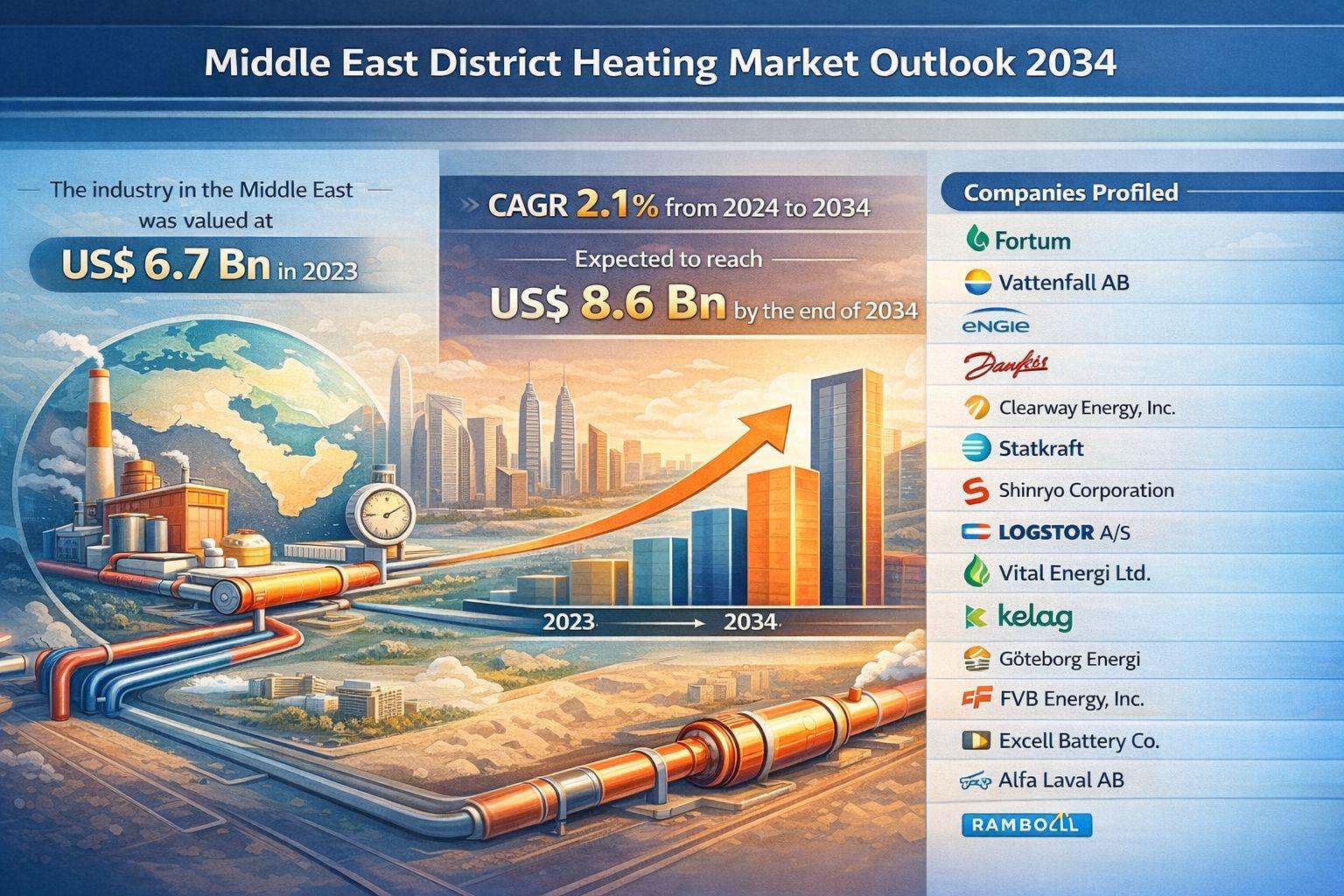

Middle East District Heating Market to Reach US$ 8.6 Bn by 2034 Driven by Renewable Integration and Smart Energy Systems

The Middle East district heating market is experiencing steady yet strategic growth, supported by rapid urbanization, rising awareness about energy efficiency, and government-backed sustainability initiatives. Valued at US$ 6.7 Bn in 2023, the market is projected to expand at a CAGR of 2.1% from 2024 to 2034, reaching US$ 8.6 Bn by the end of 2034.

Analysts highlight that technological advancements—such as smart grid integration, digital monitoring systems, and advanced control mechanisms—are transforming traditional district heating infrastructure into more efficient and reliable systems. These innovations are enabling better demand forecasting, energy optimization, and cost control.

A notable trend shaping the market is the increasing adoption of renewable energy sources, including solar thermal energy and waste heat recovery systems. Governments across the region are implementing policies to reduce carbon emissions, thereby encouraging investments in cleaner heating solutions. As a result, district heating is emerging as a vital component of the Middle East’s decarbonization roadmap.

Market Introduction

District heating refers to a centralized system that supplies heat to multiple buildings through a network of insulated pipelines. Instead of individual heating systems in each building, a central plant generates heat using energy sources such as natural gas, biomass, geothermal energy, or waste heat.

The heat—distributed in the form of hot water or steam—is transported through underground pipelines to residential, commercial, and industrial facilities. This centralized approach significantly improves energy efficiency and reduces operational costs.

District heating systems are widely used in:

- Residential complexes

- Commercial spaces such as malls and offices

- Institutional buildings including hospitals and schools

- Industrial facilities requiring process heat

These systems eliminate the need for individual heating units, thereby reducing maintenance costs and saving space. Additionally, they contribute to lower greenhouse gas emissions, making them an environmentally sustainable solution.

Another advantage is their compatibility with district cooling systems, enabling year-round climate control. This dual functionality is particularly beneficial in the Middle East, where cooling demand is high.

Key Market Drivers

Rise in Investment in Renewable Energy-based Systems

The transition toward renewable energy is one of the most significant drivers of the Middle East district heating market. While fossil fuels still dominate heat generation in the region, there is a growing shift toward sustainable alternatives.

District heating systems act as energy hubs, capable of integrating multiple renewable sources such as:

- Solar thermal energy

- Geothermal energy

- Biomass

- Waste heat recovery

These systems can store excess heat generated during peak production periods and redistribute it when demand rises. According to projections aligned with global energy transition goals, renewable energy and electricity could account for approximately 35% of district heating supply in the coming decades, significantly reducing carbon emissions.

This transition is not only environmentally beneficial but also economically viable, as it lowers long-term energy costs and enhances energy security.

Favorable Government Policies and Regulations

Government initiatives play a crucial role in accelerating the adoption of district heating systems. Countries across the Middle East are implementing policies to reduce greenhouse gas emissions and achieve net-zero targets by 2050.

Key policy measures include:

- Subsidies and tax incentives for district heating projects

- Regulatory frameworks promoting clean energy adoption

- Financial support for infrastructure development

- Incentives for end-users to adopt centralized heating

These measures are encouraging both public and private sector investments in district heating infrastructure. Moreover, policy stability is enhancing investor confidence and facilitating long-term project planning.

The push for decarbonization is particularly strong in urban areas, where centralized heating systems can efficiently serve densely populated regions.

High Demand for Combined Heat & Power (CHP) Systems

Combined Heat & Power (CHP) systems are expected to dominate the market during the forecast period. These systems simultaneously generate electricity and heat from a single energy source, achieving efficiency levels of up to 80% or higher.

In CHP systems:

- Fuel (natural gas, biomass, or waste) is used to generate electricity

- Waste heat from electricity generation is captured and reused for heating

- This dual-output system reduces energy wastage and fuel consumption

The integration of CHP systems into district heating networks offers several advantages:

- Improved energy efficiency

- Reduced greenhouse gas emissions

- Lower operational costs

- Enhanced energy reliability

As energy demand continues to rise in the Middle East, CHP systems are becoming a preferred solution for sustainable and efficient energy generation.

Key Market Trends

Integration of Smart Technologies

Digitalization is transforming district heating systems across the Middle East. Smart grids, IoT-enabled sensors, and AI-based analytics are enabling real-time monitoring and optimization of energy consumption.

These technologies help in:

- Predicting energy demand

- Reducing transmission losses

- Enhancing system reliability

- Lowering operational costs

Smart district heating networks are expected to play a critical role in future urban infrastructure.

Growing Adoption of Waste Heat Recovery

Waste heat recovery is gaining traction as an efficient way to utilize excess heat generated from industrial processes and power plants. Instead of releasing heat into the environment, it is captured and reused for district heating.

This approach not only improves energy efficiency but also reduces environmental impact, making it a key trend in the market.

Regional Outlook

The UAE emerged as the leading country in the Middle East district heating market in 2023, driven by strong infrastructure development and significant investments in sustainable energy solutions. The country’s focus on smart cities and green buildings is further boosting demand.

Saudi Arabia is another key market, supported by its ambitious Vision 2030 initiative, which emphasizes sustainability and energy diversification. The country is investing heavily in modern infrastructure and renewable energy projects.

Qatar has also made notable progress, particularly in preparation for global events such as the FIFA World Cup, which accelerated infrastructure development and energy-efficient solutions.

Meanwhile:

- Jordan is prioritizing renewable energy integration

- Oman and Kuwait are witnessing growing interest due to urban expansion and environmental concerns

Overall, regional growth is influenced by varying levels of economic development, policy frameworks, and infrastructure investments.

Competitive Landscape and Key Players

The Middle East district heating market is characterized by a mix of global and regional players focusing on innovation, partnerships, and sustainability.

Key companies operating in the market include:

- Fortum

- Vattenfall AB

- Engie

- Danfoss

- Clearway Energy, Inc.

- Statkraft

- Shinryo Corporation

- LOGSTOR A/S

- Vital Energi Ltd.

- Alfa Laval AB

- Ramboll Group A/S

- Helen Ltd.

These companies are investing in advanced technologies, expanding their geographic presence, and forming strategic collaborations to strengthen their market position.

Key Developments

Recent developments highlight the growing investment activity in the district heating sector:

- In March 2021, Fortum sold its Baltic district heating business to Partners Group for EUR 800 million, signaling strategic portfolio optimization.

- In December 2020, Mubadala, a sovereign investment firm based in Abu Dhabi, acquired a significant stake in a district heating investment platform focused on geothermal energy systems.

These developments indicate increasing investor interest and a shift toward sustainable energy solutions.

Market Outlook

The Middle East district heating market is set to witness steady growth over the next decade. While the CAGR of 2.1% indicates moderate expansion, the market’s long-term potential lies in sustainability-driven transformation.

Key factors shaping the future include:

- Expansion of renewable energy integration

- Adoption of smart and digital technologies

- Government support for decarbonization

- Increasing demand for energy-efficient infrastructure

As urbanization accelerates and environmental concerns intensify, district heating systems are expected to play a crucial role in shaping the region’s energy landscape.

In conclusion, the Middle East district heating market represents a stable yet evolving sector, driven by innovation, policy support, and the global transition toward cleaner energy.

Categories

Read More

ฟุตบอลโลกเป็นการแข่งขันฟุตบอลระดับโลกที่รวมทีมชาติชั้นนำจากทุกทวีปมาแข่งขันกันอย่างเข้มข้นในทุกแมตช์ ความน่าสนใจไม่ได้อยู่แค่ผลการแข่งขันในสนาม แต่ยังรวมถึงการวิเคราะห์เกมและการเพิ่มประสบการณ์ผ่านการ พนันบอลโลก ซึ่งช่วยให้การรับชมมีความตื่นเต้นมากขึ้น และทำให้ผู้เล่นได้ใช้ความรู้ด้านฟุตบอลมาประกอบการตัดสินใจอย่างมีเหตุผลมากยิ่งขึ้น ภาพรวมของฟุตบอลโลกกับความหลากหลายของเกมการแข่งขัน...

The industry of sports gaming continues to grow with shifting user expectations and technological developments. Websites now focus on delivering faster, smarter, more engaging experiences. Gold365 highlights some of the key trends in this changing landscape that are shaping user perceptions of online gaming. Customers can discover more about how sites are evolving to address modern needs by...

In today’s eco-conscious landscaping industry, the Electric Garden Loader is emerging as a quiet revolution, seamlessly blending clean energy with rugged outdoor performance for professional and personal use alike. Garden and landscape professionals often face challenges involving tight spaces, delicate terrain, and environmental restrictions. Traditional machines, while powerful, can be...

"Global Executive Summary Asia-Pacific Robotic Vacuum Cleaner Market: Size, Share, and Forecast Data Bridge Market Research analyses that the Asia-Pacific robotic vacuum cleaner market which was USD 2.58 billion in 2022, is expected to reach USD 16.01 billion by 2030, and is expected to undergo a CAGR of 25.60% during the forecast period of 2023 to 2030.The complete Asia-Pacific Robotic...

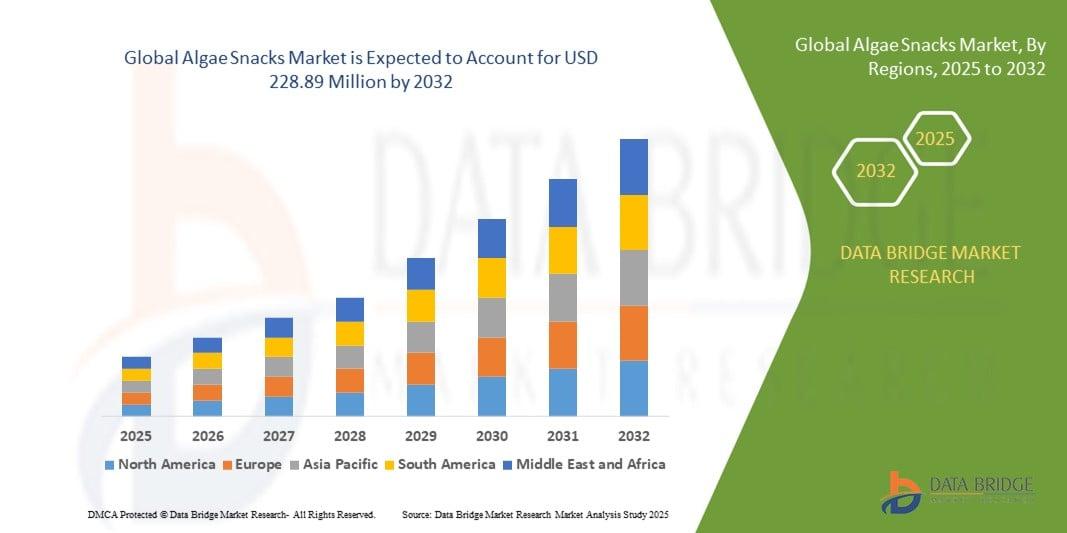

"Algae Snacks Market Summary: According to the latest report published by Data Bridge Market Research, the Algae Snacks Market The global algae snacks market size was valued at USD 105.24 million in 2024 and is expected to reach USD 228.89 million by 2032, at a CAGR of 10.20% during the forecast period With the clear understanding of customer requirement,...