From Conventional to Imaging Radar: Automotive 4D Radar Market Size, Share, and Outlook (2025–2034)

The automotive 4D imaging radar market is moving from “incremental ADAS sensing upgrades” to a foundational perception layer for next-generation assisted driving as OEMs seek higher confidence, wider operational envelopes, and better redundancy across weather, lighting, and complex traffic scenes. 4D imaging radar refers to advanced radar systems that generate richer point-cloud-like outputs by resolving objects in range, azimuth, elevation, and relative velocity, enabling improved object separation, better classification cues, and more stable tracking compared with conventional long-range or corner radars. Unlike traditional radar that excels in range and speed but provides limited angular resolution, 4D imaging radar is designed to deliver finer spatial detail—supporting applications such as highway pilot functions, traffic jam assist, automated lane changes, forward collision avoidance, cross-traffic detection, and robust vulnerable road user awareness in scenarios where cameras can be degraded by glare, darkness, or precipitation. Between 2025 and 2034, the market outlook is expected to remain structurally positive as ADAS penetration broadens across price tiers, OEMs accelerate sensor fusion roadmaps, and regulatory as well as consumer safety expectations continue to rise—pushing sensing stacks toward higher-performance, software-defined platforms.

Market overview and industry structure

The Automotive 4D Imaging Radar Market was valued at $87.1 million in 2025 and is projected to reach $9026.9 million by 2034, growing at a CAGR of 67.5%.

Automotive 4D imaging radar sits within the broader ADAS and automated driving sensor ecosystem that includes cameras, ultrasonic sensors, LiDAR in select programs, GNSS/IMU positioning, and high-performance compute running perception, prediction, and control. 4D imaging radar systems are generally deployed as forward-facing radars (long-range, high-resolution) and, increasingly, as higher-resolution corner radars that improve near-field perception around the vehicle. The defining feature is the combination of advanced antenna architectures (often MIMO arrays), higher channel counts, refined waveform and signal processing, and algorithms that deliver denser, more accurate spatial detections with elevation information—reducing ghost targets and improving separation of closely spaced objects.

The value chain is anchored by semiconductor providers delivering radar transceivers and processing capability, Tier-1 suppliers integrating radar modules and providing functional safety-grade hardware and software stacks, and OEMs integrating sensors into vehicle platforms with tuning, calibration, and validation. In many programs, 4D imaging radar adoption is tightly tied to the evolution toward centralized ADAS domain controllers and zonal architectures, where fewer compute units process shared sensor data and enable multiple features through software. This structural shift favors suppliers that can provide not only the radar hardware but also the perception software interfaces, diagnostics, and lifecycle support required for continuous improvement via over-the-air updates.

Industry size, share, and adoption economics

Adoption economics for 4D imaging radar are shaped by a clear trade-off: higher sensor cost and integration complexity versus improved performance, redundancy, and feature scalability. OEMs increasingly view sensing as a platform investment—once a high-resolution radar is in place, it can support multiple functions (ACC, AEB enhancements, cut-in detection, lane-change assist, highway automation) and improve the reliability of camera-based systems through fusion. This “platform reuse” logic is central to the market’s growth: rather than adding sensors for each new feature, OEMs standardize a higher-capability sensor set and unlock functions through software packages and trim strategies.

Market share dynamics will increasingly concentrate around vendors that can scale volume production while meeting strict automotive-grade requirements: temperature robustness, electromagnetic compatibility, low failure rates, cybersecurity readiness, and functional safety compliance. Beyond technical performance, execution and validation maturity are decisive. 4D imaging radar must perform consistently across diverse road geometries, speeds, and traffic mixes, and it must be tuned to avoid false positives that degrade driver trust. As a result, suppliers with deep scenario libraries, simulation toolchains, and proven OEM integration experience tend to capture larger platform wins and long production runs.

Key growth trends shaping 2025–2034

- ADAS reliability expectations drive “sensor upgrade cycles”: Consumers and regulators increasingly expect advanced driver assistance features to work smoothly across real-world conditions. 4D imaging radar is being adopted as a pathway to reduce edge-case failures—improving detection in rain, fog, dust, night driving, and complex highway merges where camera-only systems can struggle.

- From “radar as support” to “radar as perception backbone” in some stacks: In certain architectures, high-resolution radar outputs are used more directly within object-level perception, not merely as confirmation. This supports stronger tracking stability, better separation of vehicles in adjacent lanes, and improved detection of stationary objects and cut-ins—especially when combined with camera fusion.

- Centralized compute and software-defined vehicles accelerate integration: As OEMs consolidate ECUs into ADAS domain controllers, they prefer sensors that provide richer data and can be upgraded through software. 4D imaging radar aligns with this shift because algorithm improvements (clutter suppression, classification cues, tracking) can continue post-sale, increasing lifetime value of the sensor platform.

- Higher-frequency innovation and packaging optimization: The market is seeing rapid innovation in antenna design, channel scaling, and module packaging to reduce size, weight, and cost while improving resolution. This enables broader deployment across vehicle segments, including mid-range models where cost sensitivity is higher.

- Safety, NCAP influence, and redundancy requirements strengthen demand: Safety rating programs and OEM risk management increasingly favor multi-sensor redundancy. 4D imaging radar is positioned as a key redundancy layer that improves confidence in AEB, ACC, and highway assistance functions, supporting both safety outcomes and brand reputation.

Core drivers of demand

A primary driver is the push to deliver more capable L2 and L2+ assisted driving experiences with fewer disengagements and less “jerky” behavior. High-resolution radar improves longitudinal control confidence by enhancing target selection, cut-in anticipation, and tracking stability, which directly impacts comfort and trust. Another major driver is the expansion of ADAS to mass-market vehicles. As sensor costs decline and platforms standardize, OEMs can offer richer safety packages across larger volumes, turning advanced sensing into a mainstream purchase factor.

Electrification also indirectly supports demand. EV platforms often adopt modern electrical architectures, centralized compute, and richer digital feature sets, which makes integration of advanced sensors more feasible and aligns with customer expectations for technology-forward vehicles. In parallel, commercial fleets and mobility operators increasingly value safety and downtime reduction; more robust sensing stacks reduce collision risk and can lower insurance and operational disruptions. Finally, regulatory attention on collision reduction and vulnerable road user safety raises the value of sensors that perform reliably across conditions and scenarios, strengthening the investment case for imaging radar.

Challenges and constraints

Despite strong tailwinds, adoption is constrained by cost, integration complexity, and validation burden. 4D imaging radar produces more data than conventional radar, which increases compute requirements, bandwidth needs, and software integration work. OEMs must manage sensor placement constraints behind bumpers and fascia materials, ensure thermal and environmental robustness, and maintain consistent calibration across manufacturing tolerances and repairs.

Performance tuning remains a critical challenge. Radar is sensitive to multipath reflections, clutter, and interference, especially in dense traffic or urban canyons. Imaging radar reduces some issues through better resolution, but it also introduces new tuning requirements to avoid false objects and unstable detections. Another constraint is functional safety and cybersecurity: as radar becomes more central to driving functions, suppliers must meet rigorous safety processes, secure firmware pipelines, and robust diagnostics. Finally, supply chain volatility in semiconductors and advanced packaging can influence availability and cost curves, affecting how quickly imaging radar moves from premium trims to mainstream platforms.

Browse more information

https://www.oganalysis.com/industry-reports/automotive-4d-imaging-radar-market

Segmentation outlook

By application, forward-facing imaging radar is expected to remain the anchor segment due to its direct impact on highway ADAS performance, while corner imaging radar grows as OEMs seek richer near-field perception for lane changes, merging, and cross-traffic scenarios. By vehicle segment, premium vehicles lead adoption due to higher willingness to pay and earlier deployment of L2+ suites, but the largest volume growth is expected in mid-range vehicles as costs decline and platform strategies standardize. By architecture, imaging radar adoption is tightly coupled with centralized ADAS compute and sensor fusion stacks, where richer radar outputs enable broader feature scalability. By channel, OEM fitment dominates due to safety liability, calibration requirements, and deep integration into vehicle software and validation frameworks.

Key Market Players

· Panasonic Corporation

· Denso Corporation

· Magna International Inc.

· ZF Friedrichshafen AG

· Continental AG

· Valeo S.A.

· Aptiv PLC

· Analog Devices Inc.

· Autoliv Inc.

· Velodyne Lidar Inc.

· Hella GmbH & Co. KGaA

· Robert Bosch GmbH

· Veoneer Inc.

· Topcon Positioning Systems Inc.

· First Sensor AG

· Blackmore Sensors and Analytics Inc.

· Ibeo Automotive Systems GmbH

· LeddarTech Inc.

· Ouster Inc.

· Innovusion Inc.

· Luminar Technologies Inc.

· Quanergy Systems Inc.

· Innoviz Technologies Ltd.

· Cepton Technologies Inc.

· AdaSky Technologies Ltd.

· FLIR Systems Inc.

· Xenomatix NV

· AEye Inc.

Competitive landscape and strategy themes

Competition spans radar module suppliers, semiconductor providers, and software stacks enabling perception and tracking. Key differentiation themes include angular resolution and elevation performance, robust detection under adverse weather, interference resilience, low false positive rates, and integration readiness with domain controllers and fusion frameworks. Through 2034, winning strategies are likely to include scaling high-channel-count radar hardware at automotive cost targets, offering software toolchains for tuning and validation, strengthening partnerships across chips-to-Tier-1-to-OEM integration, and supporting over-the-air update pipelines that allow continuous performance refinement. Vendors that can demonstrate measurable improvements—smoother ACC behavior, fewer false alerts, better cut-in detection, improved VRU awareness—will capture share in a market where real-world experience directly affects OEM brand value.

Regional dynamics (2025–2034)

Asia-Pacific is expected to remain a high-growth engine as China, Japan, and South Korea accelerate ADAS penetration across domestic OEM portfolios, supported by rapid innovation cycles, strong EV growth, and intense competition in L2 feature packaging that rewards higher-performance sensing stacks. North America is likely to see sustained demand driven by high highway mileage, strong adoption of ADAS in SUVs and pickups, and consumer preference for convenience features such as ACC and highway assist, with imaging radar adoption strengthening as OEMs pursue more consistent performance and redundancy. Europe is expected to maintain robust growth supported by safety-driven purchasing behavior, mature supplier ecosystems, and strong emphasis on functional safety validation and comfort tuning; the region’s regulatory and rating environment encourages wider fitment of advanced sensing and supports premiumization of ADAS suites. Latin America is expected to grow steadily from a lower base as ADAS content expands in higher trims and locally assembled models, with adoption shaped by affordability and localization of sensor supply chains. Middle East & Africa growth is expected to be selective but improving, led by higher-end vehicle mix and rising preference for safety features, while broader penetration will depend on cost targets, service ecosystem maturity, and OEM product mix over time.

Forecast perspective (2025–2034)

From 2025 to 2034, the automotive 4D imaging radar market is positioned for durable growth as assisted driving becomes more mainstream and OEMs prioritize reliability across real-world conditions. The market’s center of gravity shifts from “feature add-on radar upgrades” to “platform-level sensing,” where richer radar perception supports safer, smoother, and more scalable ADAS suites. Growth will be strongest in programs that standardize advanced sensor sets and unlock capability through software, supported by centralized compute and continuous validation improvements. By 2034, 4D imaging radar is likely to be widely viewed as a core sensing pillar—complementing cameras and, in select cases, LiDAR—enabling the redundancy, confidence, and consistency required for increasingly capable, software-defined assisted driving experiences.

Browse Related Reports

https://www.oganalysis.com/industry-reports/automotive-keyless-entry-systems-market

https://www.oganalysis.com/industry-reports/automotive-simulation-market

https://www.oganalysis.com/industry-reports/automotive-night-vision-system-market

https://www.oganalysis.com/industry-reports/automotive-adaptive-cruise-control-market

https://www.oganalysis.com/industry-reports/automotive-remote-diagnostic-market

Kategoriler

Read More

Sattva Sanyo Budigere Cross is becoming one of the most promising residential developments in East Bangalore due to its strategic location, modern planning, and growing infrastructure around Budigere Cross. Homebuyers and investors are increasingly exploring this region because of its connectivity to IT hubs, industrial corridors, and major road networks. The project combines...

A new growth forecast report titled Digital Battlefield Market Share, Size, Trends, Industry Analysis Report, By Technology (Artificial Intelligence, Big Data, Master Data Management, Cloud Computing, IoT, Others); By Platform; By Application; By Region; Segment Forecast, 2022-2030 introduced by Polaris Market Research represents conclusive data on the overall market. It majorly...

The Dreadwarden's Ring in New World stands as one of the most iconic and sought-after Legendary rings, a formidable item designed for players who relish combat endurance and aggressive offense. With a New World Gold coins remarkable Gear Score ranging from 726 to 800, this Tier V ring is not only potent in terms of stats but also offers some unique perks that can completely change the way you...

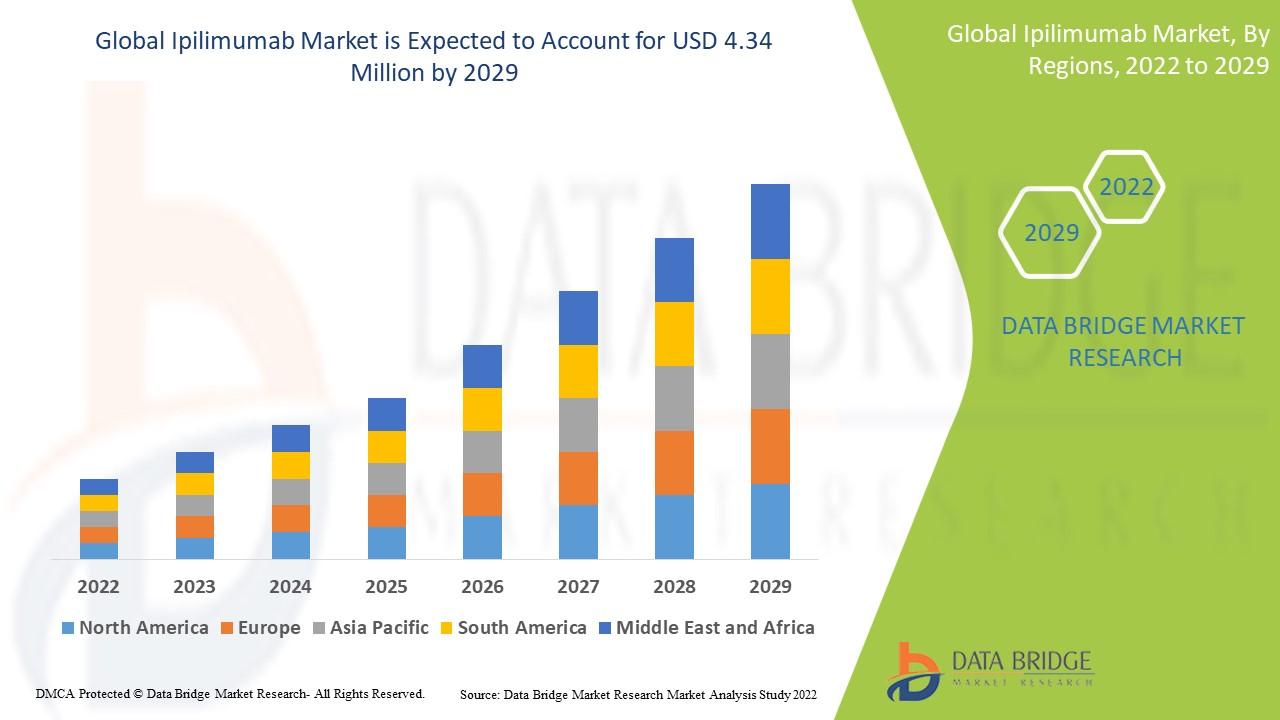

"Executive Summary Ipilimumab Market: Growth Trends and Share Breakdown Data Bridge Market Research analyses that the ipilimumab? market was valued at USD 2.026 million in 2021 and is expected to reach USD 4.34 million by 2029, registering a CAGR of 10.0% during the forecast period of 2022 to 2029. The Ipilimumab Market report has been formed with the appropriate expertises that utilize...

Selecting skilled commercial concrete slab installers Boerne TX is crucial for creating long-lasting business properties. The structural foundation of offices, retail establishments, warehouses, and industrial facilities is a correctly placed concrete slab. Long-term performance, load-bearing strength, and resistance to cracking or shifting over time are all guaranteed by high-quality...