Water Tanker Truck Market Size, Share and CAGR Insights Report 2025–2034

Market Overview

The water tanker truck market is witnessing steady growth due to increasing demand for potable water transportation, industrial water supply, and emergency water distribution systems. Rising water scarcity in urban and rural regions is significantly driving adoption of tanker-based water logistics solutions across global markets.

Market Size

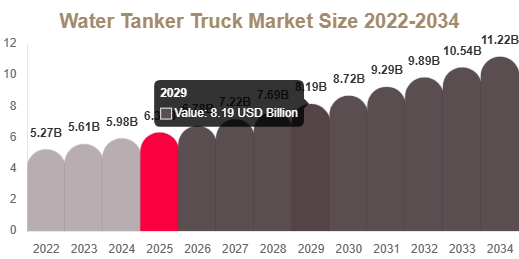

The global water tanker truck market size was valued at USD 7.86 billion in 2025 and is projected to reach USD 8.24 billion in 2026. By 2034, the market is expected to reach USD 13.92 billion, growing at a CAGR of 6.7% from 2025 to 2034.

Get Your Sample Report Here: https://www.redlinepulse.com/report/water-tanker-truck-market/request-sample

Buy Now: https://www.redlinepulse.com/report/water-tanker-truck-market

Market Trends

Growing Adoption of Smart Water Distribution Systems

A key trend in the water tanker truck market is the integration of smart monitoring systems for tracking water flow, tank levels, and route optimization. These technologies improve operational efficiency and ensure timely water delivery in municipal and industrial applications.

Increasing Use in Construction and Mining Operations

Construction and mining industries are increasingly using water tanker trucks for dust suppression, site cleaning, and material processing. Growing infrastructure development projects worldwide are further accelerating demand for these vehicles.

Market Drivers

Rising Water Scarcity and Distribution Needs

One of the primary drivers of the water tanker truck market is increasing global water scarcity. Municipalities and private operators rely on tanker trucks to supply water to regions lacking proper pipeline infrastructure.

Expansion of Construction and Infrastructure Projects

Rapid urbanization and large-scale infrastructure development are boosting demand for water tanker trucks. These vehicles are essential for construction site operations, road building, and industrial development activities.

Market Restraint

High Operational and Maintenance Costs

Water tanker trucks require regular maintenance of pumps, storage tanks, and chassis systems. Rising fuel costs and maintenance expenses can limit adoption among small fleet operators and municipalities.

Market Opportunities

Expansion of Municipal Water Supply Programs

Government initiatives to improve rural and urban water distribution are creating strong opportunities for water tanker truck manufacturers. These programs aim to ensure reliable water access in underserved regions.

Growth in Industrial Water Logistics Demand

Industries such as power generation, oil & gas, and manufacturing are increasing their reliance on tanker trucks for process water supply and emergency storage solutions.

Segmental Analysis

By Tank Type

According to Redline Pulse, stainless steel water tanker trucks dominated the market with a 46.18% share in 2025 due to durability and hygiene benefits. Aluminum and carbon steel tankers are also widely used based on cost and application requirements.

By Application

Municipal water supply dominated with a 39.72% share in 2025 due to high demand for drinking water distribution. Industrial applications are expected to grow rapidly due to increasing infrastructure and manufacturing activities.

By Capacity

Medium capacity tanker trucks (5,000–10,000 liters) held the largest share of 42.36% in 2025 due to balanced efficiency and operational flexibility. Large capacity trucks are gaining traction in industrial and mining sectors.

By End Use

Municipal corporations remained the dominant end-use segment in 2025. Construction and mining companies represent the fastest-growing segment due to rising infrastructure expansion.

Regional Analysis

North America

North America accounted for 31.28% of the market in 2025, driven by strong municipal infrastructure and emergency water supply systems, especially in the United States.

Europe

Europe held 25.14% share in 2025 due to strict environmental regulations and structured water distribution networks. Germany leads the region in tanker truck adoption.

Asia Pacific

Asia Pacific accounted for 27.66% share in 2025 and is expected to grow at the fastest CAGR of 7.3% due to rapid urbanization, water scarcity, and infrastructure development led by China and India.

Middle East & Africa

The region held 9.42% share in 2025 due to extreme climate conditions and high dependency on tanker-based water distribution, with UAE and Saudi Arabia leading demand.

Latin America

Latin America accounted for 6.50% share in 2025 with Brazil dominating due to expanding urban infrastructure and agricultural water supply needs.

Competitive Landscape

The water tanker truck market is moderately fragmented with several global and regional manufacturers competing on tank design, fuel efficiency, and durability. Companies are increasingly focusing on lightweight materials and improved pumping systems to enhance operational efficiency.

Key Players Analysis

1. Tata Motors – Strong presence in commercial vehicle segment with reliable tanker truck solutions for municipal and industrial use.

2. Ashok Leyland – Offers durable water tanker trucks widely used in infrastructure and construction projects.

3. Volvo Group – Focuses on advanced heavy-duty tanker platforms with high efficiency and safety features.

4. Daimler Truck AG – Provides robust tanker chassis solutions for global water logistics operations.

5. MAN Truck & Bus – Known for fuel-efficient heavy-duty trucks used in municipal water transport.

6. Isuzu Motors – Strong player in medium-duty tanker trucks for urban and rural applications.

7. Hino Motors – Offers reliable tanker truck platforms for industrial and municipal distribution.

8. FAW Group – Major manufacturer in Asia with expanding presence in commercial tanker trucks.

9. Dongfeng Motor Corporation – Provides cost-effective tanker truck solutions for developing markets.

10. Volvo Eicher Commercial Vehicles – Focuses on regional tanker truck demand with strong service network.

Categories

Read More

Some stories are not written to impress, entertain, or escape reality. Some are written because silence has become unbearable. Tightrope by Sandra Lee Taylor belongs to that rare category of books that exist not to decorate a bookshelf, but to testify. It is a powerful trauma recovery memoir that transforms a life shaped by fear, violence, and emotional neglect into a story...

ORDER NOW: https://healthyifyshop.com/GetClairuAirPurifier The Clairu Air Purifier stands out as a practical solution for cleaner indoor air. With its modern design, efficient filtration, and user-friendly features, it’s a great addition to any home or workspace.FOR MORE...

Bio based resins are environmentally friendly polymer materials derived from renewable biological resources such as corn starch, sugarcane, vegetable oils, cellulose, and other plant based feedstocks. These resins are increasingly used across packaging, automotive, construction, consumer goods, textiles, and electronics industries due to their reduced environmental impact and growing demand for...

In a significant turn of events, the annual observance of International VPN Day on August 19 comes at a critical juncture for digital privacy in the United Kingdom. This day, dedicated to highlighting virtual private networks' importance for online security and freedom, arrives amid unprecedented challenges to VPN accessibility in one of the world's leading democracies. The conversation around...

Rising demand for healthy diets and home-prepared beverages is expected to fuel the global blender sector over the coming years. Consumers prefer appliances that offer speed, versatility, and smart features, making blenders a staple in modern kitchens. The Blenders Market is projected to expand according to the Blenders Market Forecast report. Evolving consumer preferences, product innovations,...