Key Strategies for Thriving in the Contemporary Housing Market

Entering the world of real estate can feel like a daunting task, but having a few tricks up your sleeve can make the journey much smoother. One of the most effective ways to start is by researching the current fha loan limits in the specific county where you hope to live. These figures represent the maximum amount the government is willing to insure for a mortgage, and they can vary wildly from one city to the next. Knowing these numbers helps you filter your search effectively, ensuring that you are only looking at homes that fit within the parameters of your chosen financing. It is all about being prepared before you even step foot in an open house.

Building a Strong Financial Foundation

If you are worried that your past financial decisions might haunt your future, you are not alone. Many potential buyers feel stuck in the rental cycle because they believe their history is a permanent barrier. However, seeking out bad credit home loans is a fantastic way to break through that wall. These programs are designed to look at your current stability rather than just focusing on old mistakes. By demonstrating a steady income and a commitment to your current bills, you can prove to lenders that you are ready for the responsibility of a mortgage. It is a vital tip for anyone who needs a fresh start in the housing world.

Another great strategy is to keep your debt-to-income ratio as low as possible before you apply. Even if your credit score isn't perfect, showing that you don't have a lot of outstanding balances can make you a much more attractive candidate. Lenders love to see that you have plenty of room in your monthly budget to handle a new house payment. Combining this with a modest savings account for unexpected repairs will give you a significant advantage when it is time to sit down with a loan officer and discuss your options.

Transforming a Diamond in the Rough

In a market where inventory is low, you might find that the only affordable homes are the ones that need some serious work. Instead of being discouraged by a dated kitchen or a leaky roof, consider using a 203k loan to your advantage. This tip is a game-changer for buyers who have a vision for what a house could be. By rolling the costs of renovations into your primary mortgage, you save yourself from the headache of trying to fund repairs with high-interest personal loans or credit cards later on. It allows you to buy the worst house on the best block and turn it into a high-value asset.

When you use this type of renovation financing, you also have the benefit of knowing the work is being done by licensed professionals. The program requires detailed bids and inspections, which protects you from shoddy workmanship. This ensures that the money you are borrowing is actually increasing the value and safety of your new home. It is a smart way to bypass the bidding wars often found with move-in-ready homes and instead create a custom living space that fits your exact needs and aesthetic preferences.

Accessibility Regardless of Your Score

Many people are surprised to learn how accessible homeownership can be, even with a history of financial struggles. Successfully applying for an fha loan bad credit involves understanding that the government provides a safety net for the lender. Because the loan is insured, the bank is much more willing to work with you even if you don't have a 700 credit score. The most important tip here is to be completely transparent with your lender from the beginning. They can help you identify exactly what you need to do—whether that is paying down a specific collection account or saving a little more for a down payment—to get your application over the finish line.

If your score is on the lower end, you might be asked to provide more documentation, such as proof of consistent rent payments or utility bills. This is known as non-traditional credit, and it is a powerful tool for proving your reliability. Keeping a clean record of these payments for twelve months can often be the deciding factor in an approval. Don't let a low score stop you from asking the question; you might find that the door is much wider than you originally thought.

Long-Term Planning and Patience

The best tip for any homebuyer is to remember that this is a long-term investment. While it is easy to get caught up in the excitement of a new kitchen or a big backyard, the financial structure of your loan is what will impact your life for the next thirty years. Take the time to compare different lenders and their fees, as even a small difference in an interest rate can save you a fortune over time. Being patient and waiting for the right house that fits both your lifestyle and your budget will lead to a much happier homeownership experience.

Finally, always keep an eye on the future. As you build equity in your home, you may eventually be able to refinance into a conventional loan once your credit score has improved or the home's value has increased. This can help you remove the mortgage insurance premiums and lower your monthly payment even further. By starting with the right government-backed program today, you are setting the stage for a lifetime of financial growth and security. Homeownership is a journey, and with these tips, you are well on your way to reaching your destination.

Remember that the professionals you work with—your real estate agent and your loan officer—are there to help you. Ask plenty of questions and don't be afraid to voice your concerns. The more informed you are, the better decisions you will make. Whether you are dealing with a fixer-upper or a low credit score, there is a path forward. Stay focused on your goals, keep your finances organized, and soon you will be holding the keys to your very own home.

Categories

Read More

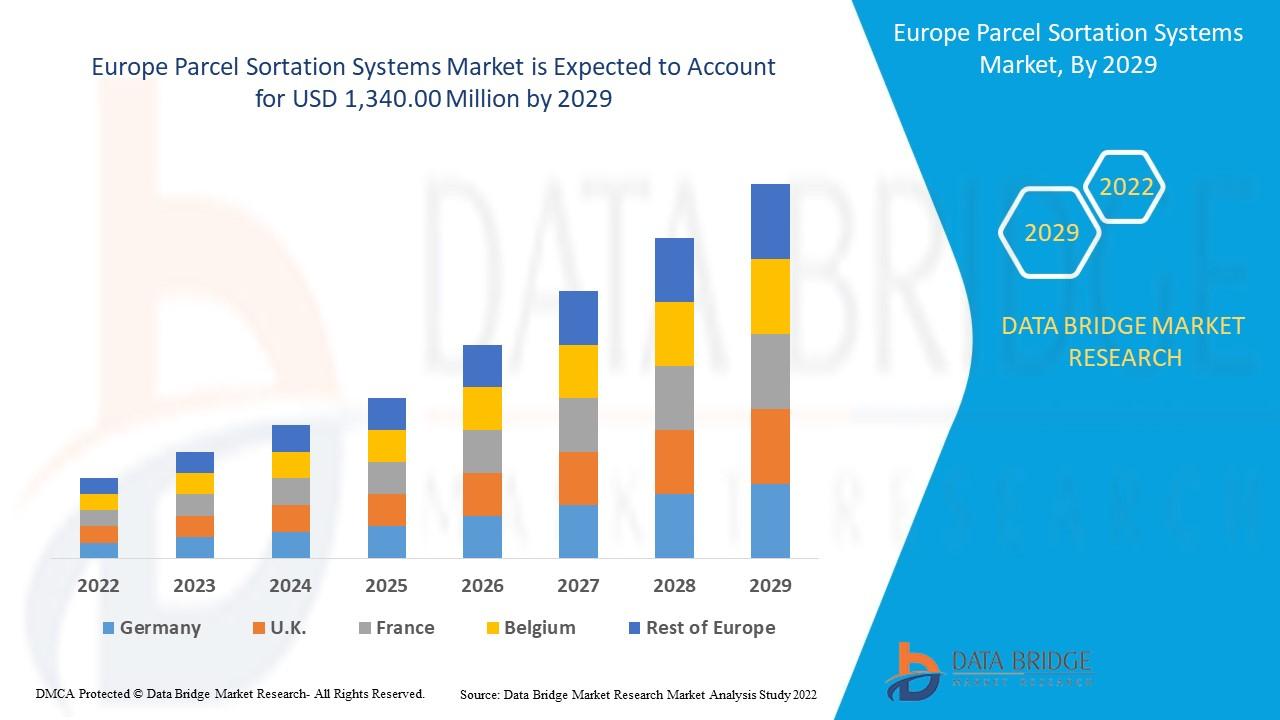

Regional Overview of Executive Summary Europe Parcel Sortation Systems Market by Size and Share CAGR Value Data Bridge Market Research analyses that the market is growing with the CAGR of 13.5% in the forecast period of 2022 to 2029 and is expected to reach USD 1,340.00 million by 2029. It is the necessity of this rapidly changing marketplace to adopt such Europe Parcel Sortation...

This Healthcare Cold Chain Logistics market report has been prepared by considering several fragments of the present market and upcoming market scenario. The insights gained through this market research analysis facilitate a clearer understanding of the market landscape, issues that may interrupt in the future, and ways to position a brand effectively. It consists of highly detailed...

If you are looking for an effective, non-surgical way to lose weight, the Allurion Balloon has become one of the most popular medical weight-loss treatments available in Melbourne. Designed to help patients reduce appetite, control portion sizes, and develop healthier eating habits, the Allurion Balloon offers a convenient alternative to traditional gastric balloons and weight-loss surgery....

Neue Set-Vorstellung Das kommende Set B1a „Feuerrote Flammen“ bringt eine aufregende Erweiterung für das Pokémon-Sammelkartenspiel Pocket mit sich. Besonders im Mittelpunkt stehen die mächtigen Mega-Pokémon-EX, die in der neuen Edition ihre beeindruckende Rückkehr feiern. Am 17. Dezember 2025 wird das Boosterpack veröffentlicht und bietet Spielern...

Surgery represents a significant event for the human body, regardless of whether it is cosmetic, medical, or corrective. While most people focus heavily on the procedure itself, the true success of any surgery is determined not in the operating theatre but in the weeks and months that follow. At Laura’s Touch, post-op massage is regarded as an essential part of recovery, not an...