A Comprehensive Overview of Current Military Home Financing Benefits

Making an informed decision about where to live and how to pay for it is a cornerstone of financial health for service members and their families. The federal government provides a robust system to support this transition, offering terms that are often far superior to those found in the civilian sector. Understanding the mechanics of these benefits is essential for any veteran looking to plant roots in 2026. This system is designed to remove traditional barriers to entry, such as the need for a massive cash reserve for a down payment. To access these specialized tools, the process begins with the verification of your service history through a certificate of eligibility, which confirms your standing with the Department of Veterans Affairs and details your available entitlement.

The Financial Structure of the Transaction

While the program is widely celebrated for its zero-down payment feature, a truly informative look at the process must include the other financial components involved. Even without a down payment, there are standard costs associated with any real estate transfer. These va loan closing costs typically range between 3% and 5% of the total loan amount and cover a variety of professional services and government requirements. It is a common misconception that these are avoided entirely; rather, the program provides unique ways to manage them, such as allowing the seller to contribute toward these expenses or permitting certain fees to be paid by the lender via a credit.

Typical Closing Cost Components in 2026

|

Category |

Specific Items |

Estimated Range |

|

Lender Fees |

Origination, Credit Report, Underwriting |

Up to 1% of Loan |

|

Third-Party Services |

Appraisal, Title Search, Title Insurance |

$2,000 – $4,500 |

|

Prepaid Items |

Homeowners Insurance, Property Tax Escrow |

Varies by Location |

|

Government Fees |

Recording Fees, Transfer Taxes |

$500 – $2,000 |

Geographic Variables and Borrowing Capacity

In the current real estate climate, the amount you can borrow is heavily influenced by the local market conditions and your previous use of the benefit. For those who have full entitlement, the concept of a government-imposed "cap" has largely been phased out for primary residences. however, for those with remaining or partial entitlement, the 2026 va home loan limits serve as a vital guide for determining zero-down capacity. In most counties across the United States, the baseline limit for a single-family home is $832,750. In high-cost areas, such as major metropolitan hubs or coastal regions, this ceiling can reach as high as $1,249,125, reflecting the higher cost of living in those sectors.

Key facts regarding 2026 limits include:

-

The national baseline limit increased by approximately 3.26% over the previous year.

-

High-cost ceilings apply to over 100 counties with elevated median home prices.

-

Special statutory areas like Alaska and Hawaii feature even higher limits due to unique market factors.

-

Lenders still apply their own debt-to-income and credit standards regardless of the limit.

The Administrative Support Fee

To ensure the longevity of the lending program without relying solely on taxpayer funding, a specific administrative fee is applied to most loans. This is known as the va funding fee and it is a one-time charge calculated as a percentage of the loan amount. For a first-time user in 2026 choosing a zero-down payment, the standard rate is 2.15%. This percentage shifts if the buyer chooses to provide a down payment or if they have used the program in the past. Importantly, this fee can be rolled into the total loan balance, allowing the veteran to preserve their liquid cash for other needs during the move.

2026 Funding Fee Percentage Chart

|

Down Payment Amount |

First-Time Use |

Subsequent Use |

|

$0 Down (None) |

2.15% |

3.30% |

|

5% or More |

1.50% |

1.50% |

|

10% or More |

1.25% |

1.25% |

Exemptions and Protections

One of the most significant aspects of the program is the series of protections and exemptions offered to those with service-connected disabilities. In many cases, these individuals are not required to pay the administrative fee at all, which can represent a savings of tens of thousands of dollars over the life of the loan. Furthermore, the program mandates specific property inspections to ensure the home is safe, structurally sound, and sanitary. These "Minimum Property Requirements" act as a safeguard for the buyer, ensuring that the investment they are making is a sound one. By combining these federal protections with a clear understanding of the financial landscape, veterans can navigate the path to homeownership with a level of security that is unmatched in the broader mortgage market.

The military home financing system remains a powerful tool for building generational wealth and achieving stability. By staying informed about the shifting limits, understanding the breakdown of closing costs, and knowing how the funding fee applies to your specific situation, you can make strategic choices that benefit your family for years to come. The program is more than just a loan; it is a recognition of service that provides a tangible path to the American dream. Whether you are buying your first starter home or your forever home, these benefits are designed to support your journey every step of the way.

Categorias

Leia mais

Maintaining healthy blood circulation is important for overall wellness and daily comfort. Good circulation helps transport oxygen and nutrients throughout the body and supports healthy energy levels. However, modern lifestyles, long sitting hours, lack of physical activity, and stress may affect circulation and daily comfort. Many people experience tired legs, discomfort, low energy, or...

Key Drivers Impacting Executive Summary Sauces Market Size and Share CAGR Value The global Sauces market size was valued at USD 58.23 billion in 2024 and is expected to reach USD 89.37 billion by 2032, at a CAGR of 5.50% during the forecast period The large-scale Sauces Market report presents the best market and business solutions to Sauces Market...

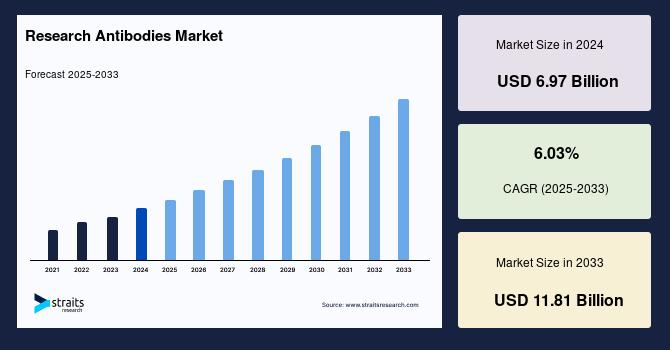

Research Antibodies Industry Insights: Straits Research recently introduced the latest update on the Research Antibodies Market that provides an extensive outlook of the market, analyzing key growth opportunities, challenges, risk factors, and emerging trends across diverse geographic regions. The report offers a definitive and meticulous analysis of the Research Antibodies...

Introduction For anyone who enjoys online poker, being able to access an account quickly and safely is very important. Players want a login process that is simple, reliable, and secure so they can spend less time dealing with technical problems and more time enjoying the game. This is one reason why many people search for Login IDN Poker88. The platform is widely used by poker players because...

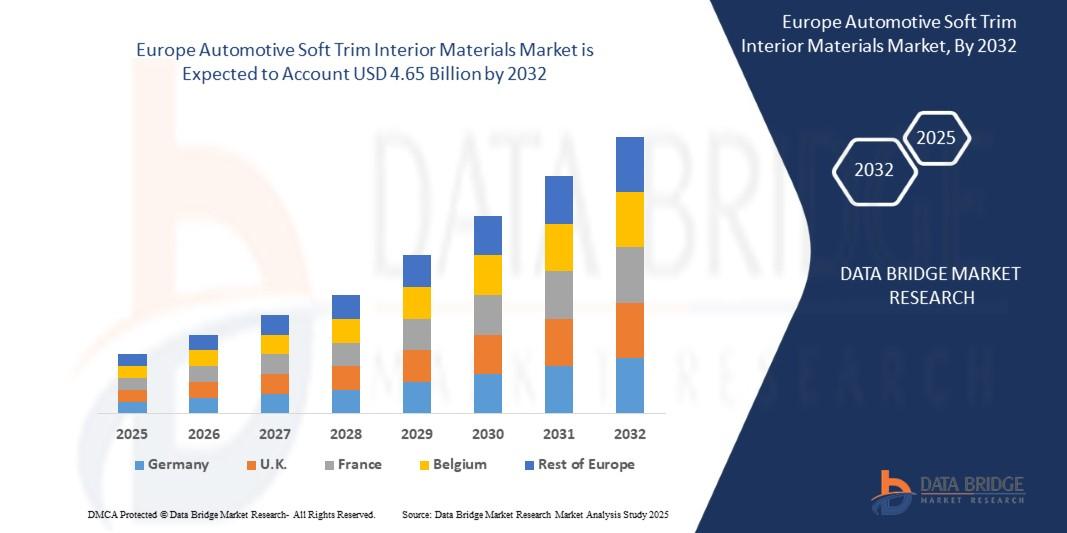

"Europe Automotive Soft Trim Interior Materials Market Summary: According to the latest report published by Data Bridge Market Research, the Europe Automotive Soft Trim Interior Materials Market The Europe Automotive Soft Trim Interior Materials Market size was valued at USD 3.22 billion in 2024 and is expected to reach USD 4.65 billion by 2032, at a CAGR of...