Neodymium Magnets in Electric Vehicles: The Small Metal Core Quietly Deciding Motor Efficiency, Range, Supply Security, and the Next EV Infrastructure Race

Neodymium Magnets in Electric Vehicles: The Small Metal Core Quietly Deciding Motor Efficiency, Range, Supply Security, and the Next EV Infrastructure Race

The electric vehicle story is usually told through battery packs, charging stations, lithium prices, and gigafactories. But inside the motor, a smaller material is doing a disproportionate amount of work. Neodymium magnets in electric vehicles sit inside traction motors, power steering systems, braking systems, thermal management pumps, sensors, seat motors, compressors, and auxiliary actuators. A modern battery electric car may use 1–3 kg of rare-earth permanent magnets in the traction motor alone, while premium models with more motorized comfort, ADAS, and thermal systems can carry dozens of smaller magnet-driven motion points.

Semple Request At: https://datavagyanik.com/reports/neodymium-magnets-in-electric-vehicles-market-research-insights-market-size-analysis-and-forecast-competitive-landscape-market-share/

The reason is simple: weight is money in an EV. Every kilogram removed from the motor housing, cooling system, gearbox, and power electronics improves range, acceleration, packaging, or battery economics. Neodymium magnets in electric vehicles allow compact motors to produce high torque density without needing larger copper windings, heavier induction systems, or oversized cooling assemblies. In a 150 kW EV traction motor, the permanent magnet rotor can help convert electrical energy into wheel torque with efficiency levels that often cross 90% under optimized operating conditions. Even a 1–2 percentage point efficiency gain becomes meaningful when a vehicle travels 150,000–250,000 km over its life.

The infrastructure angle begins with the global EV fleet itself. Global electric car sales crossed 20 million units in 2025, meaning roughly one in four new cars sold worldwide was electric. That one statistic turns Neodymium magnets in electric vehicles from a component story into an infrastructure story. If 20 million EVs require only 1.5 kg of rare-earth magnet material per traction system on average, the annual motor-side pull becomes nearly 30,000 tonnes of magnet demand before counting e-buses, electric trucks, two-wheelers, compressors, pumps, and steering motors. A 100,000-unit EV platform can therefore lock in 150–300 tonnes of magnet demand depending on motor architecture and vehicle class.

This is why automakers treat Neodymium magnets in electric vehicles as a range, sourcing, and geopolitical design decision. A single permanent magnet synchronous motor can deliver high low-speed torque, good highway efficiency, and compact packaging. For city EVs, it reduces drivetrain losses in stop-start traffic. For SUVs, it supports heavier curb weight and dual-motor layouts. For electric buses, it improves climb performance and energy use across long duty cycles. For performance EVs, it supports instant torque without making the motor physically oversized.

According to DataVagyanik, the Neodymium magnets in electric vehicles market is estimated at USD 5.96 billion in 2026 and is forecast to reach USD 10.68 billion by 2032, expanding at a CAGR of 10.2% during 2026–2032. This value is being pulled by higher EV production, rising permanent magnet motor penetration, dual-motor passenger EV platforms, electric commercial vehicles, thermal-management electrification, and the shift from basic traction motor procurement to qualified, high-temperature NdFeB magnet supply contracts.

The use-case map is wider than the traction motor. Neodymium magnets in electric vehicles also appear in electric power steering motors, brake-by-wire actuators, active suspension systems, HVAC blowers, electric compressors, coolant pumps, seat adjusters, door locks, speakers, charging-port actuators, and battery thermal-control valves. A low-cost EV may have fewer than 50 motorized subsystems, while a premium EV can easily cross 100 motion-control points. If only 40 of those points use compact permanent magnet motors, the magnet story spreads from drivetrain engineering into cabin comfort, safety, software-defined vehicle architecture, and maintenance economics.

A traction motor is the visible use case, but thermal management is becoming the quiet growth zone. EV batteries operate best in a controlled temperature window, typically around 20–40°C depending on chemistry and operating condition. That creates demand for electric coolant pumps, refrigerant compressors, battery chiller valves, cabin heat-pump motors, and inverter cooling loops. Neodymium magnets in electric vehicles support these compact, high-duty-cycle motors because thermal systems must run repeatedly during fast charging, winter driving, hot-climate parking, and battery preconditioning. A 350 kW fast-charging event can push thermal systems into heavy operation even when the vehicle is stationary.

The charging infrastructure story also feeds magnet demand indirectly. Every new fast-charging corridor increases the practical value of EVs that can accept high charging loads, and high charging loads create stronger battery thermal-management requirements. A vehicle that charges from 10% to 80% in 20–30 minutes must move heat quickly, precisely, and repeatedly. That means more electrically driven pumps, valves, blowers, and compressors. Neodymium magnets in electric vehicles therefore benefit not just from the number of EVs sold, but from the intensity of charging, software-controlled cooling, and battery-size growth.

The supply chain is more concentrated than most EV buyers realize. Neodymium magnets in electric vehicles depend on rare-earth mining, separation, oxide production, metal/alloy making, strip casting, powdering, pressing, sintering, machining, coating, magnetizing, and motor qualification. Missing one step can break the chain. A magnet producer must control oxygen exposure, grain size, coercivity, dysprosium or terbium use, coating quality, and dimensional tolerance. For EV motors, this is not a commodity block of metal; it is a qualified magnetic component that must survive heat, vibration, corrosion, and demagnetization risk across a vehicle life of 8–15 years.

The 2024–2026 investment timeline shows how strategic this became. In March 2024, Europe’s Critical Raw Materials Act set 2030 capacity ambitions across extraction, processing, recycling, and external dependency reduction. In 2025, U.S. policy support accelerated with large public-private funding around rare-earth magnets, including MP Materials’ magnet manufacturing expansion and offtake-linked supply strategy. In late 2025, eVAC’s South Carolina facility shipped U.S.-made NdFeB magnets, signaling that commercial magnet production outside Asia is moving from policy presentation to factory output. These events matter because Neodymium magnets in electric vehicles cannot scale only through automaker purchase orders; they need upstream chemical separation, alloy capacity, skilled magnet manufacturing, and long qualification cycles.

The technical bottleneck is not only neodymium. High-temperature EV motors may require praseodymium, dysprosium, or terbium additions to maintain coercivity under heat. Heavy rare earths are expensive, supply-sensitive, and politically strategic. A motor operating near 150°C has different magnet requirements than a mild auxiliary motor under the dashboard. For this reason, Neodymium magnets in electric vehicles are increasingly designed through grain-boundary diffusion, reduced-heavy-rare-earth formulations, improved cooling, segmented magnet shapes, and rotor designs that use less material per kilowatt.

The economics can be quantified at vehicle level. If a traction motor uses 2 kg of NdFeB magnet material and magnet pricing swings by USD 20 per kg, the direct magnet cost exposure is USD 40 per vehicle before qualification, machining, coatings, scrap, logistics, and supplier margin. For a 500,000-unit EV platform, that same movement becomes USD 20 million of procurement exposure. If the vehicle uses dual motors, exposure rises further. That is why automakers are not only asking “how much magnet per motor?” but also “which supplier, which alloy, which country, which coating, which qualification path, and which recycling route?”

Neodymium magnets in electric vehicles are also changing the motor-architecture debate. Induction motors avoid rare earths but can carry efficiency and weight trade-offs. Switched reluctance motors reduce magnet dependence but need careful noise, vibration, torque ripple, and control optimization. Ferrite-assisted motors lower rare-earth exposure but usually require larger motor volume. Permanent magnet motors remain attractive because they compress efficiency, torque, and size into a package that fits mass-market EV platforms. This is why many automakers experiment with magnet reduction, but few can ignore magnet performance completely.

How Neodymium Magnets in Electric Vehicles Turn Motor Design Into an Industrial Strategy

The second layer of this story is manufacturing geography. Almost 22 million electric cars were produced globally in 2025, and nearly three-fourths of that production came from China. That means the largest pull for Neodymium magnets in electric vehicles is not spread evenly across the world; it is concentrated around Chinese EV platforms, Chinese motor suppliers, Chinese magnet producers, and Chinese rare-earth processing capacity. When one country produces close to 75% of electric cars and also dominates rare-earth magnet supply, the magnet becomes both a component and an industrial control point.

This concentration is why Western EV supply chains are being rebuilt around magnet localization. A battery plant can be announced with gigawatt-hour capacity, but a magnet plant has a different timeline. It needs rare-earth oxide supply, metal conversion, alloy making, sintering, machining, coating, magnetic-property testing, and customer approval. For Neodymium magnets in electric vehicles, the qualification cycle can run 18–36 months because automakers must validate torque output, thermal stability, corrosion resistance, noise behavior, crash durability, and long-term demagnetization risk. A factory may be built in two years, but a qualified EV magnet supply chain often takes longer.

MP Materials’ U.S. magnet facility illustrates the scale logic. Its Texas-based magnet manufacturing plan targets around 1,000 metric tons per year of finished NdFeB magnets as production ramps. If an EV traction motor uses 1.5–2.5 kg of magnet material, that one facility’s theoretical traction-motor equivalent supply could support roughly 400,000–650,000 EVs annually, depending on vehicle architecture and magnet loading. That sounds large, but it covers only a fraction of North America’s potential EV production base. This is why Neodymium magnets in electric vehicles remain a capacity story even after the first localized plants come online.

Europe faces a similar equation. The European Union’s 2030 critical raw material targets are not only about mining; they are about reducing exposure at processing and recycling stages. If Europe wants to build millions of EVs annually, it cannot depend only on imported finished magnets while localizing battery cells and vehicle assembly. Neodymium magnets in electric vehicles require a full chain: rare-earth separation, alloy production, magnet forming, motor integration, and recycling. Without those middle steps, European automakers may assemble EVs locally but still import the magnetic heart of the drivetrain.

Japan and South Korea add another layer. Japanese firms such as Shin-Etsu Chemical and TDK have deep rare-earth magnet and materials expertise, while South Korean EV and battery groups are scaling high-volume electric platforms. But heavy rare-earth dependency, especially dysprosium and terbium for high-temperature magnet grades, remains a pressure point. When rare-earth export restrictions appear, the immediate risk is not always neodymium itself; it is the smaller-volume additives that allow Neodymium magnets in electric vehicles to survive high motor temperatures without performance loss.

The technology response is already measurable. Motor engineers are reducing magnet volume per kilowatt through better rotor design, segmented magnet placement, improved cooling channels, and stronger electromagnetic simulation. Magnet producers are reducing heavy rare-earth loading through grain-boundary diffusion, where dysprosium or terbium is concentrated near grain surfaces instead of being used uniformly across the magnet. If this cuts heavy rare-earth use by even 20–40% in selected high-performance grades, it changes both cost and supply risk. Neodymium magnets in electric vehicles are therefore being optimized not only for magnetic strength, but for material thrift.

At the vehicle level, magnet intensity depends on platform strategy. A front-wheel-drive compact EV with one permanent magnet motor may use a lower magnet load than a dual-motor SUV with performance-oriented torque delivery. A three-row electric SUV, electric pickup, or high-performance sedan can use two traction motors, raising magnet demand per vehicle. If 30% of a platform’s sales move from single-motor to dual-motor trims, magnet demand can rise much faster than unit sales. That is why Neodymium magnets in electric vehicles should be measured not only by EV volume, but by motor count per vehicle.

Commercial vehicles sharpen the equation. Electric buses, delivery vans, and medium-duty trucks have higher duty cycles than passenger cars. A city e-bus may run 200–300 km per day, 300 days per year, with repeated acceleration, regenerative braking, and heat exposure. The motor must deliver reliability under high load, frequent stop-start movement, and long operating hours. Neodymium magnets in electric vehicles used for commercial fleets therefore face harsher validation than magnets used in small auxiliary motors. Fleet downtime converts directly into operating losses, so magnet failure tolerance is extremely low.

The infrastructure use case also includes repair and replacement economics. EV motors are designed as long-life assemblies, but the growing installed base creates downstream demand for replacement traction units, remanufactured drive modules, and recycled magnet recovery. A country with 5 million EVs on the road will eventually have thousands of motor units entering repair, collision replacement, and end-of-life streams each year. Neodymium magnets in electric vehicles can be recovered, reprocessed, or reused, but only if dismantling, demagnetization, separation, and alloy-refining systems are economically organized.

Recycling is becoming a strategic lever because magnet scrap has high material density compared with low-grade ore. Production scrap from magnet manufacturing, motor assembly rejects, and end-of-life rotors can contain recoverable neodymium, praseodymium, dysprosium, and terbium. If a magnet plant has a 5–10% process scrap rate, a 1,000-tonne annual facility may generate 50–100 tonnes of internal magnet scrap even before post-consumer recycling. That scrap stream is valuable because it has known chemistry and lower contamination than mixed end-of-life waste. For Neodymium magnets in electric vehicles, circular supply starts inside the factory before it reaches scrapyards.

The pricing story is also changing from commodity pricing to qualification pricing. A standard industrial NdFeB magnet is not priced like an automotive traction-grade magnet. EV-grade magnets need tight tolerances, thermal ratings, corrosion-resistant coatings, batch traceability, and audit-ready documentation. A supplier that can deliver 10,000 units is not equal to one that can deliver 10 million units with consistent magnetic performance. Neodymium magnets in electric vehicles therefore carry a qualification premium. Automakers pay not only for rare-earth content, but for reliability, documentation, low defect rates, and supply continuity.

This is why the buyer map is complex. Automakers may not always buy magnets directly. Tier-1 motor suppliers, e-axle manufacturers, pump makers, steering system suppliers, and actuator producers may procure magnets and integrate them into assemblies. A single EV platform can involve magnet demand through the main traction supplier, HVAC supplier, steering supplier, braking supplier, seat supplier, audio supplier, and thermal-management supplier. Neodymium magnets in electric vehicles therefore move through a layered supply chain where the final car brand may be several steps away from the magnet manufacturer.

The motor supplier ecosystem shows this clearly. Companies such as Bosch, BorgWarner, Nidec, Valeo, Denso, Hitachi Astemo, Magna, ZF, and several China-based e-drive suppliers are not simply buying generic magnet blocks. They are optimizing full e-axle packages around torque density, inverter compatibility, cooling, cost, noise, and packaging. For each platform, the magnet geometry, grade, coating, and assembly method are matched to rotor design. Neodymium magnets in electric vehicles become part of a systems-engineering decision, not a loose materials purchase.

China’s scale advantage comes from this full-system connection. Rare-earth separation, magnet manufacturing, motor design, EV assembly, and domestic demand are clustered closely. This reduces logistics friction, shortens engineering feedback loops, and allows rapid design iteration. If a magnet grade needs adjustment, the feedback path from EV motor testing to magnet supplier can be faster. For Neodymium magnets in electric vehicles, this cluster advantage is one reason China can scale platforms quickly while other regions are still building upstream capacity.

India’s case is different but important. India is already large in electric two-wheelers and three-wheelers, and it is building electric bus and passenger EV capacity. Many small EVs use lower magnet volumes than premium cars, but the unit count is high. A million electric two-wheelers using smaller permanent magnet motors can still generate a significant magnet pull across hub motors, mid-drive motors, controllers, and auxiliary systems. Neodymium magnets in electric vehicles in India are therefore not only a passenger-car story; they are tied to scooters, rickshaws, buses, small commercial vehicles, and localized component manufacturing.

The next technical frontier is magnet-light design rather than magnet-free design. Automakers want lower rare-earth exposure, but they also want compact motors, high efficiency, and predictable performance. That is pushing hybrid solutions: ferrite-assisted motors, optimized reluctance torque, reduced-NdFeB rotors, and better software control. If a redesigned motor reduces magnet content by 15% while keeping the same power output, a 1 million vehicle platform can save 300 tonnes of magnet material at a 2 kg baseline. Neodymium magnets in electric vehicles will not disappear; they will be engineered more carefully.

Semple Request At: https://datavagyanik.com/reports/neodymium-magnets-in-electric-vehicles-market-research-insights-market-size-analysis-and-forecast-competitive-landscape-market-share/

Categories

Read More

Buy CNC tools online for accurate, high-speed machining. Explore durable, precision CNC tools at competitive prices from a trusted supplier. High-Quality CNC Tools Designed for Fast, Precise Machining. In today’s advanced manufacturing environment, speed and precision are no longer optional—they are essential....

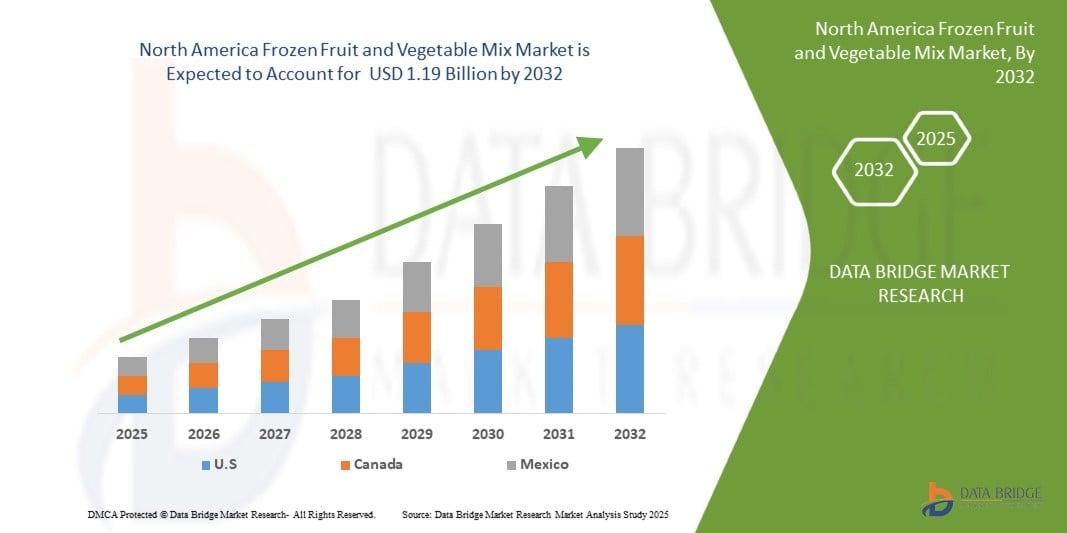

"North America Frozen Fruit & Vegetable Mix Market Summary: According to the latest report published by Data Bridge Market Research, the North America Frozen Fruit and Vegetable Mix Market The North America Frozen Fruit & Vegetable Mix Market size was valued at USD 1.13 billion in 2024 and is expected to reach USD 1.19 billion by 2032, at a CAGR of...

Introduction Many people today are searching for long-term grooming solutions that save both time and money. That is why Laser Hair Removal Sheepshead Bay, Brooklyn NY has become one of the most requested cosmetic treatments in the area. Whether you are tired of shaving every few days or dealing with irritation from waxing, laser hair removal offers a more convenient and...

"Executive Summary Four Side-Sealed Pouches Market Size, Share, and Competitive Landscape The four side-sealed pouches market size was valued at USD 1.11 billion in 2024 and is projected to reach USD 1.80 billion by 2032, with a CAGR of 6.20% during the forecast period of 2025 to 2032. An exceptional Four Side-Sealed Pouches Market research document can be formulated well...

The Optical Brighteners market report is intended to function as a supportive means to assess the global Optical Brighteners market along with the complete analysis and clear-cut statistics related to this market. In other words, the report would provide an up-to-date study of the market in terms of its latest trends, present scenario, and the overall market situation. Further, it...