A Deep Dive Into Modern Property Acquisition and Risk Mitigation

The landscape of the housing market has shifted from a rigid, institutional framework into a more nuanced ecosystem that rewards strategic planning. For many years, the path to ownership was a narrow gate guarded by standard banking protocols that favored a very specific type of earner. However, as the workforce evolves toward freelancing and entrepreneurship, the methods for evaluating creditworthiness must also adapt. Whether you are focused on buying a rental property or securing a primary residence, success now depends on a comprehensive analysis of the available financial mechanisms. Understanding how risk is calculated in a modern context allows you to navigate hurdles that once seemed insurmountable.

One significant development in the lending industry is the growth of non qm loans. These instruments represent a departure from the one-size-fits-all criteria of the past, focusing instead on the holistic health of a borrower's portfolio. From an analytical perspective, these products fill a vital gap for those with high net worth but low taxable income, such as small business owners with significant expenses. By evaluating 12 to 24 months of cash flow rather than just tax returns, these lenders apply a more realistic lens to the borrower’s ability to manage a mortgage. This shift in perspective has democratized access to capital for a large segment of the modern economy.

Evaluating the Economic Impact of Individual Liability

Lenders utilize specific metrics to quantify the risk of a potential default. A primary indicator used in this assessment is the debt ratio. This figure provides a mathematical snapshot of how much of your monthly gross income is already committed to other obligations. Analytically, a lower percentage indicates a higher capacity to absorb financial shocks, such as a temporary loss of income or an unexpected repair. Reducing your recurring liabilities before applying for a loan is not just a cosmetic improvement; it is a fundamental shift in your financial risk profile that can result in more favorable interest rates and higher borrowing limits.

The Statistical Reality of Credit Recovery

There is a common misconception that a history of financial mistakes creates a permanent barrier to ownership. However, buying a house with bad credit is an achievable objective when approached with a data-driven strategy. Statistical analysis shows that recent payment behavior is often a more accurate predictor of future performance than mistakes made several years ago. Lenders who specialize in these areas look for a trend of improvement. By demonstrating twelve to eighteen months of perfect payment history on current obligations, you provide the evidence needed to offset the impact of an older bankruptcy or a series of late payments from a previous economic downturn.

Quantitative Analysis of Real Estate as an Investment

When transitioning from a homeowner to an investor, the analytical focus must shift toward the property’s performance as a standalone asset. This involves calculating the capitalization rate, which compares the net operating income to the purchase price. A thorough analysis must account for property management fees, estimated vacancy rates, and a reserve fund for capital expenditures. Successful investors do not rely on speculation of rising prices; they rely on the certainty of cash flow. By stress-testing your numbers against a variety of economic scenarios, you ensure that the investment remains viable even if the local market experiences a temporary cooling period.

The Correlation Between Down Payments and Loan Terms

The amount of capital you commit upfront has a direct correlation with the long-term cost of your mortgage. Analytically, a larger down payment serves two purposes: it reduces the loan-to-value percentage, which lowers the lender's risk, and it typically eliminates the need for private mortgage insurance. Over a thirty-year period, the compound savings from a lower interest rate and the absence of insurance can amount to a staggering sum. Buyers should weigh the benefits of entering the market quickly with a small down payment against the long-term financial efficiency of waiting until they have a more substantial equity stake to offer at the closing table.

Infrastructure of Alternative Lending Markets

The secondary mortgage market plays a crucial role in how non-traditional loans are funded. Unlike government-backed loans that are bundled into securities, many specialized products are held in private portfolios. This allows for more flexible underwriting because the lender is not beholden to the same rigid federal guidelines. Analyzing the differences between these two structures helps a borrower understand why a private lender might be comfortable with a unconventional income source that a large commercial bank would reject. This internal flexibility is the engine that drives innovation in the real estate finance sector today.

Managing Liquidity for Long-Term Solvency

A critical component of a successful purchase is the post-closing liquidity position. It is analytically dangerous to exhaust all available cash on the down payment and closing costs. Lenders often require "reserves," which are liquid funds equal to a certain number of months of mortgage payments. Maintaining a robust emergency fund ensures that you can weather the unexpected without falling into a cycle of high-interest debt. For the savvy borrower, the goal is to balance the desire for the lowest possible monthly payment with the necessity of maintaining a safety net that protects their overall net worth and financial stability.

Strategic Portfolio Diversification Through Property

Real estate offers a unique analytical advantage through the power of leverage. Unlike stocks, where you typically must pay the full price for the asset, property allows you to control a high-value asset with a relatively small percentage of your own capital. This amplifies the return on equity. However, this leverage must be managed carefully. A diversified portfolio might include a mix of traditional residential units, short-term vacation rentals, and perhaps commercial space. By spreading risk across different sectors of the real estate market, an investor can protect themselves against localized economic shifts that might affect one specific property type more than others.

Final Synthesis of Borrowing Strategies

Navigating the path to property ownership requires a synthesis of market knowledge, self-assessment, and the clever application of financial tools. By analyzing your current standing through the eyes of a lender—focusing on your earnings-to-expense balance and your recent credit trends—you can identify the most efficient route forward. Whether you are leveraging the flexibility of specialized loan products or working to repair your standing after a setback, the key is to remain focused on the data. A well-informed buyer is not just a participant in the market; they are a strategist capable of turning financial obstacles into long-term wealth building opportunities.

Categorias

Leia mais

A new adaptation of Joan Didion's 1996 novel is now in production. The film, titled 'The Last Thing He Wanted,' is being directed by Dee Rees. Anne Hathaway stars as the journalist Elena McMahon. Her journey into the Iran-Contra affair's perilous arms trade forms the core of the story. The supporting cast includes acclaimed actors like Ben Affleck and Willem Dafoe. Rosie Perez, Toby Jones, and...

"Future of Executive Summary Advanced Process Control Market: Size and Share Dynamics CAGR Value Data Bridge Market Research analyses that the advanced process control market will exhibit a CAGR of 8.10% for the forecast period of 2021-2028. Therefore, the advanced process control market would stand tall by USD 31.66 billion by 2028. Businesses can attain detailed insights with the large...

The Indian Premier League continues to dominate the cricket world, bringing unmatched excitement to fans and bettors alike. Among the highly anticipated fixtures, SRH vs PBKS stands out as a thrilling contest filled with explosive batting, strategic bowling, and unpredictable moments. For Indian cricket enthusiasts looking to make the most of this action, having a secure and reliable...

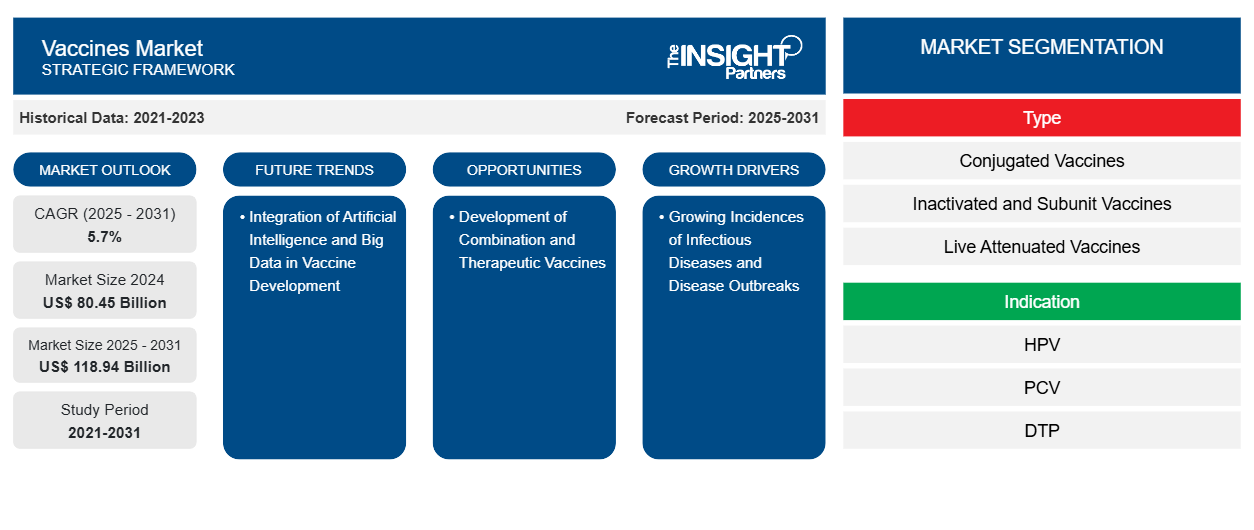

The global vaccines market is currently undergoing a period of unprecedented transformation, characterized by rapid technological shifts and a widening of the target patient demographic. According to the latest industry analysis by The Insight Partners, the global vaccines market was valued at US$ 80.45 billion in 2024 and is projected to reach US$ 118.94 billion by 2031, progressing at a CAGR...

Finding the right therapist can be life-changing, especially when language and cultural understanding play a crucial role in communication. For Persian-speaking individuals living in Toronto, working with a Farsi therapist can make therapy more comfortable, relatable, and effective. If you are searching for a Farsi therapist Toronto, Airsing Bliss offers a supportive and culturally...