Have You Ever Wondered How Professionals Fund Real Estate Without Bank Approvals?

The world of finance often feels like a gated community where only those with a perfect history are allowed inside. It is natural to feel frustrated when you have the capital and the drive but do not meet the rigid criteria of a traditional lending institution. One of the most frequent inquiries from aspiring homeowners is can you buy a house with bad credit when the big banks say no. The answer is a resounding yes, provided you are willing to look beyond the standard mortgage products and explore the thriving world of private and alternative capital that exists specifically to help people in your exact situation.

What Makes Alternative Lending Different?

If you have been turned away by a local branch, it is likely because they only offer products that fit into a very small box. However, the market for Non QM loans is vast and designed specifically for the outliers. These are not subprime products from the past; they are sophisticated financial tools for people with diverse income streams, such as freelancers, small business owners, or those with significant liquid assets. By focusing on your overall ability to pay rather than just a historical score, these lenders provide a pathway to ownership that recognizes the reality of the modern economy.

Is It Time to Focus on Your Business Potential?

For many, the most effective way to enter the market is to stop looking for a personal home and start looking for an investment property that pays for itself. When you approach a purchase as a business venture, the conversation with the lender changes entirely. They stop looking at your personal debt-to-income ratio and start looking at the revenue potential of the real estate itself. This shift in perspective can be incredibly liberating, as it allows you to leverage the value of the asset to overcome any personal financial hurdles you might be facing.

How Do You Prove a Deal is Worth the Risk?

The secret weapon of the professional investor is the debt coverage ratio formula which is the primary tool used to justify a loan on a rental unit. This calculation compares the expected monthly rent to the total monthly mortgage obligation. If the rent is significantly higher than the payment, the lender feels secure knowing the property is a self-sustaining entity. By mastering this math, you can present a deal to a lender that is based on hard data and proven income, making your personal credit history a secondary concern in the overall approval process.

Can You Really Close a Deal with These Tools?

Success in this arena comes down to preparation and the quality of the deal you bring to the table. Lenders who work in the alternative space are looking for common-sense solutions. If you can show that you have a solid down payment and that the property you are buying is in a high-demand area, you are halfway to a closing. The process is often faster than a traditional loan because these lenders are not bogged down by the same level of federal bureaucracy, allowing you to move quickly when a great opportunity arises.

Why Does This Approach Work for Modern Buyers?

The traditional banking model was built for a world where everyone had a single employer for thirty years. Today’s world is different. We have more entrepreneurs, more remote workers, and more people building wealth through diverse portfolios. Alternative lending products reflect this new reality. They allow for a more nuanced view of risk, taking into account your current cash flow, your professional experience, and the underlying value of the real estate market in which you are participating.

What Are the Next Steps for Your Journey?

If you are ready to move forward, the first step is to stop asking for permission from traditional banks and start looking for partners in the private lending space. Look for mortgage professionals who specialize in non-traditional documentation and investor-focused loans. Gather your bank statements, research the rental rates in your target neighborhood, and run the numbers on a few potential properties. You will likely find that the obstacles you thought were insurmountable are actually just minor hurdles on the path to a successful closing.

Is Now the Right Time to Buy?

Many people hesitate because they are waiting for the perfect market conditions, but the truth is that the best time to buy real estate is when you find a deal that makes sense mathematically. By using flexible financing now, you can secure an asset that will likely appreciate over the next decade. You can always refinance later if rates drop or your credit improves, but you can never go back and buy a property at today's prices. Taking action now with the tools available to you is the surest way to build long-term security and wealth.

Real estate ownership is a powerful tool for financial freedom, and it shouldn't be reserved only for those with a flawless past. By understanding the alternatives and focusing on the performance of the assets you buy, you can navigate the market with confidence and achieve your goals on your own terms. The opportunities are out there; it is simply a matter of knowing which questions to ask and which tools to use to unlock them.

Κατηγορίες

Διαβάζω περισσότερα

Benefits of Using Certification Exam Preparation Material Certification exams help people grow in their careers. They help you get better jobs. They also help you earn more money. Many students want to pass the AE-Adult-Echocardiography exam on the first attempt. This exam is offered by ARDMS. However, exam preparation can feel difficult. There are many books to read and many topics to cover....

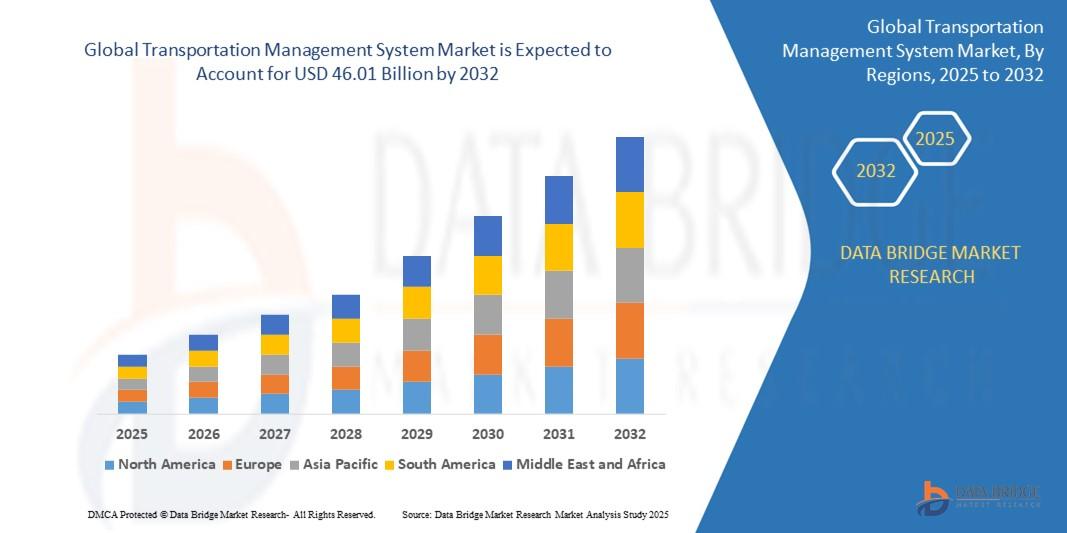

"Competitive Analysis of Executive Summary Transportation Management System Market Size and Share CAGR Value The global transportation management system market was valued at USD 15.25 billion in 2024 and is expected to reach USD 46.01 billion by 2032During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 14.80 % primarily driven by the increasing demand...

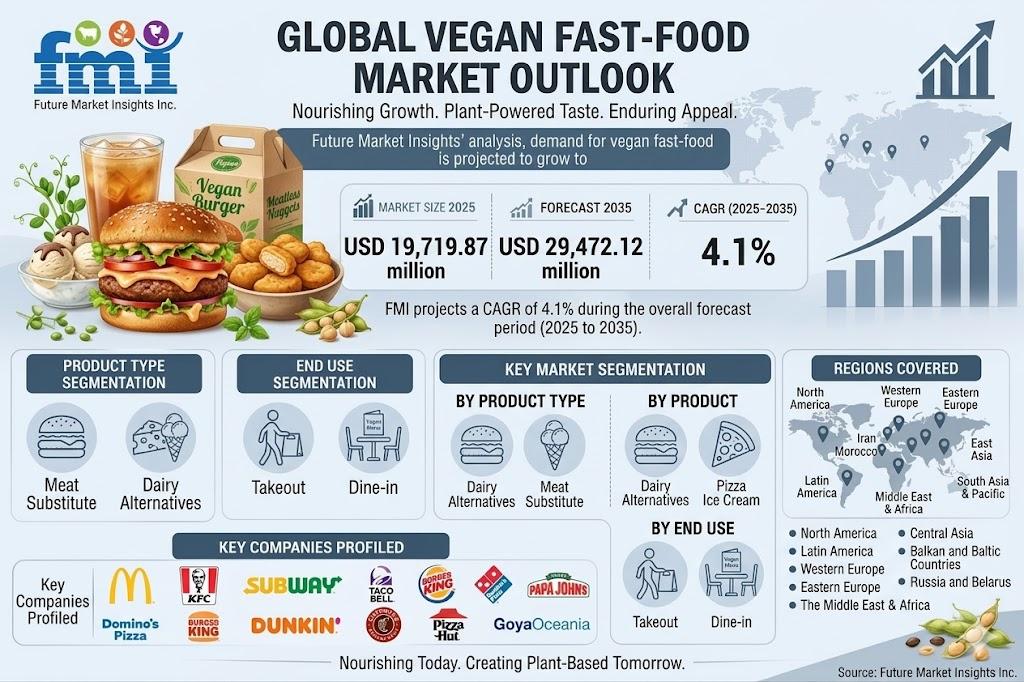

NEWARK, Del., USA | April 8, 2026 — According to the latest market analysis by Future Market Insights, the global vegan fast-food market is witnessing steady expansion as consumers increasingly shift toward plant-based diets driven by health, environmental, and ethical considerations. Valued at USD 19,719.87 million in 2025, the market is projected to reach USD 29,472.119 million by 2035,...

The world of online casino entertainment has expanded rapidly, and one of the most searched terms today is Slot Pragmatic a phrase closely linked with modern digital slot experiences. Players looking for exciting gameplay, engaging themes, and high-quality graphics often come across this term while exploring casino platforms. Many users also visit resources like this guide on to understand how...

"Latin America Cochlear Implants Market Summary: According to the latest report published by Data Bridge Market Research, the Latin America Cochlear Implants Market The Latin America cochlear implants market size was valued at USD 188.50 billion in 2025 and is expected to reach USD 450.30 billion by 2033, at a CAGR of 11.50% during the forecast period...