Subsea Systems Market Size, Trends & Competitive Analysis — Forecast to 2034, CAGR 3.12%

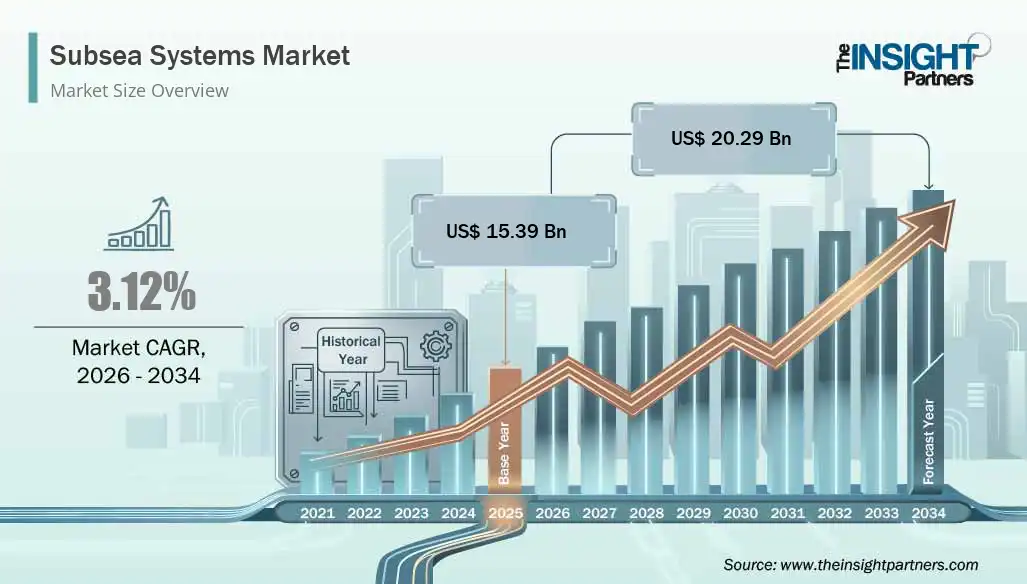

The global Subsea Systems Market is expected to grow steadily over the coming decade as energy companies continue to develop deepwater and ultra-deepwater reserves, modernize aging infrastructure, and invest in reliability and automation. The market size is projected to reach US$ 20.29 billion by 2034 from US$ 15.39 billion in 2025, registering a compound annual growth rate CAGR of 3.12% during the forecast period 2026–2034.

Market drivers

-

Continued exploration and production in deepwater and ultra-deepwater fields increases demand for subsea production systems, umbilicals, flexible pipes, and related control equipment.

-

Aging offshore infrastructure requires brownfield investments for life extension, integrity management, and replacement of subsea components.

-

Technological advancements such as digitalization, remote monitoring, and subsea processing improve operational efficiency and reduce the need for surface intervention.

-

Higher oil and gas price volatility encourages investment in lower-cost, higher-recovery subsea tiebacks and marginal-field developments.

-

Growing focus on safety and environmental regulations drives adoption of robust, reliable subsea systems that minimize leak and failure risks.

Implications for operators and suppliers

Operators can extend field life and lower break-even costs by selectively deploying subsea processing, tiebacks, and electrification solutions. Suppliers that offer modular, scalable subsea systems and strong aftermarket services will be better positioned to capture recurring revenue from maintenance, upgrades, and field life-extension projects. Contract models linking performance to uptime and reliability may become more prevalent.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00014385

Market restraints and challenges

-

High capital expenditure and extended project lead times for deepwater developments can slow procurement and deployment of subsea systems.

-

Complex marine conditions, supply-chain constraints, and skilled-labor shortages create execution risks and cost overruns.

-

Volatility in oil and gas markets and shifts toward renewable energy sources can reduce long-term investment appetite in hydrocarbon-focused subsea projects.

-

Technical complexity of subsea processing and electrification requires significant R&D and testing before wide commercial rollout.

Segment trends

-

Subsea production systems and control systems remain core revenue generators, supported by demand for subsea trees, manifolds, and intervention tooling.

-

Umbilicals and flexible pipes benefit from tie-back projects and the need for longer-distance subsea connections.

-

Subsea robotics and ROVs (remotely operated vehicles) see increased adoption for inspection, maintenance, and repair, aided by improvements in autonomy and sensor suites.

-

Electrification and hydraulic-to-electric conversions on the seabed drive uptake of subsea power distribution and subsea control modules.

Regional outlook

-

The North America market, led by Gulf of Mexico activity, continues to attract investments in tiebacks and brownfield projects.

-

The Asia Pacific region shows rising demand driven by offshore developments in Southeast Asia and Australia.

-

The Middle East & Africa remain important for ultra-deep projects and strategic subsea developments off West Africa.

-

Europe sustains steady demand through North Sea projects focused on life extension, decommissioning planning, and electrified subsea systems.

Key players

-

Aker Solutions

-

Baker Hughes (General Electric Company)

-

Bechtel Corporation

-

Howco Group plc

-

National Oilwell Varco

-

Nexans S.A.

-

Oceaneering International, Inc.

-

OneSubsea (Schlumberger Limited)

-

Parker Hannifin Corporation

-

TechnipFMC plc

Competitive dynamics

Leading firms differentiate through integrated service offerings, strategic alliances with operators, and investment in digital and subsea-processing technologies. Mergers, joint ventures, and long-term supply agreements remain common strategies to secure megaprojects and reduce project delivery risk. Smaller and specialized suppliers carve niche positions by offering tailored components, obsolescence management, and rapid-response subsea intervention services.

Future Outlook

Over the forecast period, the subsea systems market is expected to balance traditional oil and gas drivers with incremental adoption of electrification, digitalization, and subsea processing. While growth is moderate projected at a 3.12% CAGR innovation will create opportunities for value capture beyond hardware sales, especially in service contracts, remote operations, and lifecycle management. Companies that invest in R&D, build flexible supply chains, and form operator partnerships will capture most value as the industry pursues safer, more efficient, and lower-carbon subsea production solutions.

Related Reports–

Subsea Well Access and BOP System Market

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

الأقسام

إقرأ المزيد

If you’re weighing private knee replacement in Canada, expect a typical price range of about CAD 18,000 to CAD 35,000 depending on surgeon, implant, and facility. The cost of private knee replacement in Canada can vary significantly based on the clinic, technology used, and level of postoperative care included. That range gives you a realistic starting point so you can compare clinics,...

Most people quit skincare too early. That’s the real problem. When you use an at home light therapy skincare device consistently for 30 days, you finally give your skin enough time to respond and show visible change. If you’ve been searching for laser mask results after 30 days or wondering what happens when you use a laser mask daily, this guide walks you...

A receding hairline is one of the most common forms of hair loss affecting both men and women. In modern aesthetic medicine, receding hairline restoration has become highly advanced, offering multiple effective solutions for those seeking a fuller and more youthful appearance. In Hair Transplant in Abu Dhabi, individuals now have access to a wide range of hair restoration techniques designed to...

Will Ferrell marks his television comedy debut portraying a legendary golfer in this highly anticipated series. His frequent rival on the greens, played by Luke Wilson, is a pro golfer who has bested Ferrell's character twice for the tour championship. Adding comedic firepower is Ferrell's longtime collaborator Molly Shannon, taking on the role of Stacy across all ten episodes. Chris Parnell...

"Asia-Pacific Bacteriophages Therapy Market Summary: According to the latest report published by Data Bridge Market Research, the Asia-Pacific Bacteriophages Therapy Market The Asia-Pacific Bacteriophages Therapy Market size was valued at USD 10.82 Billion in 2025 and is expected to reach USD 18.73 Billion by 2033, at a CAGR of 7.10% during the forecast period To impart a supreme...