Ways to Approach the Modern Lending Landscape Confidently

The journey toward property ownership has shifted away from a one-size-fits-all model, especially for those who don't have a standard paycheck. Many self-employed individuals find that a 1099 loan provides the necessary leverage to secure a home without the traditional headache of providing years of complex tax filings. By focusing on your gross income rather than the net figures after deductions, these programs acknowledge your true purchasing power and offer a streamlined path to a successful closing.

Maximize Your Financial Profile for Quick Approval

Success in the alternative lending space often comes down to preparation and presenting a clear financial picture to your lender. Since you are stepping away from traditional documentation, the strength of your liquid assets and credit history takes on a more prominent role. Keeping your business and personal expenses clearly separated can help underwriters see a clean trail of income, making the approval process significantly smoother and faster.

-

Maintain a healthy reserve of cash to cover several months of mortgage payments.

-

Keep your credit utilization low in the months leading up to your application.

-

Ensure all your independent contracting agreements are documented and up to date.

-

Work with a loan officer who specializes in non-traditional income streams.

Focus on Debt Service for Investment Success

When you transition from buying a home to building a portfolio, the math shifts toward the performance of the asset. Lenders are particularly interested in how the property handles its own weight. Understanding the dscr loan down payment requirements is essential here, as most programs will ask for a 20% to 25% stake to ensure the loan stays in a safe risk bracket. This higher equity position often results in better interest rates and more favorable terms over the life of the loan.

Expand Your Horizons Beyond Conventional Constraints

The rigid guidelines of government-backed loans can be a major roadblock for entrepreneurs and seasoned investors alike. Choosing a non-qm mortgage allows you to bypass the strict debt-to-income ratios that often disqualify highly successful people. These products are designed to be flexible, looking at bank statements or asset depletion rather than just a W-2. It is a more holistic way to view wealth in a modern economy where income isn't always delivered in a tidy bi-weekly envelope.

Leveraging Asset-Based Lending

If you have significant savings or investment accounts but a lower monthly "income" on paper, asset-based lending can be a lifesaver. Lenders can calculate a monthly income figure based on the total value of your liquid assets. This is a common strategy for retirees or those who have recently sold a business and want to purchase property without returning to the workforce.

Smart Moves to Buy a Rental Property This Year

If your goal is to generate long-term wealth, the decision to buy rental property remains one of the most reliable strategies available. The key is to look for markets where the rent-to-price ratio makes sense. You want a property that not only covers its own mortgage and taxes but also leaves a bit of "mailbox money" at the end of every month. Doing your due diligence on the local job market and vacancy rates will ensure your investment stands the test of time.

Conducting a Thorough Market Analysis

Before pulling the trigger on a purchase, look at the historical growth of the neighborhood. Is there new infrastructure being built? Are big employers moving into the area? These are the indicators that point toward sustained demand. Financing is just one part of the equation; the physical real estate must be in a location that people actually want to live in for your strategy to truly pay off.

Managing Interest Rates and Fees Effectively

It is important to remember that specialized lending products often come with slightly higher interest rates than standard residential loans. This is the trade-off for the increased flexibility and decreased documentation requirements. However, you can often offset these costs by choosing a shorter loan term or by "buying down" the rate with points at closing. Always ask for a side-by-side comparison of different loan structures to see which one aligns best with your five-year or ten-year financial plan.

|

Strategy |

Primary Benefit |

Best For |

|

Rate Buy-Down |

Lower monthly payments |

Long-term hold investors |

|

Interest-Only Period |

Maximum monthly cash flow |

Short-term fix and flip or high-growth areas |

|

Adjustable Rate (ARM) |

Lower initial entry rate |

Borrowers planning to refinance or sell in 5-7 years |

Building a Team of Specialized Professionals

You shouldn't go through this process alone. A great real estate agent who understands investment properties, combined with a savvy mortgage broker, can make a world of difference. These professionals have seen the pitfalls and can guide you away from "money pits" or unfavorable loan terms. When everyone on your team is aligned with your specific goals, the path to closing becomes a collaborative effort rather than a stressful hurdle.

The Importance of a Pre-Approval Strategy

In a competitive market, having a pre-approval letter in hand is your most powerful tool. It shows sellers that you are a serious buyer with the backing of a lender. For specialized loans, this pre-approval carries even more weight because it proves that you have already cleared the hurdles of non-traditional income verification. It gives you the confidence to make firm offers and negotiate from a position of strength.

Evaluating Your Long-Term Portfolio Goals

As you move forward, keep an eye on the bigger picture. Every loan you take out should serve as a stepping stone to the next acquisition. By recycling your equity and using specialized financing tools, you can grow a small initial investment into a substantial real estate empire. The tools are available; it is simply a matter of applying them with discipline and a clear vision of your financial future.

Categorias

Leia Mais

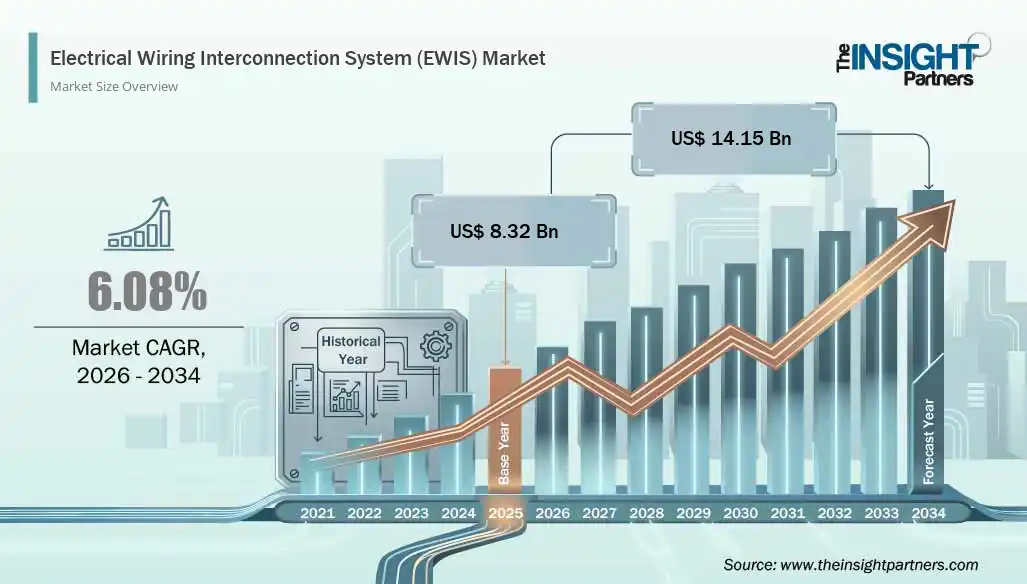

The global Electrical Wiring Interconnection System (EWIS) Market is projected to reach US$ 14.15 billion by 2034, rising from US$ 8.32 billion in 2025. The market is expected to expand at a CAGR of 6.08% during 2026–2034, supported by the increasing complexity of modern aircraft, rising demand for lightweight wiring solutions, and the need...

In today’s digital world, ranking on search engines is essential for businesses that want to attract customers online. With millions of websites competing for attention, search engine optimization (SEO) helps companies improve their visibility and reach the right audience. Working with a professional seo agency in usa allows businesses to improve search rankings, increase organic traffic,...

Warts can be frustrating, uncomfortable, and often affect confidence when they appear on visible areas of the skin. Warts Removal in Riyadh, Jeddah & Saudi Arabia focuses on safe, medically guided solutions designed to eliminate warts while protecting surrounding skin. At Royal Clinic Saudia, modern dermatology techniques are used to ensure precision, comfort, and long-term skin clarity for...

Polaris Market Research has published a brand-new report titled U.S. Veterinary Active Pharmaceutical Ingredients Manufacturing Market Size, Share, Trends, Industry Analysis Report By Service Type (In-House, Contract Outsourcing), By Synthesis Type, By Animal Type, By Therapeutic Category – Market Forecast, 2025–2034 that includes extensive information and analysis of the...

You are not alone if you deal with pain, stiffness, or slow healing that makes it difficult to enjoy or fully actively participate in your life daily. People often seek simple, natural methods of improving their health without the use of medication or surgery; this is the purpose of Discover Lasers. Discover Lasers provides safe, user-friendly laser therapy products that can be used by...