Top Methods to Repay Your Home Loan Faster

Owning a home is a major milestone, but the long-term commitment of a mortgage can feel overwhelming. Reducing your loan tenure not only saves you money on interest but also provides the financial freedom to focus on other goals. By adopting the right strategies, homeowners can repay home loan faster while maintaining a balanced lifestyle. Understanding these methods helps borrowers take control of their mortgage and accelerate repayment effectively.

Increasing your monthly EMI is one of the most straightforward and effective methods to reduce your loan tenure. Even a small increase in EMI payments can significantly impact the total interest and repayment period. For example, if your EMI is $1,800, increasing it to $2,000 allows a larger portion of your payment to go toward the principal, reducing interest charges over time. Before making adjustments, check with your lender regarding prepayment rules, as many banks allow partial prepayments without penalties. Gradual increases in EMI aligned with income growth provide a sustainable approach for early repayment.

Making lump sum payments is another powerful method to reduce your outstanding principal. Bonuses, tax refunds, or other extra income can be allocated directly to the loan. Unlike regular EMIs, lump sum payments immediately lower the principal, which reduces interest calculated on subsequent payments. Strategically timing these payments, such as once a year or during financial windfalls, ensures consistent progress without affecting your day-to-day budget.

Adopting a bi-weekly payment schedule is an effective method to repay your home loan faster. Instead of making one EMI payment each month, divide it into two half-payments every two weeks. This results in 26 half-payments per year, equivalent to 13 full EMIs, effectively giving you an extra payment annually. This method helps reduce the principal more quickly, lowers total interest paid, and shortens the loan tenure. Many lenders now offer bi-weekly payment plans, making it simple for borrowers to implement this strategy.

Refinancing your home loan at a lower interest rate is another method that can help reduce both tenure and interest. When market interest rates drop, switching to a lower-rate loan can either lower your EMI or allow the same EMI to pay off the principal faster. Refinancing can save a substantial amount in interest over the life of the loan and shorten the repayment period. Comparing multiple lender offers and understanding associated refinancing charges ensures that this method is cost-effective and beneficial.

Directing extra payments toward the principal rather than interest is critical for early repayment. Many borrowers make additional payments without specifying allocation, which often results in payments being applied to future EMIs rather than reducing the principal. By instructing your lender to allocate extra payments directly to the principal, you actively reduce the loan balance, save on interest, and shorten your loan tenure. This approach ensures that every additional payment contributes meaningfully to faster repayment.

Using financial windfalls effectively is another important method. Funds from investment returns, fixed deposit maturity, inheritance, or unexpected income can be applied toward the principal. Strategic allocation of these funds accelerates repayment and reduces interest without straining regular finances. Planning and timing such payments throughout the year ensures steady progress toward loan freedom.

Automating extra payments simplifies the repayment process and ensures consistency. Setting up automatic transfers for additional EMIs or lump sum contributions helps borrowers stay disciplined and avoid missed opportunities to reduce the principal. Many banks offer automated prepayment options, making it convenient to maintain a structured repayment plan. Automation allows borrowers to focus on other financial priorities while steadily reducing their mortgage balance.

Regularly monitoring your loan is essential to ensure that your repayment methods are effective. Reviewing statements allows you to track progress, understand the split between principal and interest, and plan future payments efficiently. Monitoring also helps identify opportunities for refinancing or adjusting EMIs to maximize repayment efficiency. Staying informed about your mortgage ensures that strategies remain effective and aligned with your financial goals.

Balancing early repayment with daily financial responsibilities is key to sustainable mortgage management. Setting realistic targets, gradually increasing EMIs, making lump sum payments, using bi-weekly schedules, refinancing when advantageous, prioritizing principal payments, leveraging windfalls, and automating contributions ensures a structured approach. Borrowers who consistently apply these methods can achieve mortgage freedom sooner and enjoy reduced financial stress.

Important Information from This Blog

Repaying your home loan faster not only reduces interest payments but also increases financial flexibility. By increasing EMIs, making lump sum payments, adopting bi-weekly payment schedules, refinancing, prioritizing principal payments, leveraging financial windfalls, and automating contributions, homeowners can shorten their loan tenure effectively. Regular monitoring and careful planning are essential to ensure these methods work efficiently. Early repayment allows homeowners to redirect funds toward investments, savings, or other personal goals, giving them greater financial freedom and security.

At BusinessInfoPro, we empower entrepreneurs, small businesses, and professionals with actionable insights, strategies, and tools to fuel growth. By simplifying complex ideas in business, marketing, and operations, we help you turn challenges into opportunities and navigate today’s dynamic market with confidence. Your success is our mission because when you grow, we grow.

Κατηγορίες

Διαβάζω περισσότερα

The push for net-zero emissions is driving a search for thinner, more effective insulation. The Microporous Insulation Market Growth reflects this, with the sector projected to expand from $2.69 billion in 2025 to $5.2 billion by 2035, driven by a robust 6.9% CAGR. This growth is fueled by stringent energy codes, the need to insulate high-temperature industrial processes, and the...

Proven Ways to Extend CNC Tools Life for Higher Efficiency and Lower Costs In modern manufacturing, efficiency and cost control are critical for success. One of the key factors that directly impacts both is the lifespan of machining tools. Extending tool life not only reduces operational costs but also ensures consistent performance and improved productivity. Proper maintenance, correct...

Executive Summary Latin America Deodorant Market Research: Share and Size Intelligence Data Bridge Market Research analyses that the deodorant market was valued at USD 2806.09 million in 2022 and is expected to reach USD 6800.28 million by 2030, registering a CAGR of 11.70% during the forecast period of 2023 to 2030 Latin America Deodorant Market report makes available the valuable...

Online sports betting is getting better in 2026. It is easier to use. Has better technology and security. More people are using their computers and phones to bet on cricket, football, tennis, and casino games. So it is very important to have an account. Verification keeps your information safe. Helps you use the platform and its money services quickly. A verified Lotus365 account makes betting....

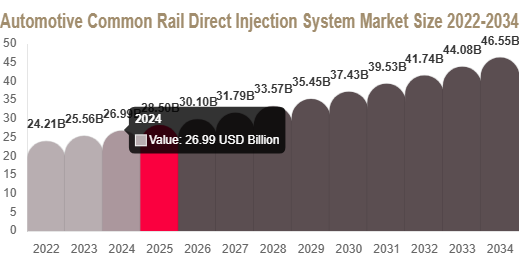

Automotive Common Rail Direct Injection System Market Overview The Automotive Common Rail Direct Injection System Market is witnessing steady growth driven by rising demand for fuel-efficient diesel engines, strict emission regulations, and continuous advancements in injection technologies. Common rail direct injection systems are widely used in diesel engines to improve combustion efficiency,...