Breaking Down the Process of Homeownership Beyond Conventional Ideas

The quest for a new home is often filled with excitement, late-night browsing of real estate apps, and perhaps a bit of anxiety about the financial hurdles ahead. Many prospective buyers find that a conventional loan serves as a versatile bridge between their current savings and their future front door. Unlike government-insured options, these mortgages follow guidelines set by private entities, which often results in more competitive interest rates and flexible terms for those who have maintained a healthy credit profile over the years. It is a classic choice for many because it allows for a variety of property types, including second homes or investment properties, which are sometimes restricted under other programs.

The Hidden Mechanics of Mortgage Verification

After you have found the perfect kitchen and a backyard with just the right amount of sun, your application moves into a phase that many find mysterious. This stage of underwriting involves a meticulous deep dive into your financial history by a professional who assesses the viability of the deal. They verify your tax returns, bank statements, and debt obligations to ensure that the mortgage is a safe bet for both you and the institution. While it may feel like a high-stakes investigation, it is actually a protective measure designed to confirm that the monthly commitment fits comfortably within your existing lifestyle and long-term financial goals.

Comparing the Two Giants of the Lending World

One of the first forks in the road for any buyer is the debate of fha vs conventional when deciding which program fits their unique situation. The primary difference usually boils down to the flexibility of credit requirements and the structure of mortgage insurance. While one might offer a lower barrier to entry for those still building their credit, the other often provides a more cost-effective solution in the long run because the private mortgage insurance can eventually be cancelled once you reach a certain amount of equity. Evaluating these two paths requires a clear understanding of your current credit score and how much cash you have available to cover upfront costs versus monthly premiums.

Calculating the True Cost of Your Entrance Fee

A major milestone in the planning process involves determining how much down payment for a house is necessary to secure the keys without draining your emergency fund. While the old-fashioned advice suggested a full twenty percent of the purchase price, modern lending standards have evolved to allow for much smaller initial investments. Many buyers are surprised to learn that they can enter the market with as little as three percent down, though it is important to remember that a smaller initial stake usually results in higher monthly payments. Balancing your desire for immediate homeownership with the long-term cost of borrowing is the secret to a sustainable mortgage strategy.

The Impact of Debt-to-Income Ratios

Lenders look closely at your debt-to-income ratio to see how much of your monthly paycheck is already spoken for by car notes, student loans, or credit card balances. Keeping this ratio low is essential because it gives you more purchasing power when you finally go to make an offer. If your existing debts are too high, it might limit the amount a bank is willing to lend you, regardless of how much you earn. Most experts recommend paying down high-interest debt before starting the home search to ensure you qualify for the best possible terms.

Credit Score Nuances and Interest Rates

Your credit score is perhaps the most influential number in your financial life when it comes to buying a home. A difference of just fifty points can translate into a significantly higher interest rate, which adds up to tens of thousands of dollars over thirty years. Monitoring your credit report for errors and avoiding new large purchases during the home-buying process are two of the smartest moves you can make. The higher your score, the more leverage you have to negotiate better terms and lower fees with your chosen lender.

Budgeting for More Than Just a Mortgage

Owning a home comes with expenses that go far beyond the monthly principal and interest payments. Property taxes, homeowners insurance, and maintenance costs should all be factored into your monthly budget from the very beginning. Many new owners find themselves caught off guard by a leaking roof or a broken HVAC system in the first year of ownership. Creating a dedicated house fund for these inevitable repairs ensures that your dream home does not become a financial burden when life happens.

The Importance of a Pre-Approval Letter

In a competitive real estate market, having a pre-approval letter in hand is like having a VIP pass to the front of the line. It shows sellers that a lender has already looked at your finances and is committed to backing your purchase. This document is different from a simple pre-qualification, as it involves a more rigorous check of your documentation. Having this ready allows you to move quickly when you find a property you love, giving you a distinct advantage over other buyers who may still be waiting for their paperwork to clear.

Navigating the Closing Process

Once your offer is accepted and the inspections are complete, you head toward the finish line known as closing. This involves a final review of the loan terms, signing a significant amount of legal paperwork, and paying the remaining closing costs. These costs cover administrative tasks like title searches and recording fees. It is the final hurdle before the house officially becomes yours. Understanding each line item on your closing disclosure form helps ensure there are no surprises during those final moments at the settlement table.

The Long-Term Rewards of Equity

As you make payments each month, you are slowly building equity, which is the portion of the home you truly own. Over time, as property values rise and your loan balance decreases, this equity becomes a powerful financial asset. You can eventually use it for home improvements, to fund an education, or as a nest egg for retirement. This transition from being a renter to being an owner is not just about having a place to live; it is about building a foundation for future wealth and stability for yourself and your family.

Categories

Read More

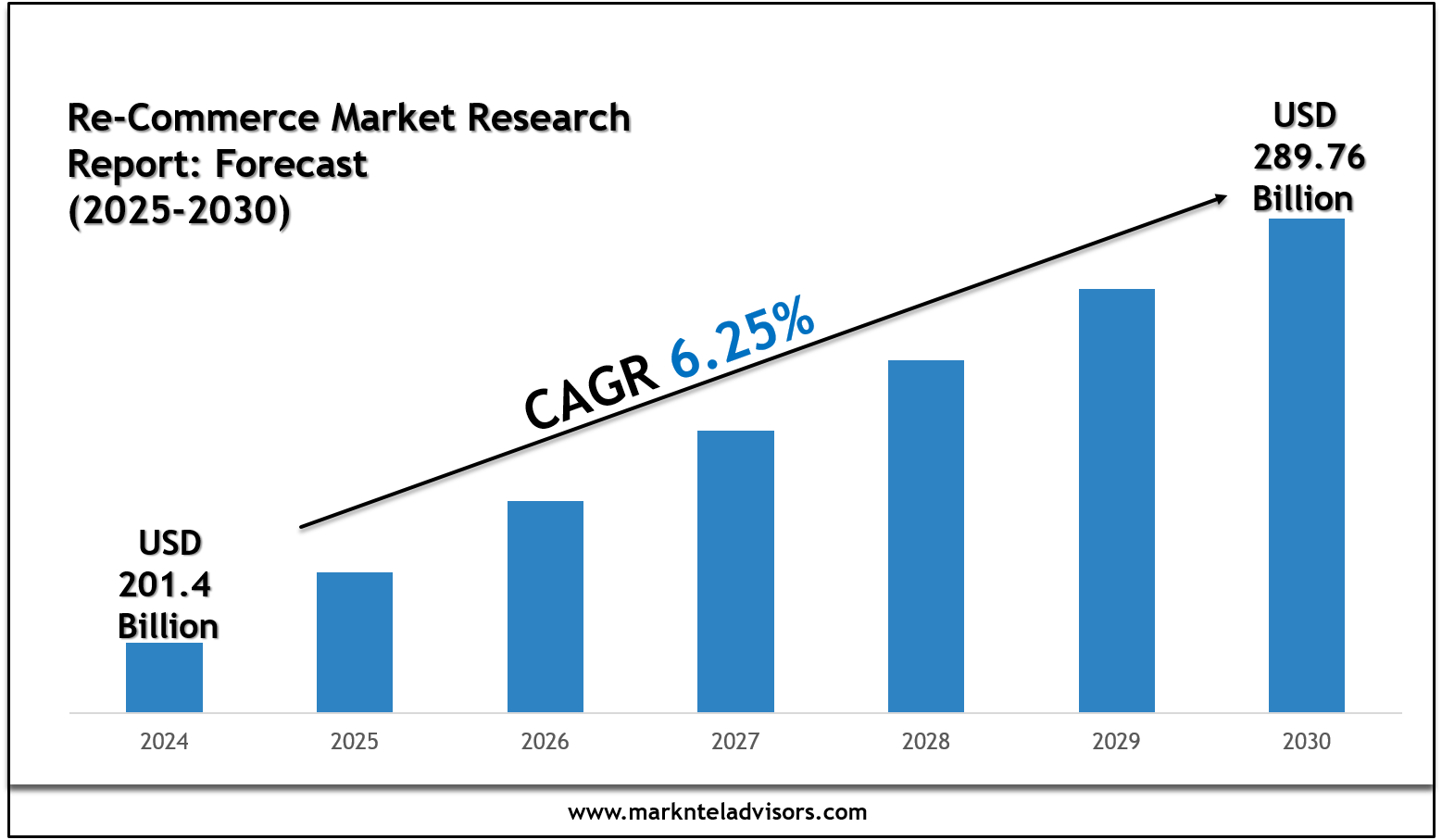

Re-Commerce Market Overview- The Re-Commerce market is witnessing steady expansion, driven by technological advancements, changing consumer demands, and global economic shifts. Market research plays a vital role in helping businesses navigate this growth by offering data-driven insights and forecasts. This report presents a comprehensive analysis of the market’s size, structure,...

1xBet Promo Code 2026: 1X200MAX | Bonus up to €130 The active 1xbet promo code 2026 for 1xBet 2026 is 1X200MAX, which unlocks a 100% welcome bonus up to $130. Such codes are valid only at the moment of signing up. Use it to score a 130% sports bonus up to €130 (or your local currency) on your first deposit. If slots and table games are more your vibe, this code unlocks a whopping...

Parlay Bola Online is a football betting system where multiple match predictions are combined into a single betting ticket. Instead of betting on only one match, players select two or more football outcomes and link them together into one parlay. All selections must be correct for the parlay to win. Because the odds are multiplied, Parlay Bola Online offers much higher potential payouts than...

E-commerce is transforming rapidly, and customer expectations are higher than ever. Today’s buyers demand speed, convenience, personalization, and seamless shopping experiences across all devices. For modern brands, simply launching an online store is no longer enough. The future of ecommerce belongs to businesses that combine advanced technology, high-performance development, smart...

The popularity of online sports betting and gaming platforms has grown rapidly, and Mahadev Book has emerged as one of the most trusted names in this space. Whether you are interested in cricket betting, live casino games, or other online markets, having a Mahadev Book ID is the first step. Once your ID is created, the next important process is logging in correctly and...