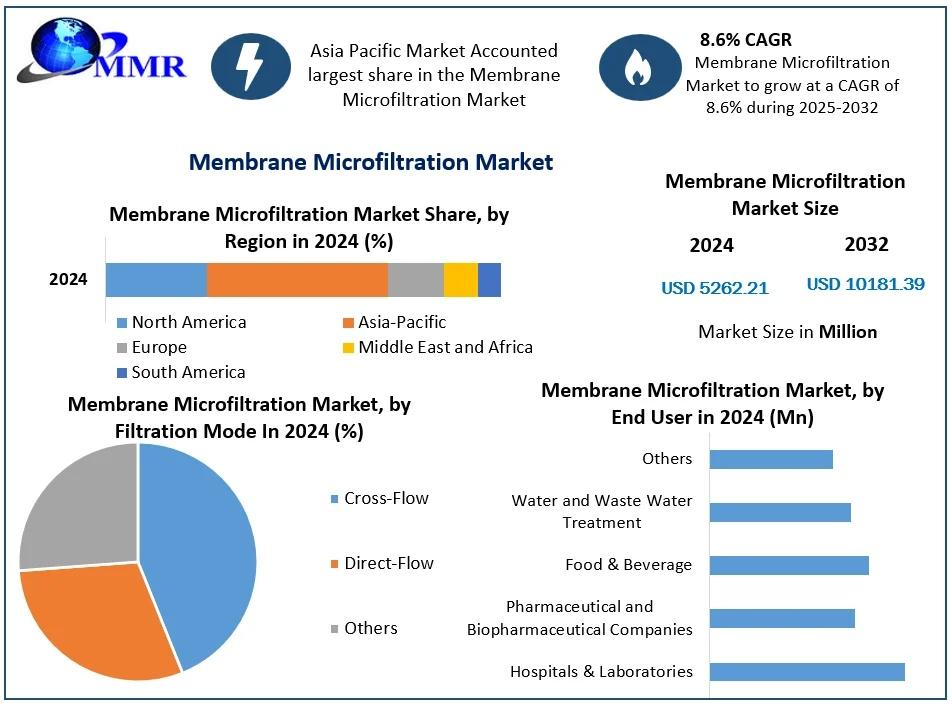

Anticipated Growth in Revenue: The Membrane Microfiltration Market was valued US$ 5262.21 Mn. in 2024 and is expected to reach US$ 10181.39 Mn. by 2032, at a 8.60% CAGR of around during a forecast period. Market Overview The global Membrane Microfiltration Market has emerged as a critical component in modern industrial filtration systems. Membrane microfiltration is a...