GCC Flooring Market to Explode from USD 3.8 Billion to USD 5.2 Billion by 2024 – 11.5% CAGR

Global GCC Countries Flooring Market was valued at USD 3.8 billion in 2021 and is projected to reach USD 5.2 billion by 2024, exhibiting a significant CAGR of 11.5% during the forecast period.

The flooring market in the Gulf Cooperation Council (GCC) region, comprising Saudi Arabia, the United Arab Emirates, Qatar, Kuwait, Oman, and Bahrain, is a dynamic and rapidly evolving sector. It is directly fueled by the region's ambitious economic diversification plans outlined in national visions like Saudi Vision 2030 and the continued expansion of the tourism and hospitality industries, particularly in the UAE and Qatar. This market is characterized by a sophisticated consumer base with a strong preference for high-end, durable, and aesthetically pleasing flooring solutions that can withstand the region's unique climatic conditions while offering superior performance.

Get Full Report Here: https://www.24chemicalresearch.com/reports/123060/global-gcc-countries-flooring-market-2022-51

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

- Mega Infrastructure and Real Estate Projects: The GCC is home to some of the world's most ambitious construction projects. Saudi Arabia's giga-projects, including NEOM, the Red Sea Project, and Qiddiya, represent investments exceeding $1 trillion and require massive quantities of flooring materials. Similarly, the UAE's preparations for events like the Dubai Expo 2020 have spurred long-term development, while Qatar's post-2022 FIFA World Cup infrastructure push continues to drive demand. These projects, often specifying premium, long-lasting materials, create a sustained, high-value demand pipeline for the flooring industry.

- Rising Disposable Income and Urbanization: High per capita incomes in GCC nations fuel a robust residential construction and renovation sector. There is a growing preference for luxury vinyl tiles (LVT), high-end ceramic tiles, and engineered wood flooring over traditional materials, as consumers seek to elevate their living spaces. This trend is accelerated by rapid urbanization, with populations increasingly concentrated in major cities like Dubai, Riyadh, and Doha, leading to a boom in apartment complexes and villas that all require quality flooring solutions.

- Thriving Hospitality and Retail Sectors: The GCC's strategic focus on becoming a global tourism and retail hub directly benefits the commercial flooring segment. The development of luxury hotels, shopping malls, entertainment centers, and airports demands specialized flooring that is not only visually appealing but also highly durable, easy to maintain, and capable of handling heavy foot traffic. Materials like commercial-grade carpet tiles, homogeneous vinyl, and polished concrete are seeing increased adoption due to their performance characteristics.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/123060/global-gcc-countries-flooring-market-2022-51

Significant Market Restraints Challenging Adoption

Despite its promising outlook, the market faces hurdles that must be overcome to achieve optimal growth.

- Volatility in Raw Material Prices and Supply Chain Disruptions: The flooring industry is highly susceptible to fluctuations in the prices of key raw materials such as polyvinyl chloride (PVC) for vinyl flooring, polymers for carpets, and ceramics. Global supply chain bottlenecks, as witnessed recently, can lead to significant delays and cost escalations, impacting project timelines and profitability for manufacturers and contractors. This volatility creates pricing instability, making budget forecasting challenging for large-scale projects.

- Intense Competition and Price Sensitivity: The GCC flooring market is highly competitive, with a mix of large international players and numerous local distributors. This often leads to price wars, particularly in the more standardized product segments, squeezing profit margins. While there is demand for premium products, a significant portion of the market remains price-sensitive, especially in the mid-range residential and certain commercial sectors, forcing suppliers to balance quality with competitive pricing.

Critical Market Challenges Requiring Innovation

The unique environmental and logistical context of the GCC presents specific challenges. The harsh climate, characterized by extreme heat, high humidity in coastal areas, and sand, demands flooring materials with exceptional resistance to UV degradation, thermal expansion, and abrasion. Not all products available globally meet these stringent requirements, necessitating specialized formulations and testing.

Furthermore, a shortage of highly skilled installation and maintenance professionals for advanced flooring systems can lead to improper installation, compromising performance and longevity. Ensuring a trained workforce is a persistent challenge that the industry must address through targeted training programs and certification initiatives to maintain quality standards.

Vast Market Opportunities on the Horizon

- Sustainable and Green Building Materials: There is a rapidly growing emphasis on sustainability, driven by government regulations like the UAE's Estidama Pearl Rating System and the increasing corporate focus on ESG (Environmental, Social, and Governance) criteria. This creates a substantial opportunity for eco-friendly flooring options such as bio-based tiles, flooring with high recycled content, and products with low VOC (Volatile Organic Compound) emissions. Companies that can offer certified sustainable solutions are well-positioned to capitalize on this burgeoning segment.

- Technological Advancements in Smart Flooring: The concept of smart buildings is gaining traction in the GCC's luxury real estate and commercial sectors. This opens the door for innovative flooring solutions with integrated technologies, such as underfloor heating and cooling systems, and even floors with embedded sensors for monitoring foot traffic, temperature, or security. While still a niche, this segment represents a high-growth frontier for technologically advanced flooring manufacturers.

- E-commerce and Digital Transformation: The pandemic accelerated the shift towards online purchasing behaviors. Developing robust e-commerce platforms for flooring samples, visualization tools (like augmented reality apps to preview floors in a room), and streamlined supply chains for direct-to-consumer or B2B sales presents a significant opportunity to reach a wider audience and improve customer experience.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Ceramic Tiles, Vinyl Flooring, Carpet & Rugs, Wood & Laminate, and others. Ceramic Tiles currently dominate the market, favored for their durability, ease of maintenance, and suitability to the hot climate. However, Vinyl Flooring, particularly LVT, is exhibiting the highest growth rate due to its versatility, water resistance, and advanced designs that convincingly mimic wood and stone at a lower cost.

By Application:

Application segments are broadly divided into Residential and Commercial. The Commercial segment accounts for the largest market share, driven by massive investments in hospitality, retail, healthcare, and office infrastructure. The Residential segment is also growing robustly, supported by population growth, urbanization, and rising disposable incomes.

By End-User Industry:

The end-user landscape includes Construction, Hospitality, Retail, Healthcare, and others. The Construction industry is the primary driver, as it encompasses both residential and commercial building activities. The Hospitality sector is a key growth end-user, constantly requiring high-quality, aesthetically pleasing, and durable flooring for hotels, resorts, and restaurants to maintain a luxury image.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/123060/global-gcc-countries-flooring-market-2022-51

Competitive Landscape:

The GCC Flooring market is fragmented and highly competitive, characterized by the presence of both multinational giants and strong regional players. The top companies—Mohawk Industries, Tarkett, and Armstrong Flooring—leverage their global brand reputation, extensive product portfolios, and strong distribution networks to maintain significant influence.

List of Key Flooring Companies Profiled:

● Mohawk Industries (U.S.)

● Tarkett (France)

● Armstrong Flooring (U.S.)

● Gerflor (France)

● Mannington Mills (U.S.)

● Shaw Industries (U.S.)

● Rashid Al Rashid & Sons. (U.A.E.)

● RAK Ceramics (U.A.E.)

● Graniti Faenza (Italy)

● Asian Granito (India)

● Kajaria Ceramics (India)

● Interface, Inc. (U.S.)

Competitive strategies are centered on product innovation, particularly in sustainable and luxury vinyl tile segments, and strengthening distribution channels through partnerships with local contractors and dealers. Providing comprehensive solutions, including installation and maintenance services, is also a key differentiator in this market.

Regional Analysis: A Market Fueled by Visionary Development

● United Arab Emirates and Saudi Arabia: Together, these two nations are the undeniable powerhouses of the GCC flooring market, collectively accounting for over 70% of the regional market share. The UAE, with Dubai and Abu Dhabi as epicenters, leads in commercial and luxury residential demand. Saudi Arabia's market is currently the largest and fastest-growing, driven overwhelmingly by the implementation of its giga-projects and broader Vision 2030 infrastructure plans, creating unprecedented demand across all flooring segments.

● Qatar, Kuwait, and Oman: This group forms a strong secondary market. Qatar continues to benefit from its ongoing infrastructure development post-World Cup. Kuwait and Oman are experiencing steady growth driven by government housing initiatives and diversification efforts in tourism and logistics, respectively, contributing to a consistent demand for flooring materials.

● Bahrain: While the smallest market in the GCC, Bahrain presents stable opportunities, primarily driven by residential construction, retail sector growth, and renovations in the hospitality industry. Its market is characterized by a high degree of import dependency for flooring products.

Get Full Report Here: https://www.24chemicalresearch.com/reports/123060/global-gcc-countries-flooring-market-2022-51

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/123060/global-gcc-countries-flooring-market-2022-51

Other related reports

https://www.24chemicalresearch.com/reports/286578/latin-america-titanium-dioxide-market-2025-2032-91

https://www.24chemicalresearch.com/reports/272300/global-butyrospermum-parkii-butter-extract-market

https://www.24chemicalresearch.com/reports/181046/north-america-automotive-power-steering-fluid-market

https://www.24chemicalresearch.com/reports/154787/global-regional-engineered-stone-countertops-market-2022-2027-77

https://www.24chemicalresearch.com/reports/185762/global-sprayon-insulation-coatings-forecast-market-2022-2028-859

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Categorias

Leia mais

Fortnite Birthday Celebration Celebrating Fortnite's Anniversary: A Guide to Completing Birthday Quests in 2025 Join in the festivities as Fortnite commemorates its yearly birthday event, a time filled with special challenges and exclusive rewards. To make the most of this celebration, players can undertake a variety of themed quests designed to test their skills and add fun to their...

Brain health is essential for everything we do each day. From remembering names and making decisions to managing emotions and staying focused, the brain controls how we think, feel, and act. When the brain is healthy, daily life feels smoother and more manageable. When it is not, even simple tasks can feel overwhelming. This article explains brain health in simple, engaging language for...

Introduction: Complete Comparison of Leading Online Betting Apps in India The online betting industry in India has grown rapidly due to smartphones, high-speed internet, and a rising sports fan base. Online betting apps now provide convenience, speed, and a variety of gaming options to millions of users across the country. With so many platforms available, choosing the right one can be...

The modern landscape of Supply Chain Analytics Solutions is rich and varied, offering a spectrum of platforms and tools tailored to meet diverse organizational needs, budgets, and levels of technical maturity. At a high level, these solutions can be categorized by their deployment model. Traditional on-premises software involves installing and running the application on a company's...

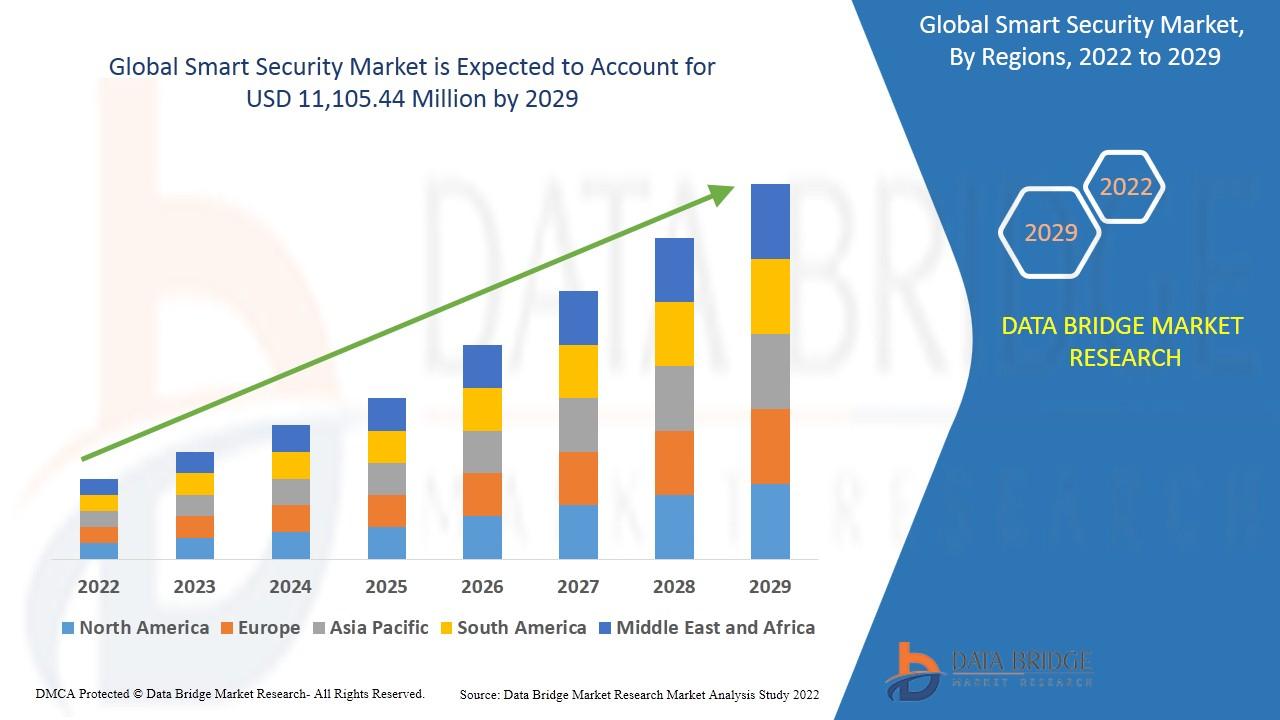

"Global Executive Summary Smart Security Market Market: Size, Share, and Forecast CAGR Value Data Bridge Market Research analyses that the smart security market will exhibit a CAGR of 9.80% for the forecast period of 2022-2029 and is expected to reach the market value of USD 11,105.44 million by 2029. The global Smart Security Market Market analysis report gives a careful overview of the...