Mastery Of Home Loan Bad Credit Requirements For New Investors

The landscape of real estate investment is often portrayed as a playground for the financially flawless, but the reality in 2026 is far more inclusive. For many aspiring moguls, the journey doesn't start with a perfect credit score; it starts with a strategic understanding of how to leverage available financial tools. Navigating home loan bad credit requirements is a specialized skill that allows you to acquire assets while your personal financial profile is still in a recovery phase. The modern market has moved away from a one-size-fits-all approach, recognizing that a borrower's past challenges do not always dictate their future success as a landlord or property manager. By mastering the specific criteria used by alternative lenders, you can bypass traditional gatekeepers and begin building a portfolio that generates long-term wealth.

The primary shift in 2026 has been toward asset-based lending, where the performance of the property takes center stage. Lenders are increasingly willing to overlook personal credit "dings" if the deal itself is fundamentally sound. This creates a massive opportunity for new investors who have the analytical skills to find undervalued properties but lack the pristine credit history required by major retail banks. Understanding the nuances of these requirements is the difference between staying a dreamer and becoming a deed-holder. It involves a shift in perspective—from seeing yourself as a consumer to seeing yourself as a business entity that is capable of managing income-producing real estate.

The Rise of Non-Conforming Financial Products

In a world where gig work and self-employment are the new norms, traditional mortgage products often fall short. This has led to the popularity of non QM loans, which are designed for borrowers who do not meet the "qualified mortgage" standards set by federal agencies. These loans are essential for investors because they offer flexibility in how income is documented and how credit history is interpreted. Instead of a hard "no" based on a score of 580 or 600, non-QM lenders look at your overall liquid assets, your down payment size, and your recent payment consistency. They provide a bridge for those who are financially capable but technically "unqualified" by legacy banking standards.

For an investor, these products are a tactical advantage. They often allow for higher debt-to-income ratios and can be used to finance properties that traditional lenders might consider too risky, such as non-warrantable condos or homes in need of significant cosmetic repair. While the interest rates are typically higher than a standard 30-year fixed prime loan, the ability to close a deal and start collecting rent often far outweighs the added interest cost. The goal is to use these loans to get into the game, improve the property, and eventually refinance once your credit score has naturally migrated upward due to your successful management of the new debt.

The Math Behind Modern Investment Approvals

When you move into the realm of investment, the most important acronym you will encounter is DSCR or the debt service coverage ratio. This is the metric that modern lenders use to determine if a property can pay for itself. Essentially, the lender divides the property's expected monthly rental income by the total monthly mortgage payment (including taxes, insurance, and association fees). In 2026, most specialized lenders look for a ratio of 1.15 to 1.25. This means the property should ideally generate 15% to 25% more in rent than it costs to maintain the loan. If the math works out favorably, your personal credit score becomes a secondary concern.

Mastering this calculation is vital because it allows you to "shop like a lender." Before you even apply for a loan, you can run the numbers on a potential purchase to see if it meets the DSCR threshold. If a property has a high enough cash flow, some lenders will even offer "no-ratio" loans where your personal income isn't even checked. They are essentially betting on the property's ability to produce revenue. This level of specialization is why many new investors are finding success despite having credit scores that would be laughed out of a local credit union. It is a data-driven approach that rewards those who do their homework on property values and market rents.

Strategic Steps for Financing a Rental Property

Successfully financing a rental property with less-than-perfect credit requires a different preparation checklist than buying a primary residence. First, you must be prepared to bring more equity to the table. While a first-time homebuyer might get away with 3.5% down, an investor with bad credit should aim for 20% to 25%. This "equity cushion" protects the lender and proves your commitment. Second, you should have a "cash reserve" equivalent to six months of mortgage payments. This shows the lender that you can handle a vacancy or an unexpected repair without defaulting on the loan.

Additionally, the role of a professional appraisal is amplified in investment deals. The lender will often order a "Rent Schedule" (Form 1007) alongside the standard appraisal to verify the fair market rent in the area. If you can provide documented proof that the neighborhood is seeing rising demand and increasing rental rates, you strengthen your case. Being an investor is about presenting a business case, not just a personal application. The more professional your presentation—including a detailed plan for property management and a clear exit strategy—the more likely a non-traditional lender is to approve your request.

Typical Investor Requirements Comparison

|

Metric |

Standard Bank Loan |

Non-QM Investor Loan |

|

Minimum Credit Score |

Usually 620 - 680 |

Can be as low as 500 - 580 |

|

Income Documentation |

2 Years Tax Returns/W-2s |

Bank Statements or DSCR based |

|

Down Payment |

15% - 25% |

20% - 30% (Higher for lower scores) |

|

Max Number of Properties |

Often capped at 10 |

Usually no limit |

Essential Documentation for Your Investor File

-

Detailed Rent Roll: If the property is already occupied, provide current lease agreements and payment history.

-

Entity Documents: Many investors close in the name of an LLC; have your Articles of Organization and EIN ready.

-

Asset Statements: Two months of statements showing enough cash for the down payment and required reserves.

-

Letter of Experience: A brief resume of any previous property management or construction experience.

-

Insurance Quote: A preliminary quote for a "Landlord Policy" which covers lost rent and liability.

Overcoming the Stigma of Financial Setbacks

The final piece of the mastery puzzle is psychological. Many potential investors count themselves out before they even try because they feel a sense of shame regarding their credit score. In the professional lending world of 2026, lenders do not view bad credit as a moral failing; they view it as a risk factor to be priced. If you have a 580 score, you might pay 2% more in interest than someone with a 780, but you still get the asset. Over a five-year period, the appreciation of that asset will likely dwarf the extra interest you paid. Don't let a temporary number prevent you from acquiring a permanent asset.

By focusing on the requirements that actually matter to alternative lenders—specifically the income potential of the real estate and your available liquidity—you can navigate the market with the same confidence as a seasoned pro. The "Mastery" in the title of this article refers to the ability to see the path where others see a wall. Real estate investment is a game of math and persistence. If you can find the right property and match it with the right non-conforming loan product, your credit score will eventually become a footnote in your success story. Start looking for properties that meet the DSCR test today, and you'll find that the doors of opportunity are much easier to open than you previously thought.

Categorias

Leia mais

Low energy and diminished physical results can be incredibly frustrating for those who value an active lifestyle. Often, the missing piece of the puzzle is hormonal health, which governs how our bodies recover and grow. Consulting with a specialist allows individuals to dive deep into their biological data to find real solutions. This medical intervention is designed to bridge the gap between...

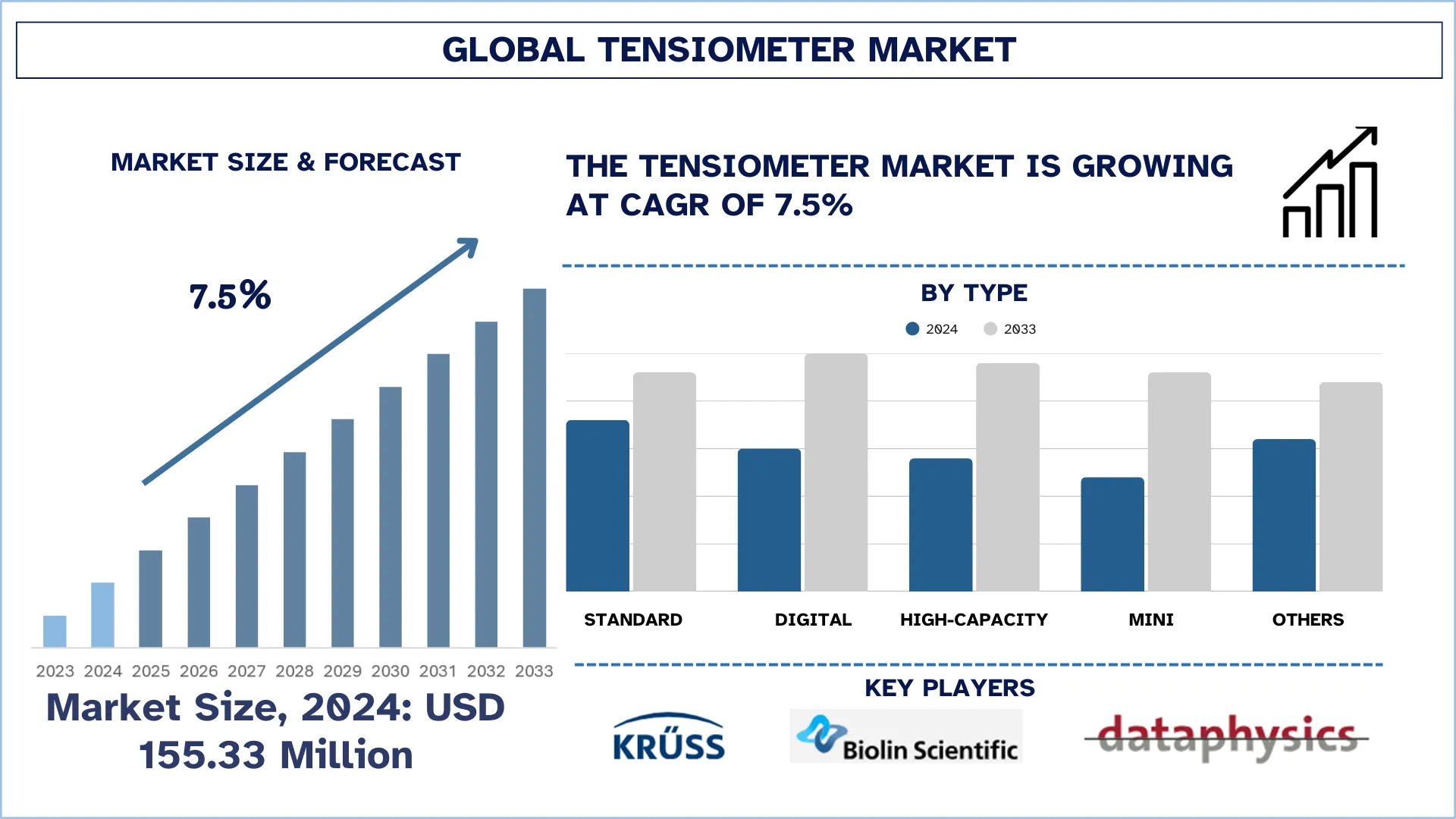

The Global Tensiometer Market was valued at USD 155.33 million in 2024 and is expected to grow at a strong CAGR of around 7.5% during the forecast period (2025-2033F), Increased funding of research allows the laboratories to upgrade their primitive equipment to high-end and automated tensiometers with greater accuracy and reproducibility, leading to the significant growth of the tensiometers...

The global Lithium Hydroxide Market Size is valued at USD 28.87 billion in 2025E and is projected to reach USD 92.19 billion by 2033, growing at a CAGR of 15.62% during the forecast period from 2026 to 2033. This strong growth reflects the accelerating demand for lithium-based materials driven by electrification trends and energy transition initiatives worldwide. Lithium hydroxide has...

The objective of this blog is to explore how geographic proximity and physical presence serve as powerful tools for business growth in the Pacific Northwest. The structure moves from the cultural nuances of the region to the technical execution of a trade show booth, emphasizing how local companies can outmaneuver national competitors by leveraging their physical location. By examining the...

In 2026, people are becoming more aware of the importance of daily health protection and immune support. With changing lifestyles, pollution, stress, and dietary habits, maintaining strong immunity has become a priority. New Era Protect is one of the trending supplements designed to support the immune system, improve overall health balance, and help the body stay protected against daily...