Common Hurdles and Clear Answers: Is This Loan Path Right for You?

When you start digging into the world of real estate, you likely have a thousand questions spinning in your head. Is now the right time to buy? Can I afford the monthly costs? One of the most frequent points of confusion centers around the mortgage insurance premium and why it exists. Many people wonder if it is a penalty for not having a large down payment. In reality, it is a gateway. This fee protects the lender, which in turn allows them to offer you a loan with as little as 3.5% down. Without this insurance, many buyers would be stuck saving for decades while home prices continue to climb out of reach.

As you research your options, you will undoubtedly come across specific government programs. A very common question for beginners is what does fha stand for in the context of my mortgage? The acronym refers to the Federal Housing Administration. This agency was created during the Great Depression to help stabilize the housing market. Today, it serves as one of the most popular paths for people who want to stop paying rent and start building equity. It acts as a safety net that makes homeownership a possibility for the average worker rather than a luxury reserved for the wealthy.

Comparing Your Financing Paths

To help you visualize how different loans stack up, it is helpful to look at the numbers side-by-side. Choosing the right vehicle for your purchase depends heavily on your current savings and your long-term plans for the property.

|

Feature |

Government-Backed Loan |

Conventional Loan |

|

Minimum Down Payment |

3.5% |

3% to 20% |

|

Credit Score Flex |

High (Accepts lower scores) |

Moderate to Low |

|

Insurance Requirement |

Always Required |

Only if under 20% down |

|

Appraisal Rules |

Stricter Safety Standards |

Standard Market Value |

What If the House Needs Work?

One question that often stops buyers in their tracks is: "What if the perfect house is a mess?" If you find a home that has structural issues or needs a complete kitchen overhaul, you might think you need a separate construction loan. This is where the 203k fha loan enters the conversation. This program is specifically designed to answer the question of how to fund both a purchase and a renovation simultaneously. It allows you to wrap the repair costs into your primary mortgage, based on the value the home will have after the work is completed.

Key Benefits of Renovation Financing:

-

Consolidates all debt into a single monthly payment with one interest rate.

-

Allows for modernizing older homes in established, desirable neighborhoods.

-

Increases immediate equity by improving the property right away.

-

Covers a wide range of repairs, from plumbing and roofing to energy-efficient upgrades.

Another major concern for many applicants is their past financial history. You might be asking yourself if a few missed payments or a low score will disqualify you completely. The reality is that qualifying for an fha loan bad credit is much more common than the big banks might lead you to believe. Because the government is insuring the loan, lenders are willing to look at "compensating factors." This means if you have a solid job and enough cash in the bank to cover a few months of payments, they can often overlook a score that is lower than the industry standard.

Common Eligibility Questions Answered:

-

Do I need a 700 credit score? No, many lenders accept scores as low as 580 for a 3.5% down payment.

-

Can I use a gift for my down payment? Yes, the program allows family members or employers to provide the down payment as a gift.

-

Are there income limits? Generally, no. As long as you can prove you can afford the monthly debt, there is no "ceiling" on what you can earn.

-

Is there a limit on how much I can borrow? Yes, there are "loan limits" that vary by county based on local housing costs.

The Long-Term Perspective

Once you get past the initial questions of "Can I?" and "How?", you have to look at the "Should I?" aspect. Buying a home is a marathon, not a sprint. While the upfront costs and the ongoing insurance premiums are important, you should also consider the cost of waiting. If home prices are rising at 5% a year, waiting two years to save a bigger down payment might actually cost you more than the insurance premiums ever would. You are essentially paying for the "locked-in" price of today's market.

Furthermore, consider the stability of your housing costs. When you rent, you are at the mercy of a landlord who can raise the price every time your lease is up. When you own, your principal and interest remain the same for the life of the loan. This predictability is a huge financial advantage as your income grows over time while your housing cost stays the same. It is the ultimate hedge against inflation.

Important Factors for Your Decision:

-

Assess your current debt-to-income ratio to see what you can comfortably afford.

-

Determine how long you plan to stay in the home; insurance costs are more manageable over a 5-10 year window.

-

Look at your local rental market—is owning cheaper than or equal to current rent prices?

-

Check for local first-time buyer grants that can be combined with these programs to further lower your costs.

Closing Thoughts on Making the Move

Asking the right questions is the first step toward a successful home purchase. By understanding how insurance protects your ability to borrow and how specific renovation programs can expand your search, you put yourself in a position of power. Don't be afraid to speak with multiple lenders to get different perspectives on your specific situation. Every buyer's journey is unique, and the programs available today are designed to be flexible enough to meet a wide variety of needs and financial backgrounds. With the right information, the path to homeownership becomes much clearer and less intimidating.

The goal is to stop asking "if" you can buy a home and start asking "when." By utilizing the tools and programs specifically created for your situation, you can turn a complex financial process into a series of manageable steps. Your future self will likely thank you for having the courage to navigate these questions today so you can enjoy the security of your own home tomorrow.

Категории

Больше

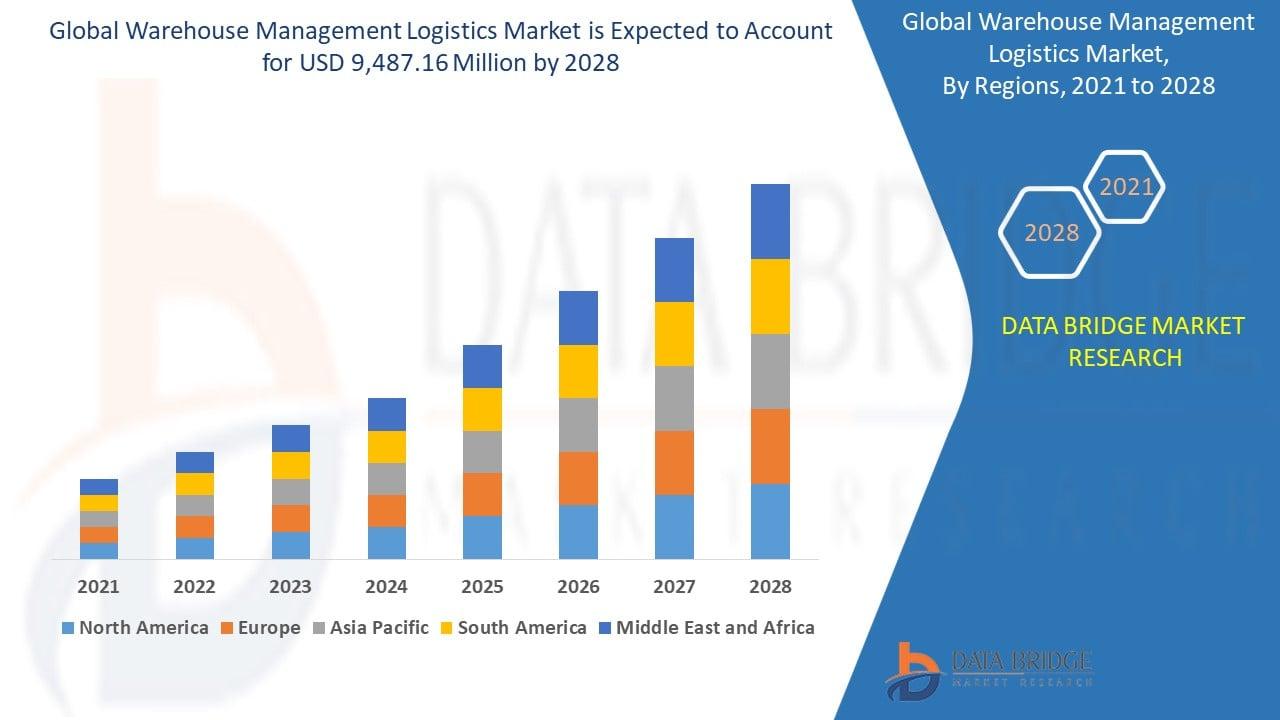

"Warehouse Management Logistics Market Summary: According to the latest report published by Data Bridge Market Research, the Warehouse Management Logistics Market The global warehouse management logistics market size was valued at USD 5.21 billion in 2024 and is projected to reach USD 17.30 billion by 2032, with a CAGR of 16.20% during the forecast period of 2025 to 2032 For an...

The Yeezy Gap line brings a fresh mix of comfort and street feel to daily wear. It focuses on soft fabrics that give you ease while you move through your day. Many people choose the pieces because they match with almost anything in a wardrobe. The brand keeps its look simple, which helps users enjoy clothing that works in many settings. Your website offers these items in clean shades that pair...

The global fuel cell vehicle market is witnessing significant growth as governments, automotive manufacturers, and energy companies focus on reducing carbon emissions and promoting sustainable transportation solutions. Fuel cell vehicles operate using hydrogen fuel cells that generate electricity through a chemical reaction between hydrogen and oxygen, producing only...

Finding the right mortgage doesn't have to be a source of constant stress if you approach the market with a solid strategy. Most successful buyers find that the many types of conventional loans available provide a perfect balance of interest rates and long-term stability. Unlike government-backed schemes, these private sector loans often reward borrowers who have spent time polishing...

Easy and Trusted NetApp NS0-005 Exam Prep for Fast Results Many students feel confused before NetApp NS0-005 exams. They study many books but still feel unsure. This wastes time and energy. Good NetApp Technology Solutions Professional certification exam preparation material helps fix this problem in a simple way. It keeps your study clear and focused from day one. You...