An Analytical Look at Veteran Mortgage Utility in 2026

The landscape of the American housing market has undergone significant shifts over the last few years, making it more important than ever for service members to dissect the tools available to them. From an analytical perspective, the primary driver of success for a military homebuyer is the leverage provided by the federal government. To activate this leverage, the first order of business is securing the certificate of eligibility which serves as the foundational data point for lenders to assess risk. By providing this verification, the borrower moves from a high-risk category into a specialized tier where the government guarantees a portion of the debt, allowing for terms that are mathematically superior to most conventional financing options.

When we examine the cost-benefit ratio of these loans, the va funding fee emerges as a critical variable. While it represents an upfront administrative cost, its impact on the overall loan-to-value ratio is significant. In 2026, for a first-time user with no down payment, this fee is typically 2.15 percent. Analytically, the ability to roll this cost into the total loan balance allows the borrower to preserve liquid capital. For those who have reached a 10 percent disability rating, the removal of this fee entirely creates an immediate equity advantage that traditional buyers cannot replicate through market timing alone.

Deconstructing Market Access and Loan Volatility

One of the most profound changes in the modern mortgage environment is the removal of specific government-imposed caps on borrowing for those with their full entitlement intact. Historically, va home loan limits functioned as a ceiling that restricted veterans in competitive markets. In 2026, the baseline conforming limit for a single-unit property has risen to $832,750 in most counties, and even higher in designated high-cost areas. However, for a veteran with full entitlement, these numbers are no longer a hard limit on the loan amount itself; rather, they serve as a benchmark for how the government calculates its guarantee. This allows for a zero-down purchase at much higher price points, provided the borrower’s debt-to-income ratio remains within healthy parameters.

2026 Baseline Conforming Limits for Partial Entitlement

|

Property Type |

2026 Baseline Limit (Most Counties) |

|

One-Unit Property |

$832,750 |

|

Two-Unit Property |

$1,066,250 |

|

Three-Unit Property |

$1,288,800 |

|

Four-Unit Property |

$1,601,750 |

The Efficiency of Interest Rate Optimization

Equity management does not end at the closing table; it requires ongoing analysis of market fluctuations. If the Federal Reserve adjusts policies leading to a drop in interest rates, the va irrrl becomes the primary tool for rate optimization. This Interest Rate Reduction Refinance Loan is a streamline product designed to minimize the friction of refinancing. From a financial planning standpoint, the low funding fee of 0.5 percent for this specific loan type ensures that the "break-even" point—the time it takes for monthly savings to exceed the cost of the loan—is achieved much faster than with a standard cash-out refinance or a conventional loan modification.

-

The streamline refinance typically requires no new appraisal, insulating the borrower from local market dips.

-

Closing costs can often be wrapped into the new loan, maintaining cash reserves.

-

The program enforces a "net tangible benefit" rule, ensuring the refinance actually improves the borrower's position.

-

Seasoning requirements ensure at least 210 days have passed since the first payment of the original loan.

Risk Mitigation and Long-Term Stability

The stability of a veteran-backed mortgage is further enhanced by the appraisal process, which focuses on Minimum Property Requirements. While some view these as hurdles, an analytical view reveals them as a form of risk mitigation. By ensuring a home is structurally sound and safe before the purchase is finalized, the program protects the veteran from the high costs of immediate, unforeseen repairs. This layer of protection, combined with the lack of private mortgage insurance (PMI), significantly lowers the monthly carrying cost of the asset compared to an FHA or conventional loan with similar down payment levels.

Furthermore, the 2026 market has seen a stall in national house price growth at roughly 0 percent, according to major research firms. In a flat market, the absence of a down payment means a borrower is not tying up large sums of cash in an asset that isn't rapidly appreciating. Instead, that capital can be diverted toward diversified investments or high-yield savings accounts, where it may earn a higher return than the equity in a stagnant housing market. This makes the zero-down benefit a powerful tool for broader wealth management, rather than just a way to buy a house.

The Data-Driven Path to Homeownership

To maximize the utility of these benefits, a borrower must approach the process with a focus on data and documentation. Lenders in 2026 are increasingly using automated systems to pull service records, but the responsibility remains with the veteran to ensure their records are accurate and up to date. Whether you are navigating the initial administrative fees or calculating the potential savings of a future refinance, understanding the underlying mechanics is essential. The military housing benefit is not merely a loan; it is a sophisticated financial instrument designed to provide stability and wealth-building opportunities to those who have served.

By analyzing the interplay between loan caps, funding exemptions, and streamline refinancing, it becomes clear that the value of the program extends far beyond the day of purchase. It is a lifelong asset that can be used multiple times, adapted to changing economic climates, and leveraged to secure a family's financial future. As the real estate market continues to evolve, those who treat their mortgage with the same strategic discipline they applied in service will find themselves best positioned to thrive in any economic environment.

Categorías

Read More

"Power Connector Market Summary: According to the latest report published by Data Bridge Market Research, the Power Connector Market Data Bridge Market Research analyses that the power connector market was valued at USD 3.27 billion in 2021 and is expected to reach the value of USD 4.83 billion by 2029, at a CAGR of 5% during the forecast period.Power Connector Market report endows...

Stainless steel travel flasks are popular for their durability, temperature retention, and convenience. They are designed to provide a reliable way to carry beverages on the go while maintaining safety and quality. Daily Commuting and Work One of the primary applications of stainless steel travel flasks is for daily commuting. Many people use these flasks to carry coffee, tea, or water to...

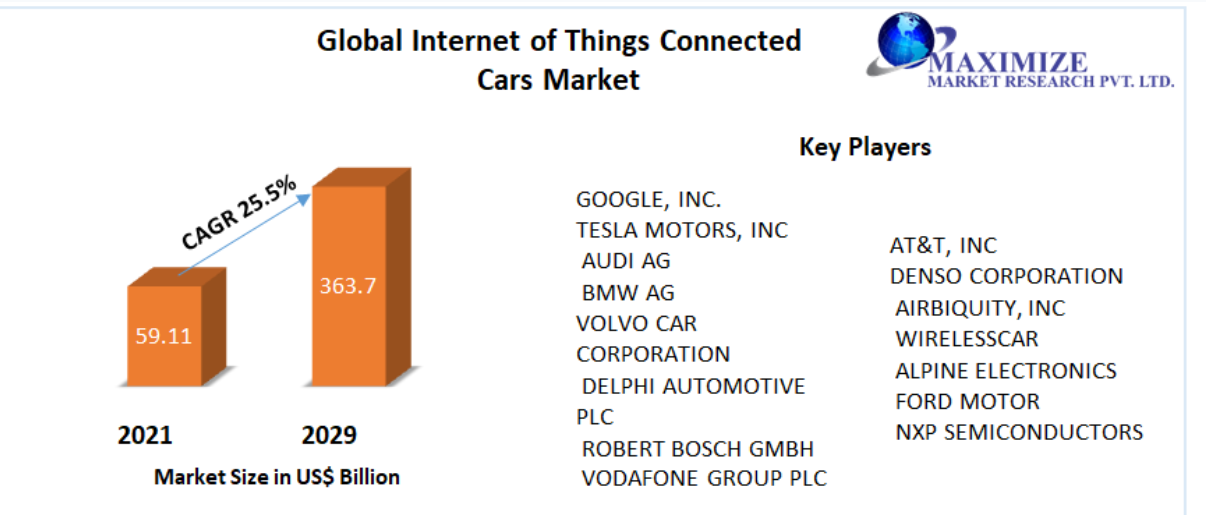

Internet of Things (IoT) Connected Cars Market is expected to grow at a CAGR of 25.5% during the forecast period. Global Internet of Things (IoT) Connected Cars Market is expected to reach US $ 363.7 Bn by 2029. Internet of Things (IoT) Connected Cars Market Overview: Maximize Market Research is a Business Consultancy Firm that has published a detailed analysis of the “Internet...

Die Suche nach einem kompetenten kfz gutachter münchen kann auf den ersten Blick schwierig erscheinen. Gerade in einer Großstadt wie München gibt es zahlreiche Anbieter, die ihre Dienstleistungen anbieten. Doch nicht jeder Gutachter arbeitet gleich professionell oder unabhängig. Deshalb ist es wichtig, bei der Auswahl einige entscheidende Kriterien zu beachten. Worauf...

Pakistan appears to be intensifying its efforts to control internet usage within its borders by blocking access to certain VPN services. Since late December, restrictions have been imposed on major VPN applications, notably affecting providers like Proton VPN, which confirmed their apps have been restricted since December 22. This move follows the country's decision to reintroduce VPN...