10 Ways To Secure A No Down Payment Mortgage For First-Time Buyers

The dream of owning a home is a powerful motivator, but for many young professionals and growing families, the initial cash requirement feels like an insurmountable wall. You might find yourself staring at real estate listings and wondering exactly how much down payment for a house is needed to get started. While the old-school advice suggested saving twenty percent, the modern lending offers a no down payment mortgage to those who know where to look. Transitioning from a tenant to an owner does not always require a massive bank balance if you leverage the right financial tools and programs available in today's diverse marketplace.

1. Utilizing the Power of VA Financing

For those who have served in the military, the VA loan is arguably the most powerful tool in real estate. It offers a true zero-percent initial investment option with no monthly mortgage insurance. This program is backed by the government to ensure that veterans can transition into civilian life with stable housing. The eligibility extends to active-duty members, veterans, and even surviving spouses in some cases. It is a benefit earned through service that removes the biggest barrier to entry in the housing market.

2. Exploring Rural Development Opportunities

If you aren't a veteran but are willing to live in a less densely populated area, the USDA loan is a fantastic alternative. Many people are surprised to find that eligible areas include not just farmland, but many quiet suburban pockets on the outskirts of major cities. These loans provide 100% financing to low-to-moderate-income borrowers. The goal is to encourage growth in rural communities, making it an ideal path for first-time buyers looking for space and affordability without a large upfront cost.

3. Applying for State-Sponsored Grants

Every state has a Housing Finance Agency dedicated to making homeownership reachable. These agencies often provide down payment assistance grants that can cover the entire 3% or 3.5% required by standard loan types. When you look at the minimum down payment for house requirements, these grants essentially act as a bridge. Some of these funds are structured as a gift that never needs to be repaid, provided you remain in the home for a set period, effectively resulting in a zero-down experience.

4. Seeking Community Seconds and Silent Mortgages

In addition to flat grants, many local municipalities offer what is known as a silent second mortgage. This is a secondary loan that covers your initial investment and closing costs. It is called silent because it usually carries 0% interest and requires no monthly payments. The balance is typically only due if you sell the home or refinance. This allows you to purchase a home using a conventional or FHA structure while bringing none of your own cash to the closing table.

5. Negotiating Significant Seller Concessions

In a market where sellers are motivated, you can ask the current owner to pay for your closing costs. While the seller cannot pay your actual down payment, they can cover the thousands of dollars in taxes, title fees, and lender charges. By pairing this with a low-down-payment loan and a small gift or grant, the total cash you need to bring to the appointment can be virtually non-existent. It is all about how the contract is written and negotiated by your real estate professional.

6. Tapping into Employer-Assisted Housing Programs

Some large corporations, universities, and hospital systems offer housing benefits to attract and retain talent. These Employer-Assisted Housing programs might provide a forgivable loan or a direct grant to employees purchasing a home near their workplace. If you work for a major institution, check with your human resources department. Often, these benefits can be combined with other low-investment loan products to create a path to ownership that requires no personal savings for the initial purchase.

7. Leveraging Gift Funds from Family

Almost all loan programs allow for a family member to provide the funds for your purchase. This is a common way for parents or grandparents to help the next generation build equity. The lender will require a gift letter stating that the funds do not need to be repaid. When this is used in conjunction with an FHA loan or a 3% conventional loan, the buyer can walk into a new home without touching their own savings account, preserving their liquid cash for future needs.

8. Utilizing Professional Grade Specialized Loans

Certain professions, such as doctors, dentists, and sometimes attorneys, have access to specialized portfolios often called Physician Loans. These products recognize that while these professionals may have high student debt and low initial savings, they have high earning potential. Many of these programs offer 100% financing with no private mortgage insurance. It is a customized approach to lending that looks at the trajectory of a career rather than just the current balance in a checking account.

9. Navigating the Direct Approval Process

Regardless of which zero-down path you take, your file will eventually reach a mortgage underwriter who will verify the validity of your financial documents. This professional ensures that the zero-down program guidelines are strictly followed and that your income supports the monthly debt. They are the final set of eyes on the transaction. Having an organized paper trail for your income and any assistance funds you are receiving will make this process much smoother and ensure that your no-money-down deal actually makes it to the finish line.

10. Investigating Nonprofit Housing Organizations

Organizations like NACA (Neighborhood Assistance Corporation of America) provide a unique pathway to homeownership with no down payment, no closing costs, and no perfect credit requirement. These programs are more labor-intensive and require participation in workshops and counseling, but they offer some of the most favorable terms in the industry. For a dedicated first-time buyer, the time investment is a small price to pay for a mortgage that requires zero dollars upfront and offers a below-market interest rate.

Categorias

Leia mais

In today's fast-paced digital world, a reliable and organized network is essential for businesses across Ireland. Patch panels play a key role, connecting and managing multiple network cables to ensure smooth performance and minimal downtime. At PC Systems, we offer high-quality patch panels in Ireland that simplify cable management, make maintenance easier, and keep your IT infrastructure...

Introduction Men’s sexual wellness is an essential part of overall health, influencing confidence, relationships, and quality of life. In today’s fast-paced environment, stress and lifestyle factors can impact performance, leading many individuals to seek convenient and discreet solutions. Zypharix Labs has become a recognized digital platform that provides access to popular...

"In-Depth Study on Executive Summary Hydrogenated Oils Market Size and Share The global hydrogenated oils market was valued at USD 85.20 billion in 2024 and is expected to reach USD 119.32 billion by 2032. During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 4.30%, primarily driven by the increasing demand for processed foods and the growing use of...

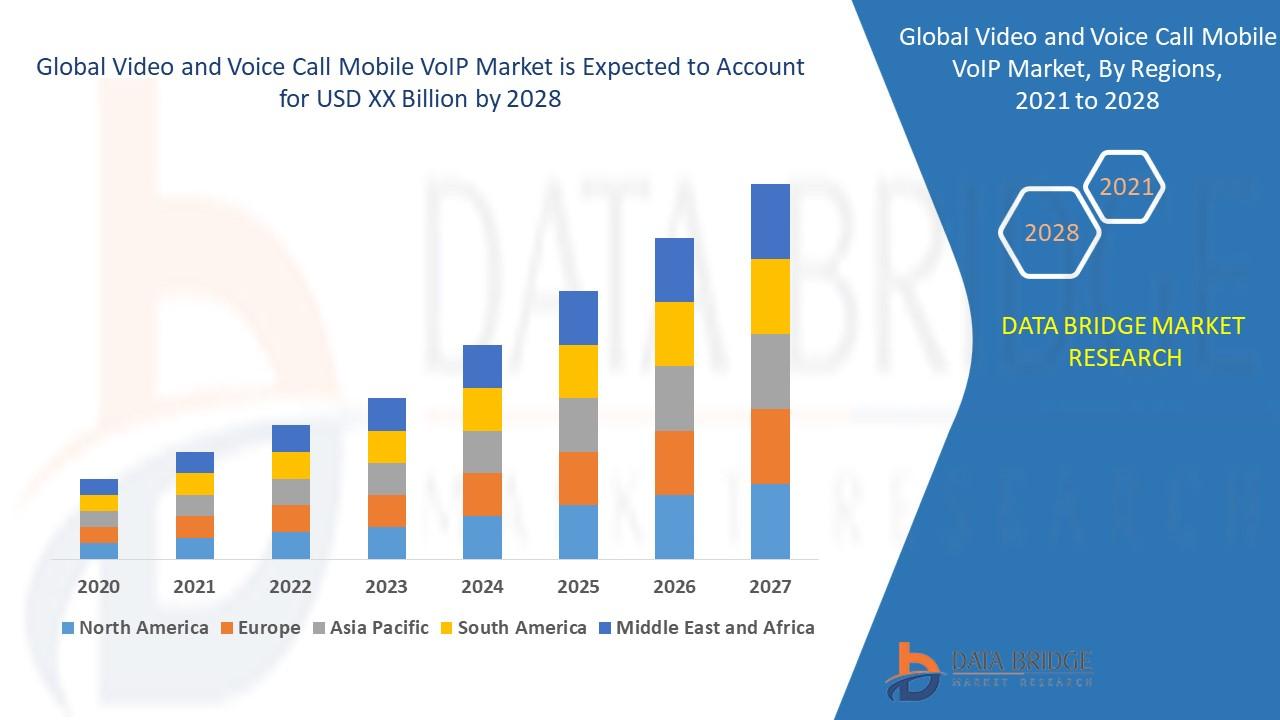

"Executive Summary: Video and Voice Call Mobile VoIP Market Size and Share by Application & Industry CAGR Value The global video and voice call mobile VoIP market size was valued at USD 15.2 billion in 2024 and is projected to reach USD 65.79 billion by 2032, with a CAGR of 20.10% during the forecast period of 2020.1 to 2032 The leading Video and Voice Call Mobile VoIP...

Online Cricket Betting is extremely popular amongst many Indians today, however it is very common for new cricket bettors to jump into the market without having a full understanding of their Cricket Betting ID and how it works. Because of this, many cricket bettors have experienced account being blocked, delayed withdrawals and further losses due to a lack of understanding of their...