First Time Home Buyer Loans: Stop Renting And Start Owning

The dream of homeownership often feels like a distant light on the horizon, especially when you are caught in the cycle of monthly rent payments that seem to vanish into thin air. Many people believe that the path to owning a home is reserved for those with perfect financial histories and massive down payments. However, the modern lending landscape has evolved significantly to support those who are ready to transition from tenants to owners. Accessing first time home buyer loans is more attainable today than it has ever been, thanks to a variety of programs designed to lower the barrier to entry for newcomers to the real estate market.

Renting offers flexibility, but it lacks the one thing that builds long-term wealth: equity. Every time you write a check to a landlord, you are essentially paying off their mortgage and increasing their net worth. By shifting that same monthly expenditure toward your own property, you begin the process of forced savings. Over time, as property values appreciate and your loan balance decreases, you create a financial cushion that can fund your retirement, your children's education, or future business ventures. The transition might seem daunting, but breaking down the process into manageable steps makes the journey much clearer.

Finding Financing Options Despite Financial Hiccups

One of the biggest misconceptions in the housing market is that a less-than-stellar financial history automatically disqualifies you from buying a home. Life happens—medical bills, job transitions, or simple mistakes can impact your standing with credit bureaus. Fortunately, specialized lending products exist for those in need of mortgages for bad credit. These programs often look at the bigger picture, considering your consistent income and current debt-to-income ratio rather than just a single three-digit number. While the interest rates might be slightly higher than a traditional prime loan, the opportunity to enter the market and start building equity usually far outweighs the additional interest cost over the first few years.

Government-backed programs like the FHA loan are specifically tailored for this demographic. They allow for lower down payments and are much more forgiving regarding previous financial challenges. By utilizing these tools, you can secure a stable roof over your head while simultaneously working to improve your overall financial profile. Once your score improves and you have built up some equity, you can always look into refinancing into a more traditional product with better terms. The key is to get your foot in the door now rather than waiting for a perfect scenario that might never arrive.

Expanding Your Portfolio Beyond a Primary Residence

Once you have mastered the basics of purchasing your first home, you might find yourself looking at real estate as more than just a place to sleep. Many successful individuals use their first home as a springboard into the world of property management. Exploring investment property loans can open up a second stream of income that provides stability and growth. These types of loans differ from residential ones in that lenders often look at the potential income the property itself can generate. It is a powerful way to make your money work for you, creating a snowball effect of wealth generation.

When you move from being a renter to an owner, and then eventually to an investor, your perspective on money changes. You stop seeing housing as a monthly expense and start seeing it as an asset class. The transition requires a bit of a learning curve, especially regarding how to manage tenants and maintain a secondary structure, but the rewards are substantial. The tax benefits alone associated with owning additional properties can significantly impact your annual bottom line, making it a favorite strategy for those looking to build a legacy.

The Long-Term Value of Real Estate Assets

The historical trend of real estate values in most developed areas has been one of steady growth. While there are always cycles of booms and busts, the long-term trajectory is upward. This is why investing in rental properties remains a reliable way to secure your financial future. Unlike the stock market, which can be incredibly volatile and influenced by factors completely out of your control, real estate provides a tangible asset. You can see it, touch it, and make physical improvements to it to increase its value. You are in the driver's seat of your investment.

Furthermore, rental income typically keeps pace with inflation. As the cost of living goes up, so does the amount you can charge for rent. This provides a natural hedge against the eroding purchasing power of the dollar. For a first-time buyer, the ultimate goal isn't just to stop paying a landlord; it is to eventually become the one who provides quality housing to others while securing their own financial independence. It all starts with that first courageous step of applying for your initial loan and committing to the responsibilities of ownership.

Navigating the Modern Application Process

The digital age has made the application process for a mortgage much more transparent and streamlined. You no longer have to walk into a local bank with a mountain of paper files and hope for the best. Most of the preliminary work can be done from your smartphone or laptop. You can compare rates, check your eligibility, and upload documents in a matter of minutes. This ease of access has democratized the home-buying process, allowing people from all walks of life to compete in the housing market.

However, technology doesn't replace the need for a good strategy. It is important to have your documentation in order. This includes your tax returns, recent pay stubs, and a clear understanding of your monthly outgoings. Lenders want to see that you are responsible and have a plan for repayment. Even if your history has some spots on it, showing a recent trend of financial stability and a clear understanding of your budget goes a long way in convincing a loan officer to take a chance on you.

Steps to Prepare for Your First Purchase

-

Check your credit report for errors and dispute any inaccuracies immediately.

-

Save a dedicated fund for closing costs, which usually range from 2% to 5% of the purchase price.

-

Get a pre-approval letter to show sellers that you are a serious and capable buyer.

-

Research local grants or down payment assistance programs available for first-timers.

-

Keep your job stable during the application process to avoid red flags with the lender.

Typical Costs of Ownership vs. Renting

|

Expense Category |

Renter Perspective |

Owner Perspective |

|

Monthly Payment |

Pure expense, likely to increase annually. |

Partially builds equity, fixed if on a 30-year term. |

|

Maintenance |

Managed by landlord (included in rent). |

Owner's responsibility (adds to property value). |

|

Tax Benefits |

None. |

Mortgage interest and property tax deductions. |

|

Customization |

Limited by lease agreement. |

Complete freedom to renovate and improve. |

Building a Future Through Ownership

The psychological shift that occurs when you receive the keys to your own home is profound. There is a sense of pride and permanence that a rental agreement simply cannot provide. You are no longer a guest in someone else's building; you are the master of your own domain. This stability often leads to better community involvement and a stronger sense of belonging. Children who grow up in owned homes often have better educational outcomes due to the stability of their living situation. The benefits of homeownership ripple out far beyond your bank account.

As you move forward, remember that your first home doesn't have to be your forever home. It is a starting point. Many people buy a modest condo or a small starter house, live in it for a few years while the value grows, and then use the proceeds to buy something larger or more suited to their changing needs. The most important part of the journey is getting started. Don't let the fear of a complex process or a less-than-perfect credit score keep you on the sidelines. The tools and programs are there; you just need to reach out and take advantage of them.

The path from renting to owning is paved with information and opportunity. By understanding the various loan products available, including those for varying credit levels and investment goals, you can navigate the market with confidence. The transition requires discipline and a bit of research, but the reward is a lifetime of financial security and the personal satisfaction of owning a piece of the world. Stop contributing to your landlord's wealth and start building your own today. The market is waiting for you, and your future self will thank you for the decision to invest in a home of your own.

Categorias

Leia Mais

Plant-derived actives are steadily replacing synthetic alternatives across pharmaceuticals, personal care, and agriculture, and neem stands out as one of the most versatile botanicals driving this shift. The Neem Extracts Market is valued at US$ 2.09 billion in 2025 and is projected to climb to US$ 5.84 billion by 2034, expanding at a CAGR of 12.11% between 2026 and 2034. That trajectory...

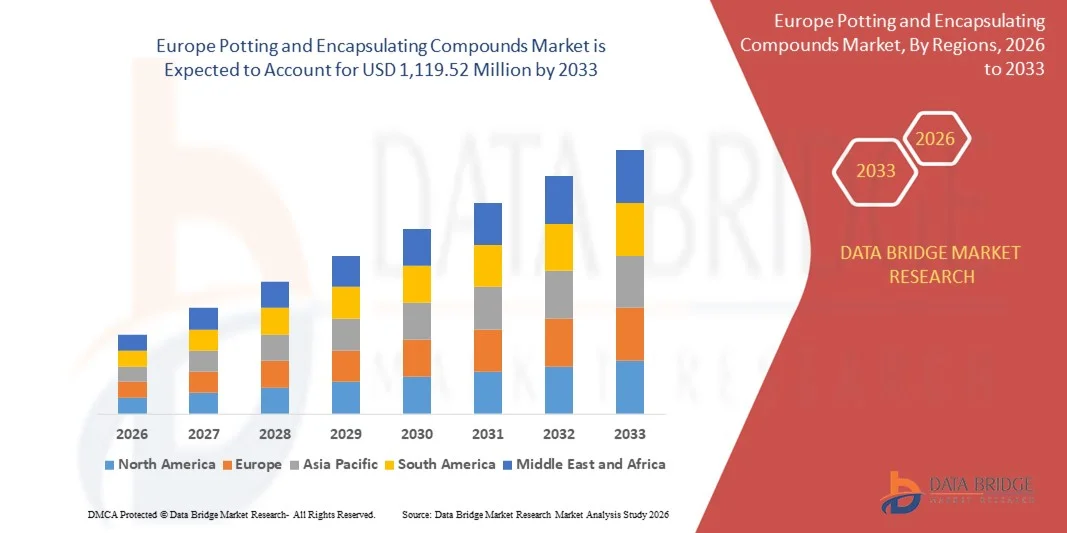

"Executive Summary Europe Potting and Encapsulating Compounds Market Size and Share Forecast CAGR Value The Europe potting and encapsulating compounds market size was valued at USD 799.39 million in 2025 and is expected to reach USD 1,119.52 million by 2033, at a CAGR of 4.30% during the forecast period The Europe Potting and Encapsulating Compounds...

Introduction to Link Bola88 Link Bola88 serves as a gateway for sports enthusiasts who enjoy online betting, particularly in football and other popular sports. This platform is designed to offer users an accessible and seamless experience, allowing them to place bets quickly while staying updated on live match results. Its focus on convenience, security, and variety has made it a preferred...

In Odin: Valhalla Rising, some boss encounters stop feeling like simple fights and start feeling like endurance tests designed to punish every mistake in your build, Odin Valhalla Rising Diamonds, and even your patience. Ouroboros is one of those encounters. This guide breaks down how the fight works, why preparation matters more than raw damage, and how a flexible gear-swap and...

A web development company UAE provides end-to-end digital solutions, including custom website design, responsive development, and advanced mobile applications. These companies focus on delivering user-friendly, fast, and SEO-optimized websites that help businesses build a strong online presence. With the rise of mobile users, App Development Dubai has become a crucial service, enabling...