A Strategic Analysis of Modern Mortgage Structures and Market Accessibility

The landscape of residential finance has undergone a significant transformation, shifting from the rigid requirements of previous decades to a more nuanced, data-driven approach. When examining the current housing market, many prospective investors first evaluate how much of a down payment do i need for a house to determine their actual purchasing power. This initial capital requirement serves as the primary barrier to entry, but analytical trends show that the average contribution has decreased as lenders find new ways to mitigate risk through advanced scoring models and insurance products. This evolution has made it possible for a broader demographic to transition from wealth-consuming rent to wealth-building equity.

Comparative Analysis of Lending Frameworks

To understand the mechanics of today’s market, one must look at the structural difference between fha and conventional loans and how they impact the borrower's long-term net worth. Government-insured programs are designed to promote liquidity in the market by allowing higher debt-to-income ratios and lower credit scores. Conversely, the private market focuses on rewarding borrowers who demonstrate lower risk with more favorable interest rates and the eventual removal of secondary costs. An analytical approach suggests that while the government route is more accessible initially, the private route often proves more cost-effective over a thirty-year horizon due to more flexible insurance policies.

The Economics of Initial Capital Contributions

Choosing a conventional loan down payment is no longer a binary choice between zero and twenty percent. Data indicates that a significant portion of first-time buyers now opt for a three-to-five percent range, allowing them to enter the market earlier and benefit from property appreciation. While this strategy involves the added expense of private mortgage insurance, the rate of home value growth in many regions often outpaces the cost of that insurance. This trade-off represents a strategic shift where buyers prioritize market timing over the traditional goal of avoiding monthly premiums through a large upfront investment.

The Quantitative Review: Behind the Scenes of Risk Assessment

Once a contract is in place, the file enters a specialized phase of technical verification. To grasp the complexity of this stage, it is necessary to explore what is underwriting in the context of institutional risk management. This process is essentially a comprehensive audit where a professional actuary ensures the loan meets specific secondary market guidelines. By verifying the accuracy of the borrower's financial disclosures and the validity of the property appraisal, the lender ensures that the asset is sufficient to cover the debt in the event of a default, maintaining the overall stability of the financial system.

Core Data Points in the Risk Evaluation Model

-

The Loan-to-Value (LTV) ratio, which measures the amount of debt against the appraised value of the property.

-

Liquid asset reserves, ensuring the buyer has enough capital to handle the first few months of ownership costs.

-

Credit utilization patterns, which serve as a proxy for the borrower's overall financial discipline and reliability.

-

The Debt-to-Income (DTI) ratio, establishing a ceiling for how much of a person's gross earnings can be committed to housing.

Structural Differences at a Glance

A data-driven comparison of the two primary lending paths highlights the specific trade-offs involved in mortgage selection. These variables directly influence the total cost of borrowing over time.

|

Economic Metric |

Standard Private Funding |

Publicly Insured Funding |

|

Initial Liquidity Required |

Typically 3% to 20% of price |

Fixed at 3.5% of price |

|

Long-term Insurance Cost |

Ends when equity reaches 20% |

Usually remains for the loan life |

|

Interest Rate Sensitivity |

Highly dependent on credit score |

Generally more stable across scores |

|

Property Standards |

Focus on market value |

Focus on health and safety codes |

Optimizing the Financial Profile for Approval

The success of a mortgage application relies on the presentation of a stable and predictable financial history. From an analytical perspective, lenders are looking for anomalies in cash flow. Avoiding large, unverified deposits or the opening of new credit lines is essential during the active review period. Those who maintain a high level of transparency and keep their financial profile "clean" are statistically more likely to close on time. Furthermore, understanding the impact of interest rates on monthly cash flow allows buyers to decide if they should pay points upfront to lower their long-term interest expense, a move that often pays for itself within five to seven years.

Strategic Preparation Checklist

-

Auditing credit reports at least six months prior to purchase to correct any inaccuracies.

-

Aggregating all sources of income, including bonuses and dividends, to maximize the qualifying income.

-

Identifying potential closing cost credits that can be negotiated with the seller to preserve personal cash.

-

Maintaining a consistent employment record to satisfy the two-year stability requirement typical of most lenders.

Analyzing the mortgage process through a technical and financial lens removes the mystery from the transaction. By focusing on the math behind the requirements and the risk models used by banks, buyers can make decisions that align with their broader financial goals. Whether the objective is to minimize the initial cash outlay or to secure the lowest possible monthly payment, a deep understanding of the mechanics of lending is the most valuable asset a homebuyer can possess in a competitive market.

The culmination of a real estate transaction is the result of months of preparation and a thorough understanding of financial tools. As the industry continues to leverage technology for faster reviews and more precise risk modeling, the borrower who remains educated and proactive will always have the advantage. By viewing the mortgage as a strategic financial instrument rather than just a debt, you can navigate the path to homeownership with a clear and focused vision for the future.

Категории

Больше

When you think of jewelry that lasts forever, you probably think of gold or diamonds. But there is another stone that people have loved for thousands of years—Jade. It is not just a stone; it is a symbol of luck, health, and protection. If you are looking for something beautiful to wear around your neck, a Jade Pendant is a perfect choice. It feels smooth against your skin, looks elegant...

Introduction Spain has become one of Europe’s premier golfing destinations, attracting players from around the world with its warm climate, stunning landscapes, and exceptional golf facilities. Among the country’s top attractions is the largest golf complex in Spain, a destination that combines luxury, sport, relaxation, and entertainment in one incredible setting....

Executive Summary Arch Liner Market : The arch liner market is expected to witness market growth at a rate of 5.20% in the forecast period of 2021 to 2028 and is further estimated to reach USD 3,717.5 million by 2028. Today’s cut-throat era calls for businesses to be equipped with knowhow of the major happenings of the relevant market and industry. To acquire knowhow of...

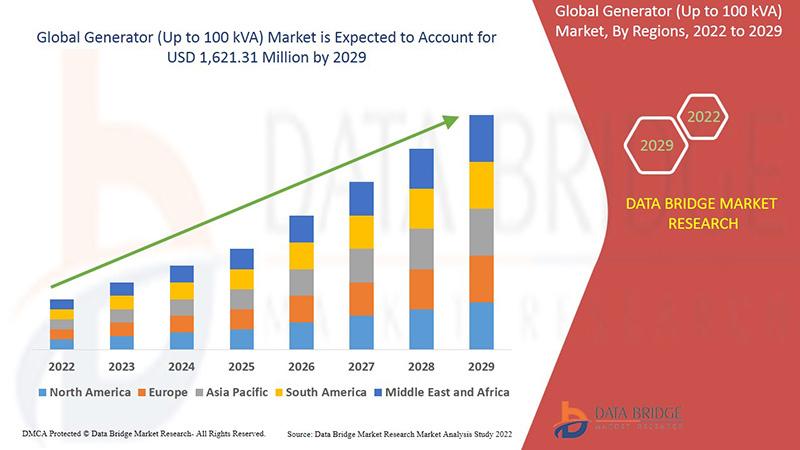

"Executive Summary Generator (Up to 100 kVA) Market Market Size and Share Analysis Report Data Bridge Market Research analyses that the generator (up to 100 kVA) market will witness a CAGR of 3.40% for the forecast period of 2022-2029. the Generator (Up to 100 kVA) Market Market analysis report, the strength and weakness of the competitors can be assessed. The dimensions of the...

"Executive Summary Coronary Intravascular Lithotripsy (IVL) Market Size and Share Analysis Report CAGR Value The global coronary intravascular lithotripsy (IVL) market size was valued at USD 277.94 million in 2024 and is expected to reach USD 493.50 million by 2032, at a CAGR of 7.44% during the forecast period Accomplishment of maximum return on...