From Design to Dashboard: Automotive AR & VR Market Set to Redefine Mobility Innovation

Automotive AR and VR Market Report

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-ar-and-vr-market/request-sample

Market Size

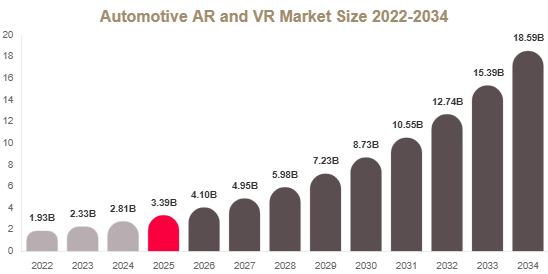

The global automotive AR and VR market size is estimated at USD 3.6 billion, increasing to USD 4.1 billion in 2026. By 2034, the market is projected to reach approximately USD 18.9 billion, growing at a CAGR of 20.8% during 2025–2034.

The automotive AR and VR market is expanding rapidly as vehicle manufacturers and technology providers integrate immersive technologies into design, manufacturing, training, and in-vehicle user experience systems.

Market Overview

The automotive AR and VR market is undergoing a rapid transformation with increasing adoption of immersive technologies across automotive design, production, training, and driver assistance systems. These technologies are reshaping how vehicles are engineered, tested, and experienced by end users.

Market Trends

Integration of AR head-up displays in modern vehicles

Automotive manufacturers are increasingly integrating AR-based head-up displays that project real-time navigation, speed, and safety alerts directly onto the windshield. This enhances driver awareness and improves road safety, especially in connected and semi-autonomous vehicles.

Expansion of VR-based design and training systems

VR technology is being widely used in automotive design simulation and workforce training. OEMs use virtual environments to test vehicle models before production, reducing costs and improving engineering accuracy. It is also used for assembly line training and service technician development.

Market Drivers

Rising digital transformation in automotive manufacturing

Automotive companies are adopting digital transformation strategies that integrate AR and VR into design, prototyping, and production workflows. This reduces reliance on physical prototypes and improves development efficiency through immersive 3D visualization tools.

Growth of autonomous and electric vehicles

The expansion of electric and autonomous vehicles is driving demand for advanced visualization systems. AR and VR help simulate driving environments, test autonomous algorithms, and improve human-machine interaction in next-generation mobility systems.

Market Restraints

High implementation cost and hardware limitations

The adoption of AR and VR technologies is limited by high costs of hardware systems, simulation platforms, and integration infrastructure. Technical limitations such as motion sickness in VR and field-of-view restrictions in AR also slow adoption.

Market Opportunities

Expansion of AR-based in-vehicle systems

Automotive OEMs are increasingly integrating AR into dashboards and windshield displays to enhance navigation and safety. These systems provide real-time contextual information, improving driver experience and situational awareness.

Growth of VR in automotive retail

VR-based virtual showrooms are transforming automotive sales by allowing customers to explore and customize vehicles digitally. This reduces showroom costs and enhances customer engagement, especially in urban markets.

Segmental Analysis

By Technology

Augmented Reality dominated the market in 2024 with approximately 58.2% share due to widespread use in head-up displays and driver assistance systems.

Virtual Reality is expected to grow at a CAGR of 21.5%, driven by increasing use in design simulation, prototyping, and workforce training.

By Application

Design and prototyping dominated the market in 2024 with approximately 32.7% share due to heavy use of VR simulation in vehicle development.

Driver assistance systems are expected to grow at a CAGR of 22.9%, driven by increasing AR-based safety visualization and smart cockpit integration.

By End Use

OEMs dominated the market in 2024 with approximately 61.9% share due to high investment in R&D and digital manufacturing tools.

Aftermarket and service providers are expected to grow at a CAGR of 20.4%, driven by VR-based training and AR diagnostic applications.

Regional Analysis

North America

North America accounted for approximately 36.4% of the automotive AR and VR market in 2025 and is expected to grow at a CAGR of 19.6%. The region benefits from strong technology infrastructure and early adoption of immersive automotive solutions.

Europe

Europe held around 27.8% share in 2025 and is projected to grow at a CAGR of 20.1%. Strong automotive engineering and digital innovation initiatives drive market growth.

Asia Pacific

Asia Pacific dominated the market with 28.9% share in 2025 and is expected to grow at a CAGR of 22.3%. Rapid EV adoption and automotive digitalization are key growth drivers.

Middle East & Africa

Middle East & Africa accounted for 3.5% share in 2025 and is expected to grow at a CAGR of 18.7%, driven by smart mobility and digital automotive training adoption.

Latin America

Latin America held 3.4% share in 2025 and is expected to grow at a CAGR of 19.2%, supported by increasing automotive digital transformation and VR-based sales adoption.

Competitive Landscape

The automotive AR and VR market is moderately consolidated with key players focusing on immersive simulation platforms, digital twin technologies, and AR/VR automotive integration solutions. Major companies include Microsoft Corporation, NVIDIA Corporation, Unity Technologies, Bosch, Siemens, and HTC Corporation.

Microsoft Corporation is a leading player, offering mixed reality platforms and cloud-based VR collaboration tools for automotive design and simulation workflows.

Key Players List

- Microsoft Corporation

- NVIDIA Corporation

- Unity Technologies

- HTC Corporation

- Siemens Digital Industries

- Robert Bosch GmbH

- PTC Inc.

- Qualcomm Technologies Inc.

- Visteon Corporation

- Panasonic Automotive Systems

- Harman International

- Continental AG

- Valeo SA

- Dassault Systèmes

- Fujitsu Limited

Nach Verein filtern

Read More

The landscape of industrial logistics is shifting rapidly as portability and flexibility become the new benchmarks for success. Mobile Tanks Market Growth is no longer just a trend; it is a structural evolution in how liquids and gases are handled across the globe. As companies move away from rigid, permanent storage infrastructure in favor of agile solutions, the demand for high-capacity,...

There’s an almost pleading line near the start of the Consensus Audit Guidelines draft that reveals how its authors hope to grab attention: address the reader as a CISO, CIO or IG and maybe they won’t look away.\n That tactic speaks to a bigger problem in information security: people often work harder to sidestep rules than to follow them. The CAG is an effort to make sensible...

Introduction In today’s design-driven world, businesses are no longer treating decor as an afterthought. From hotels and offices to retail stores and event companies, the way a space looks directly impacts how people feel, engage, and even spend. This is exactly why more businesses are shifting toward wholesale decorative item suppliers. It’s not just about buying in bulk. This is...

The indoor entertainment industry has seen significant growth in recent years, with trampoline parks emerging as one of the most popular attractions for families, fitness enthusiasts, and group activities. These parks offer a unique combination of fun, fitness, and social engagement, making them a highly attractive business opportunity. However, setting up a trampoline park is...

Creating a wellness space needs more than good design. It needs the right build and the right team. Choosing a skilled Steam Room Manufacturer helps you get better results from the start. Expert Design Gives Better Results A professional Steam Room Manufacturer knows how steam and heat work together. They plan the layout with care. This helps keep the heat even and the air...